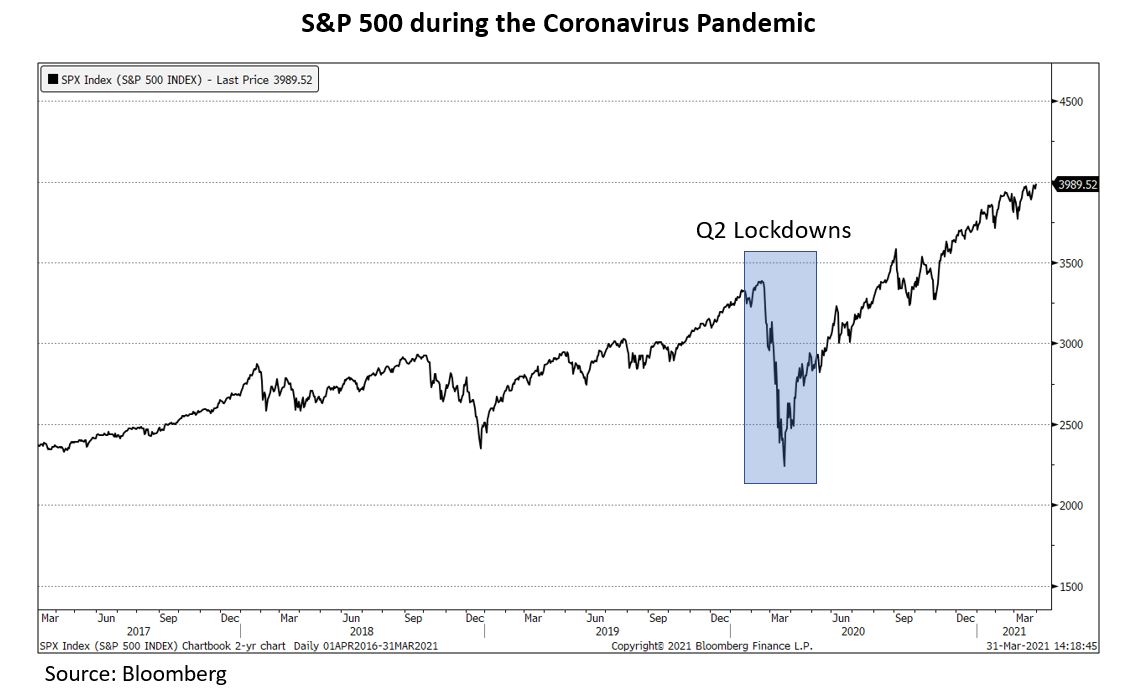

We have all endured the Covid-19 pandemic for over a year now. And while a light at the end of the tunnel may be glowing, the stock market showed very few signs that the pandemic ever existed. The first quarter of 2021 was business as usual, with the S&P 500 gaining over 6%.

Over the past twelve months, equities have benefited from the massive amount of stimulus monies pumped into the US economy. The loose monetary and fiscal policy has supported various asset classes, from equity to real estate. The indiscriminate lending to businesses in March 2020 through the Paycheck Protection Program buoyed asset prices as the pandemic accelerated. The more recent America Rescue Plan will provide direct stimulus to consumers; the backbone of the US economy. Over the long-term however, we need to be mindful of the negative consequences fiscal leniency creates. The helicopter money could undermine the investment environment should the aggressive stimulus be inflationary or impact interest rates significantly. So what is the stock market telling us?

Biden vs. S&P 500

Prior to the pandemic the former administration looked poised to retain the White House. The economy was humming and a resolution in the trade war with China seemed forthcoming. Yet, the spread of Covid-19 changed everything. However, a shift in the political landscape barely registered in the US stock market. We have previously written how the resident of the White House should be well down on the list of investors’ concerns (click here) and yet again, the change in Washington is hard to discern.

