KEY THOUGHTS

- The S&P 500 finished 1Q21 at a new all-time high (+6% YTD), but performance masks the volatility under the surface.

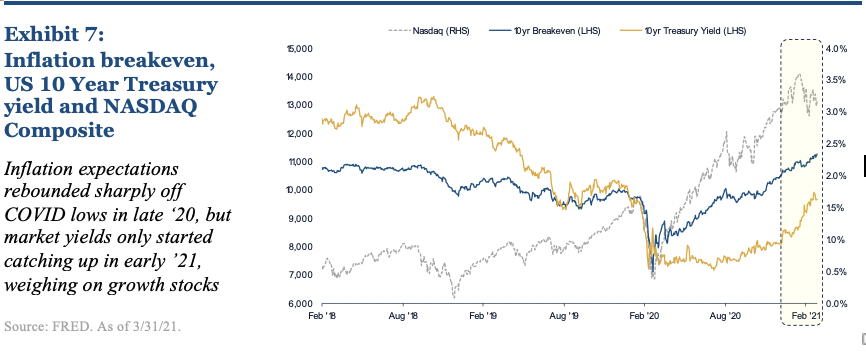

- Inflationary concerns are moving yields higher, weighing on growth stocks and causing investors to question the Fed’s course of action.

- GDP estimates in the US are being revised higher as pent-up consumer demand, warm weather, stimulus checks and vaccinations become a catalyst for a spending uptick.

- Unemployment continues to trend lower, and in states that have “reopened” unemployment is approaching pre-COVID levels.

Massive fiscal stimulus helped stem off a global depression, but investors are now realizing there are consequences (e.g. higher taxes).

The S&P 500 is up nearly 80% since March 23, 2020 (the COVID beak market bottom). The economic recovery is in full swing, and between stimulus checks, warm weather, and widespread vaccinations recovery momentum is likely to surge this summer; especially if the labor market recovery accelerates given reopening states and an uptick in services sector spending. In conjunction, we think markets should continue to push higher, although downside volatility is intensifying as headwinds from rising rates and the long-term consequences of stimulus (e.g. higher taxes) become more prevalent. We continue to see opportunity in risk assets near-term, but suggest taking a more balanced equity approach going forward, especially given the recent rotation from growth to value.

TO THE POINT

Summer spending surge will boost the economy but then what?

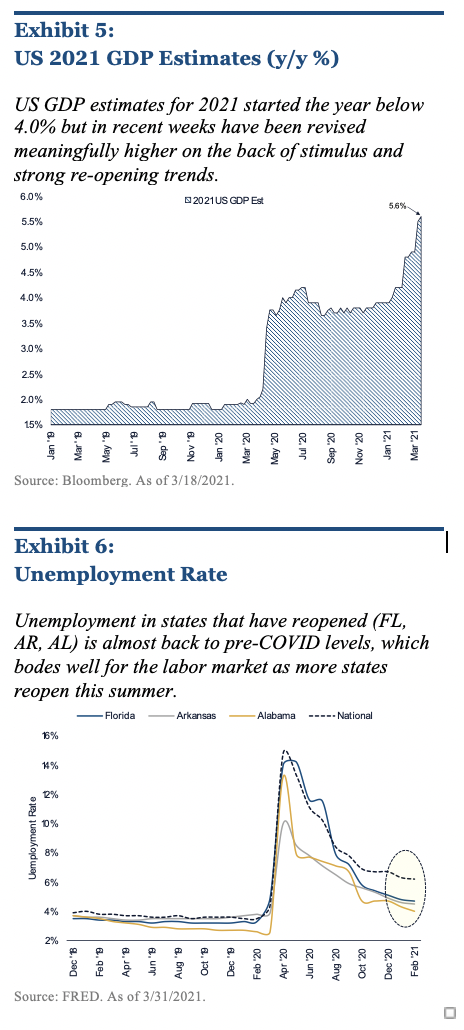

After one of the most volatile years in markets and the global economy the world is (finally) re-opening. The S&P 500 is up nearly 80% since its March 23, 2020 low and is off to another strong start in 2021 (up 6%). This summer the combination of warmer weather, stimulus checks and widespread vaccinations are likely to act as a catalyst for a surge in consumer spending, both for goods and services. And with this pick-up in activity we think labor market improvement will accelerate as services-sector businesses look to ramp-up hiring (See Exhibit 6).

