“I was dreamin’ when I wrote this So sue me if I go too fast But life is just a party And parties weren’t meant to last ‘Cuz they say... 2000 zero zero party over oops out of time So tonight I’m gonna party like it’s 1999” Prince, 1958-2016 Singer-songwriter, guitar virtuoso

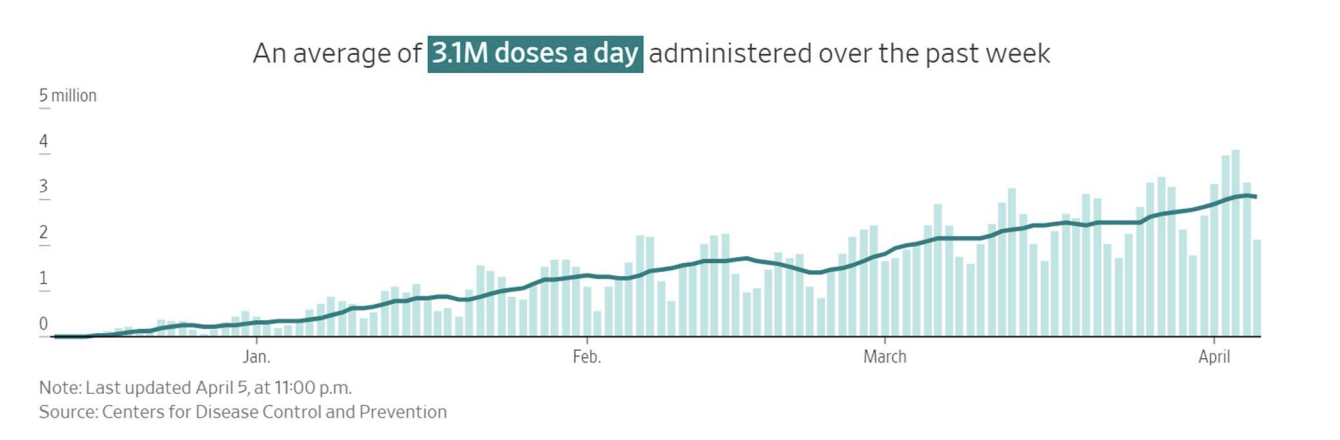

We begin with what we hope will be our final substantive COVID update. The vaccines have arrived and are going into people’s arms at an accelerating pace. The data shows roughly 80% effectiveness after an initial dose, on the way to 90% with full immunization. We in the U.S. are fortunate to be getting vaccinated quickly, as many other regions are not celebrating the end of the pandemic just yet. Much of Europe is currently in some form of lockdown and COVID remains the #1 cause of death in the Americas. Sadly, the developing world will endure this pandemic for at least a couple more years.

We fear any celebration of the end of the pandemic would be premature. This virus is like the villain in a horror film who keeps coming back after you thought you finished him off. The U.K. variant (also known as B117) now represents the majority of cases in the U.S. It is nearly twice as infectious and at least 40% more likely to cause severe illness1. Fortunately, the existing vaccines are effective against this strain. While 36% of the U.S. population has had at least one shot, the current level of immunity alone is insufficient to completely avoid the developing fourth surge2. We believe the rapid and still accelerating vaccine rollout will likely mute the impact of this fourth surge, especially when it comes to deaths and hospitalizations, because the vaccine has been targeted at more vulnerable populations. Moreover, we believe that society is gradually becoming more accepting of health risks as lockdown fatigue and economic collateral damage both continue to mount.

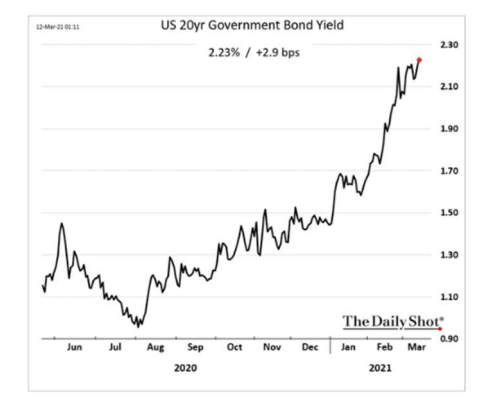

COVID will remain with us for years. A new vaccine-resistant strain may spin out of the world’s unvaccinated populations. Fortunately, we will be better prepared with faster developed booster shots. Like other deadly diseases such as the flu, AIDS, and measles, COVID will remain a serious public health challenge, but not an economic one. We expect this virus to recede from our collective psyche as time passes. For perspective, the world remembers and was scarred by WWI much more than the Spanish Flu of 1918. The latter killed a far greater percentage of the population at the time. Financial markets are now looking past COVID. Rising interest rates have been the primary driver of market activity this year. Short-term interest rates remain zero bound (as the Fed sits tight) while longer-term yields have been rising as the market sniffs out the potential for future inflation. Higher yields mean falling bond prices. Unsurprisingly, longterm bonds have taken a beating, with the 30- Year Treasury declining 15.7% in the first quarter, its worst quarter since 1976.