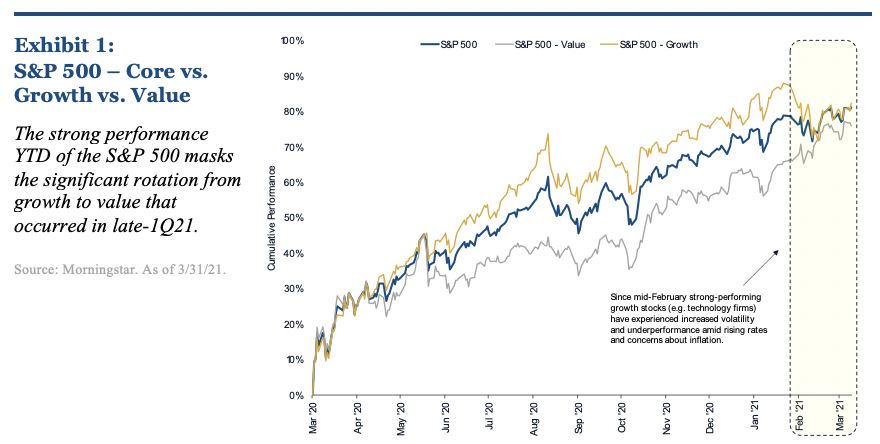

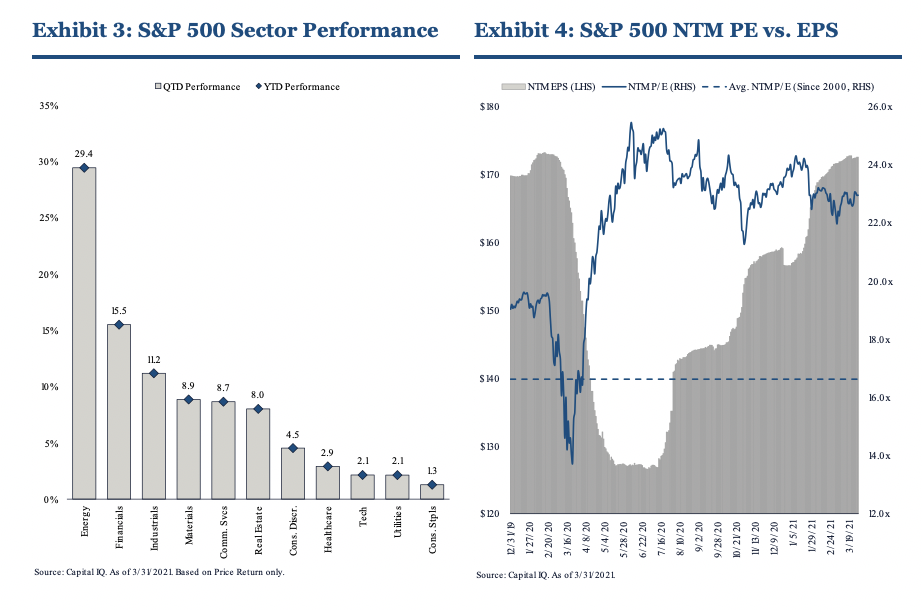

However, despite the economic growth optimism there are structural changes occurring in markets that worry us. Specifically, the robust S&P 500 performance is masking investor preference changes, highlighted by the rotation out of high growth stocks and into more value-oriented defensive stocks (See Exhibit 1 and Exhibit 3). And on the fixed income side, a disconnect between investors and the Fed is occurring as bond yields shot up in late-1Q over investor inflation concerns, even as the Fed reiterated their stance of holding rates low.

In addition, we are concerned about the lingering implications of Biden’s stimulus (both CARES Act and Infrastructure) and an overheating economy. While we continue to believe the Fed will keep rates low into 2023, we think robust improvement in unemployment and higher inflation expectations may push the Fed to scale back their accommodative polices in late-2021. And if this occurs, we expect interest rates and yields will likely continue their trajectory higher. To hedge against these risks, we suggest de-emphasizing growth (e.g. technology stocks) in portfolios and adding core/value exposure. In addition, we continue to see opportunities in Real Assets for current income and inflation hedging given inflation and Biden’s Infrastructure Plan.

TIMELY TOPICS

Signs of improvement

|

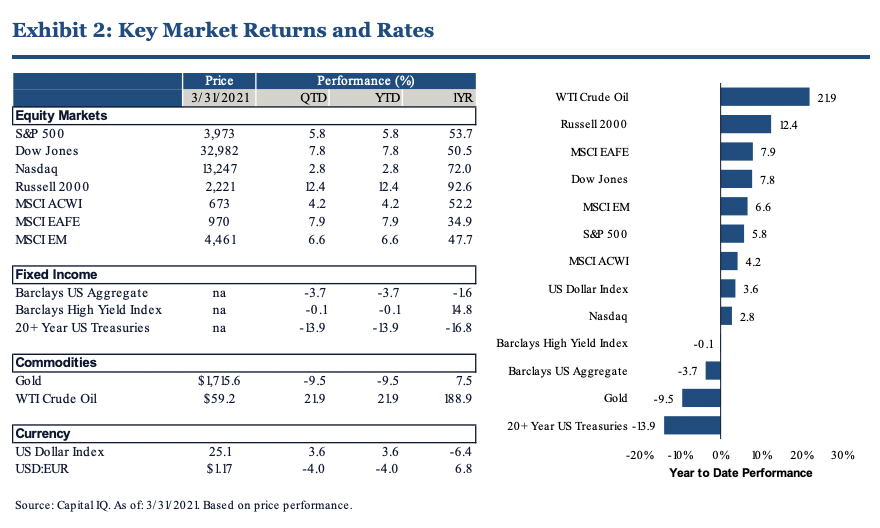

Investors pushed bond yields higher in 1Q, even as the Fed kept rates low and maintained accommodative polices. The yield on the US 10yr Treasury finished 1Q at 1.74%, its highest level since the beginning of 2020 as investor concerns over rising inflation outweighed Fed commentary to remain accommodative. Markets now face a dislocation between the Fed's stance (no rate hikes until 2023), and investor expectations that the Fed will hike sooner.

Unemployment improvement in re-opened states bodes well for the rest of the US. States that have re-opened “fully” have experienced a marked decrease in unemployment vs. peers, with overall state unemployment declining near pre-COVID levels (See Exhibit 6). As more states re-open this summer we expect national unemployment improvement should accelerate, driven by services sector re-hiring.

GDP growth estimates in the US are moving higher. Economists expect pent up consumer demand, warm weather, stimulus, and widespread vaccinations to be the catalyst for a massive summer of consumer spending. As the US reopens this summer it remains the best positioned developed country to recover from COVID. See Exhibit 5.

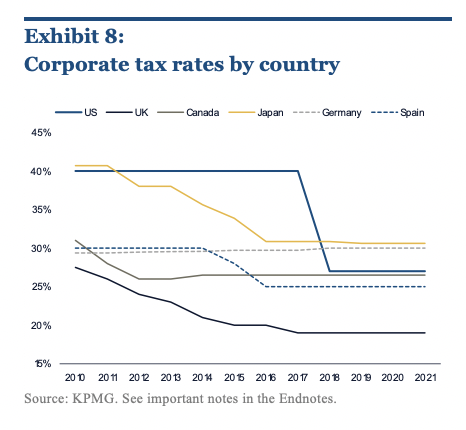

President Biden announced nearly $3.9tn in stimulus in 1Q21 (CARES Act & Infrastructure Plan) in an effort to boost the US economy. In addition to the $1.9tn CARES Act that was signed into law in 1Q, Biden also announced a $2.0tn infrastructure plan. Near-term these stimulus efforts further support market momentum and will likely drive unemployment lower and boost US GDP. The longer-term impact of the stimulus is less certain as higher taxes (both individual and corporate) may weigh on economic activity.

|

|

LOOKING AHEAD

Stimulus implications

Inflationary concerns are moving yields higher, weighing on growth stocks, and causing investors to question the Fed’s course of action. Inflation is likely to spike in the coming months as states reopen and vaccinated consumers take advantage of warm weather and stimulus checks. The key question will be the longevity of inflation, and if it remains elevated after the initial spike. Most economists continue to predict that that inflation trends will remain low into the foreseeable future, but investor inflation expectations may continue to move higher. If this persists, we think current (and future) rises in interest rates will become economic headwinds and weigh on risk asset valuations, even if the Fed maintains low rates.

Higher corporate tax rates are coming. With the Biden’s announcement of the $2tn Infrastructure Plan corporate tax rates in the US are all but certain to move higher, presenting a potential headwind to economic growth.

We suggest tactically adjusting portfolios to protect against unexpected inflation. We remain optimistic on risk assets, but suggest investors tactically reduce exposure to growth equities which are most likely impacted by inflation. In addition, given Biden’s proposed infrastructure plan we continue to suggest a tactical overweight to Real Assets, which should help limit the impact of unexpected inflation.

ENDNOTES

Disclosures

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This presentation is not intended to be used as a guide to investing, or as a source of any specific investment recommendations, and makes no implied or expressed recommendations concerning the manner in which any client’s account should or would be handled, or warranties regarding investment performance, as appropriate investment strategies depend upon the client’s investment objectives. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance is no guarantee of future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Glossary

MSCI ACWI-All Country World (ex U.S.) Index is a market capitalization weighted index designed to provide a broad measure of global equity market performance excluding the U.S. MSCI EAFE Index is a free float-adjusted market capitalization weighted index designed to measure developed market equity performance, excluding the U.S. and Canada. MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. Russell 2000® Index measures the performance of approximately 2,000 small-cap companies in the Russell 3000 Index, which is made up of 3,000 of the biggest U.S. stocks. Russell 2000® Growth Index measures the performance of the large-cap growth segment of the Russell 2000 Index. Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq. Nasdaq Composite is a stock market index of the common stocks and similar securities listed on the NASDAQ stock market. S&P 500® Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy.

Exhibit 8: In the US the federal corporate income tax rate is a flat 21%, for taxable years beginning after December 31, 2017. Most state and many local governments impose net income taxes. The top marginal rate generally ranges from 0% to 12%, with the mean of the top state tax rates being roughly 7.5%. In addition, many states and localities also impose gross receipts taxes, capital-based taxes, and other taxes that are not reflected in the rates provided. A corporation generally may deduct its state and local income tax expense when computing its federal taxable income, resulting in a net effective rate of approximately 27%.

A word on risk

All investments carry a certain degree of risk, including possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-U.S. investments involve risks such as currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. This report should not be regarded by the recipients as a substitute for the exercise of their own judgment. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Investment advisory services provided by Defiant Capital Group LLC, a registered investment adviser.

© Defiant Capital Group

More Insurance & Annuities Topics >