High yield bonds experienced a brief and orderly decline, as improving credit conditions offset the adverse increase in rates. This contrasts with the sometimes-violent selloffs caused by economic recession fears. No one currently fears a recession... at least not the type in which big companies go bankrupt and default on their debts. As a result, our Managed Income strategy delivered a positive return for the quarter as compared to the -3.4% total return for investment grade bonds3.

The S&P 500 Index returned a solid +6.2% in the first quarter and more recently crossed the 4,000 mark for the first time. However, there has been a lot of noise under the hood, with wild swings in individual stock prices from day to day. Rising interest rates have generally hurt those stocks which have been valued more on expectations of future profitability, as those profits are now worth less in today’s dollars. Higher rates have brought forth new leadership among more economically sensitive “short duration” stocks. The first quarter was mirror opposite to last year’s market environment, with value and energy stocks leading and technology and growth stocks lagging.

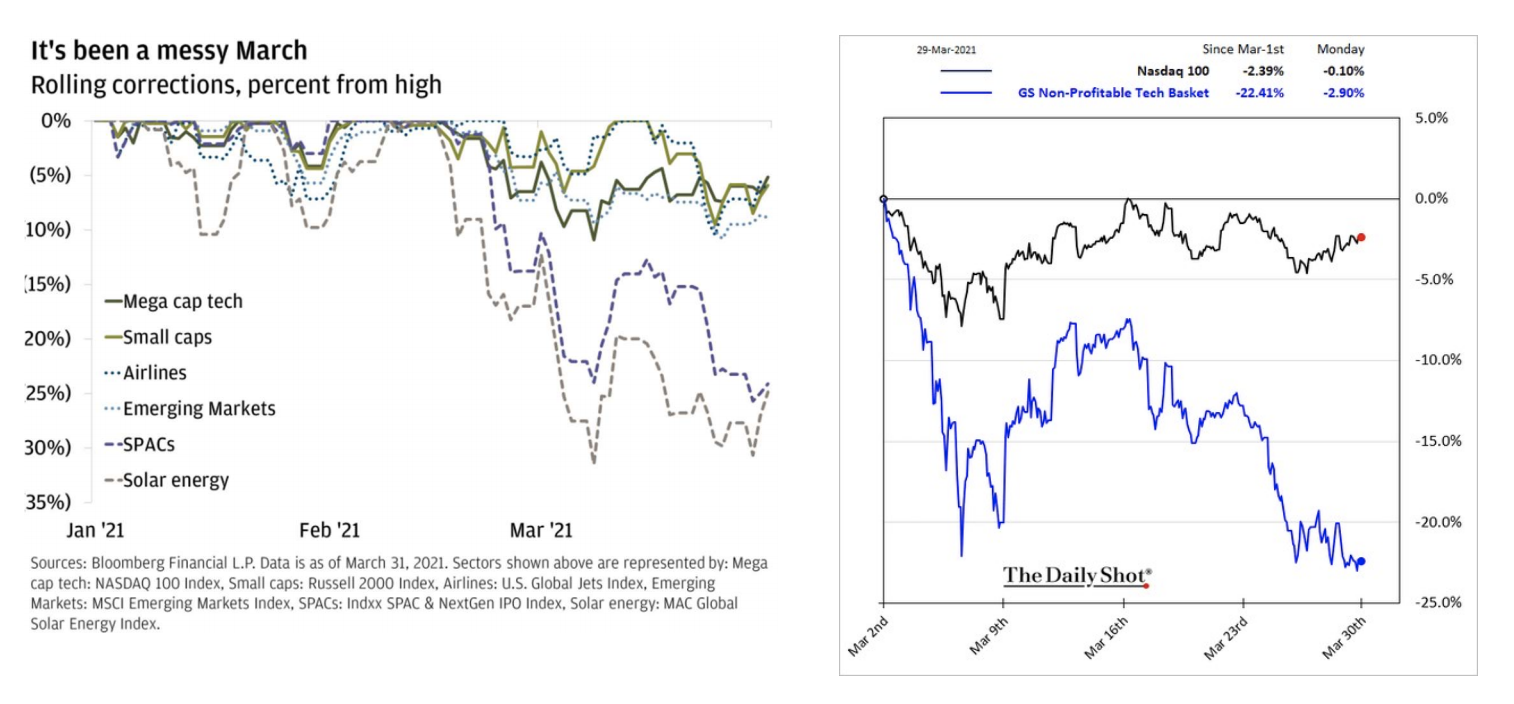

This year began with public interest in investing at a level not seen since the late-1990s dotcom boom. More recently, some of the bloom is off the rose: retail trading volumes are down and many novice traders likely experienced losses for the first time. As a result, the air has started to come out of some of the hottest market fads. As the charts atop the next page highlight, formerly red-hot solar energy stocks and SPACs have declined precipitously along with unprofitable tech companies. Norevenue EV maker and former market darling, Nikola, has dropped from $80 to $13. Tesla, a bellwether for popular momentum stocks, was off 37% earlier this year.

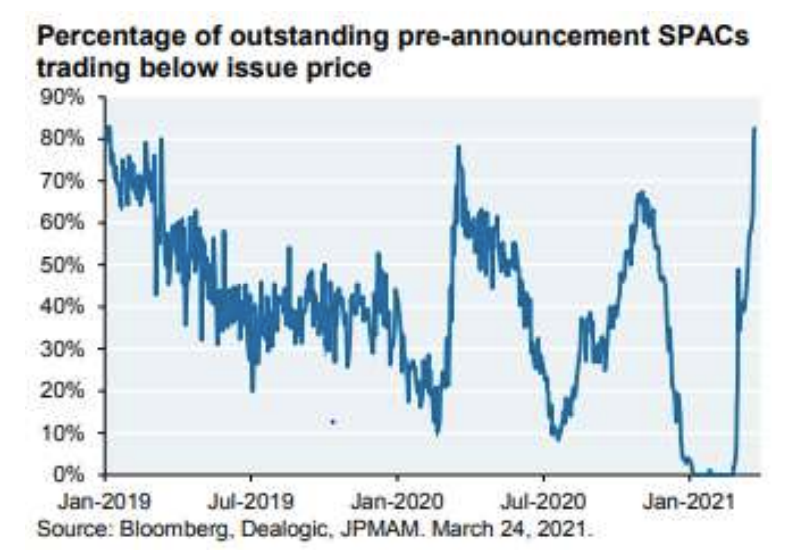

SPACs (Special Purpose Acquisition Vehicles) were all the rage to start the year. They now appear to be unraveling. These blank check companies typically IPO at a $10 price and have two years to acquire a company with their newfound cash. Earlier this year, hundreds of recently issued SPACs were priced at a premium to their IPO price, signaling investor enthusiasm toward what these management teams might go out and acquire. Post-acquisition, SPACs are starting to issue guidance on expected financial results; most are far below the predictions made at the time of their deals. In response, more than 80% of SPACs now trade below their IPO price (see chart below).

Is the end of the SPAC fad a canary in the coal mine for markets? Or simply a healthy cessation of speculative excess? We think the latter. 5 One potential area of frothiness is housing. Home prices have been particularly strong of late, driven by record low inventory levels. We question the idea that now is a great time to buy. The temporary prohibitions of foreclosures has heretofore limited a natural source of housing supply. Also, improving COVID conditions may curtail migration to the suburbs and put city living back in vogue. Thirdly, mortgage rates are on the move, which initially boosts buying demand, but soon turns into an affordability headwind.

As to the overall U.S. economy, it will run red-hot in 2021 and deliver some of the greatest GDP growth we may witness in our lifetimes. A powerful cocktail of record fiscal stimulus (government spending) and monetary stimulus (the Fed’s money printing) poured on top of a reopening should remove all economic inhibition. People are getting back to work and venturing out to spend4.

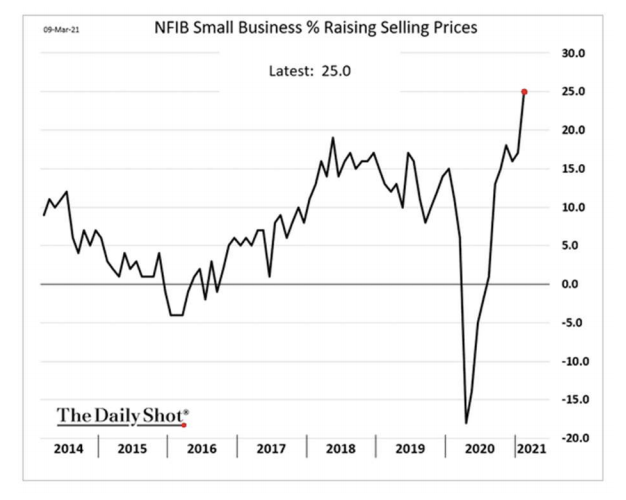

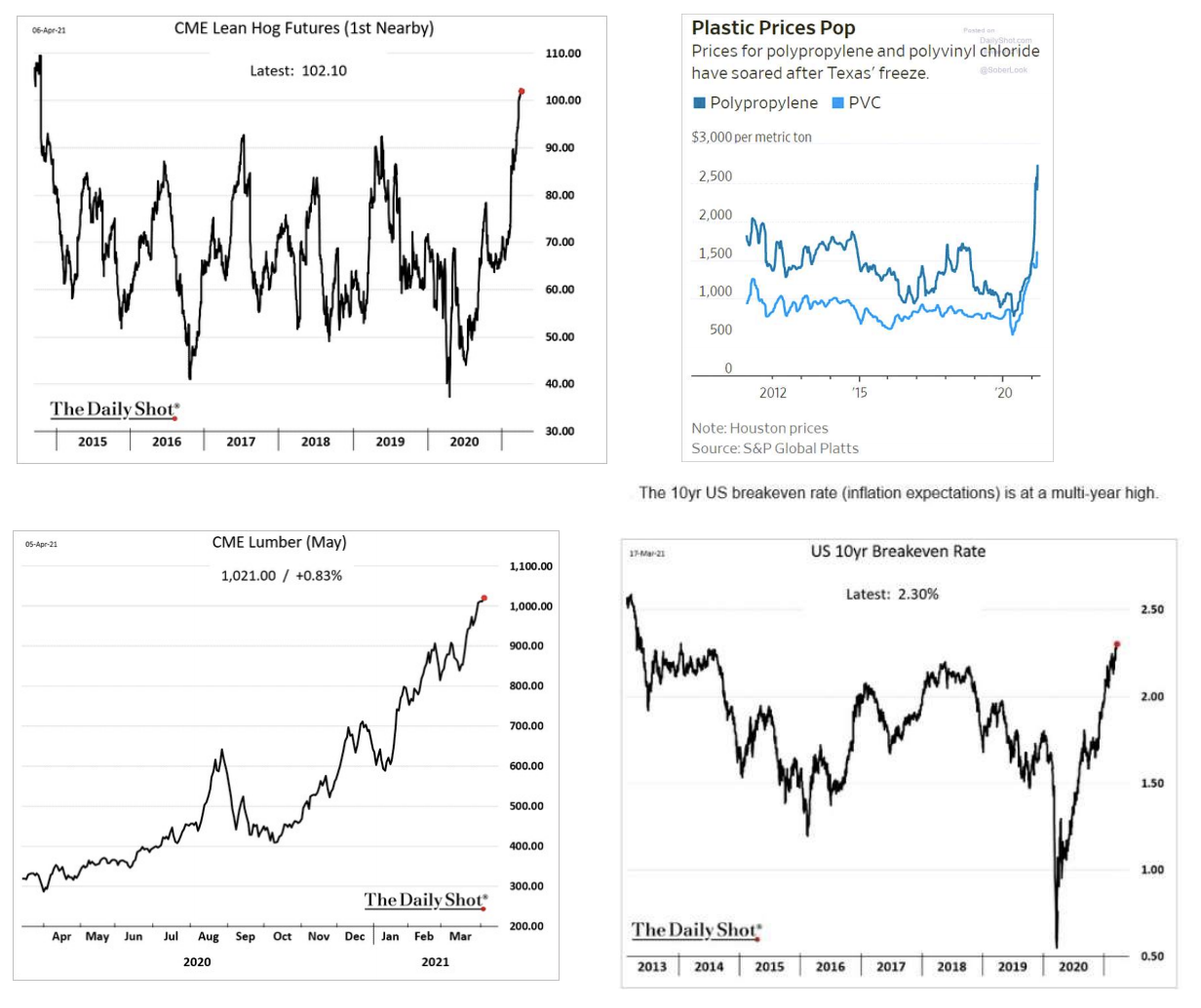

Already, inflation appears to be everywhere... except in the oft-cited Core Consumer Price Index, which is nudging upward at an annualized 1.3% rate. Businesses are telling us they are raising prices (at right). As the other following charts indicate, input prices are skyrocketing. Adding to inflation pressures are supply shocks from the pileups at the Suez Canal and the shutdowns of petrochemical plants due to the Texas deep-freeze. Here in Newport Beach, we look offshore and see container ships backed up across the horizon. One of our clients is now paying nearly three times as much to ship containers from China. The market’s future inflation expectations are shown in the “10-year breakeven rate” (bottom right), which has risen sharply over the past year.

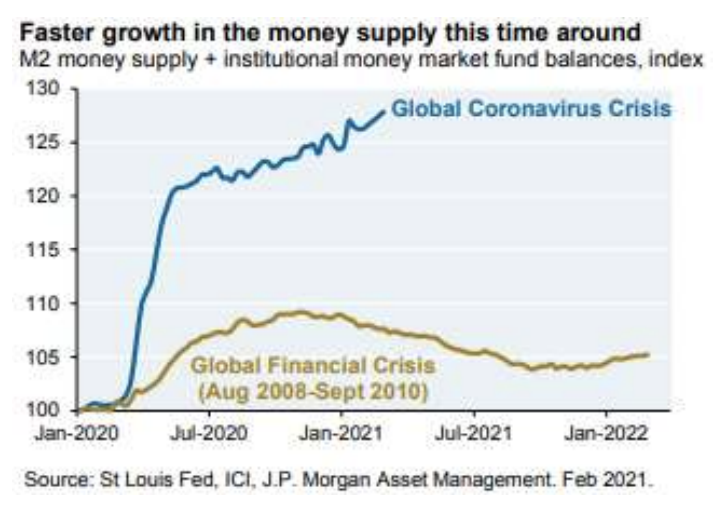

The Federal Reserve is the traditional guardian against inflation. It is the Fed’s job to raise interest rates to cool the economy before it overheats and causes inflation. The Fed’s historic practice has been to raise interest rates to head off inflation before it appears. The Fed now believes in the past it has been too aggressive in fighting inflation. This new mentality means the traditional guardian against inflation is not only stating it won’t aggressively fight inflation, but that it actually wants inflation above two percent. This not a secret. Still, it represents such a dramatic sea change from the past that we doubt the market has fully processed it. A perfect storm appears to be coming together to cause inflation. Unprecedented money printing has fueled money supply growth far beyond the (also unprecedented) rate seen during the Global Financial Crisis... and continues apace.

This new money translates into increased spending power. Massive consumer demand may overwhelm COVID-constrained supply. The current setting seems like a classic case of too much money chasing too few goods. This, along with a Fed committed to being behind the eight ball when it comes to hiking rates, likely means we are in store for an inflationary episode. With the stock market at all-time highs, we expect some “freak out” about the Fed’s ability to control inflation, which they will undoubtedly label “transitory”. The financial headlines will likely be dominated by discussions as to whether emergent inflation is merely a transitory “blip” or the start of a relentless out-of-control trend. This is the trillion-dollar question that we believe will dictate financial markets in late 2021- 2022. For now, the ocean of liquidity likely wins the day. Some of it will be spent on goods, which will cause inflation. Much of it will be absorbed by the stock market, driving further appreciation. Thus, we are relatively fully invested, though we remain watchful for when the shortterm becomes the long-term. 8 We thank you for the continued trust you place in us.

Sincerely,

John G. Prichard, Miles E. Yourman, Kurt Beimfohr, Jeff Vieth

Knightsbridge Wealth Management reviews and updates Form ADV at least annually to confirm that it remains current. No material changes were made since the last update to Knightsbridge’s brochure dated October 1, 2020. Our complete Form ADV Part 2A & 2B may be requested by contacting our firm at (949) 644-4444 or by email at [email protected]. Please remember to contact us if there are any changes in your financial situation or investment objectives. Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 This includes increased illness among younger people. Unlike the original strain, children do become infected at regular rates, which has facilitated the spread. 2 This is demonstrated by the experience of Chile and Michigan, both of which have experienced challenging surges despite having vaccination rates similar to that of the U.S. as a whole. 3 As approximated by the Bloomberg Barclays U.S. Aggregate Bond Index. 4 Consumption makes up 70% of the U.S. economy.

Read more commentaries by Knightsbridge Asset Management