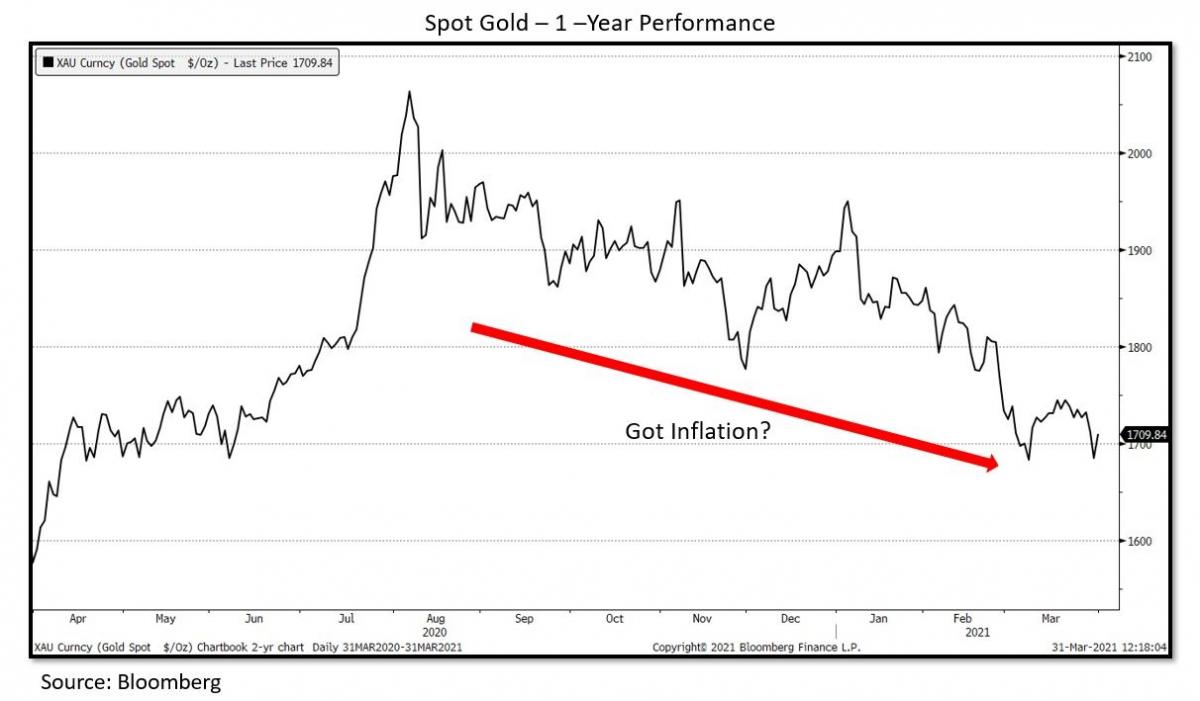

Inflation & Gold

After two large rounds of stimulus, a jump in energy prices (due to problems in Texas and rising oil demand), an assault on the US democracy, global macroeconomic uncertainty, and a sizable pending infrastructure package, gold has done NOTHING. If inflationary pressures were building, spot gold would be the canary in the coal mine. Today, investing in gold is as easy and supposedly as liquid as your average ETF, yet the price action does not signal inflation nor show a flight to safety. The chart below displays the 1-year performance of Gold.

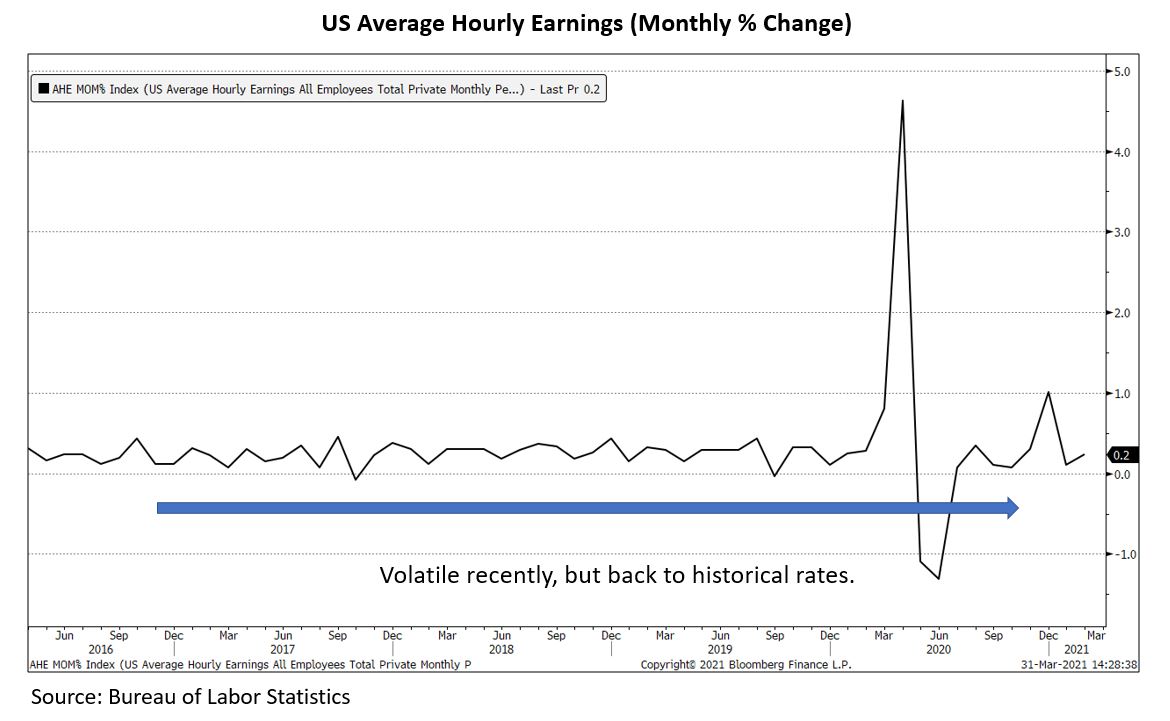

Wages & Unemployment

The second important measure of inflation that we monitor closely is wages. Labor costs are a key input for most businesses. As wage expense goes up, the prices of goods also rise as businesses seek to maintain and protect profits. Yet, hourly wages have remained stagnant. After a quick blip during the first round of stimulus programs, average hourly earnings continue to trend nowhere. This is likely due to the sudden jump in lockdown-related unemployment. With the US unemployment rate at 6.7%, it is hard to see wage pressure feeding overall inflation. It is also unlikely a $15 minimum wage can be implemented during an economic recovery. Interestingly, the US stock market tends to do well when unemployment is falling from high levels.

Pharma & Vaccine

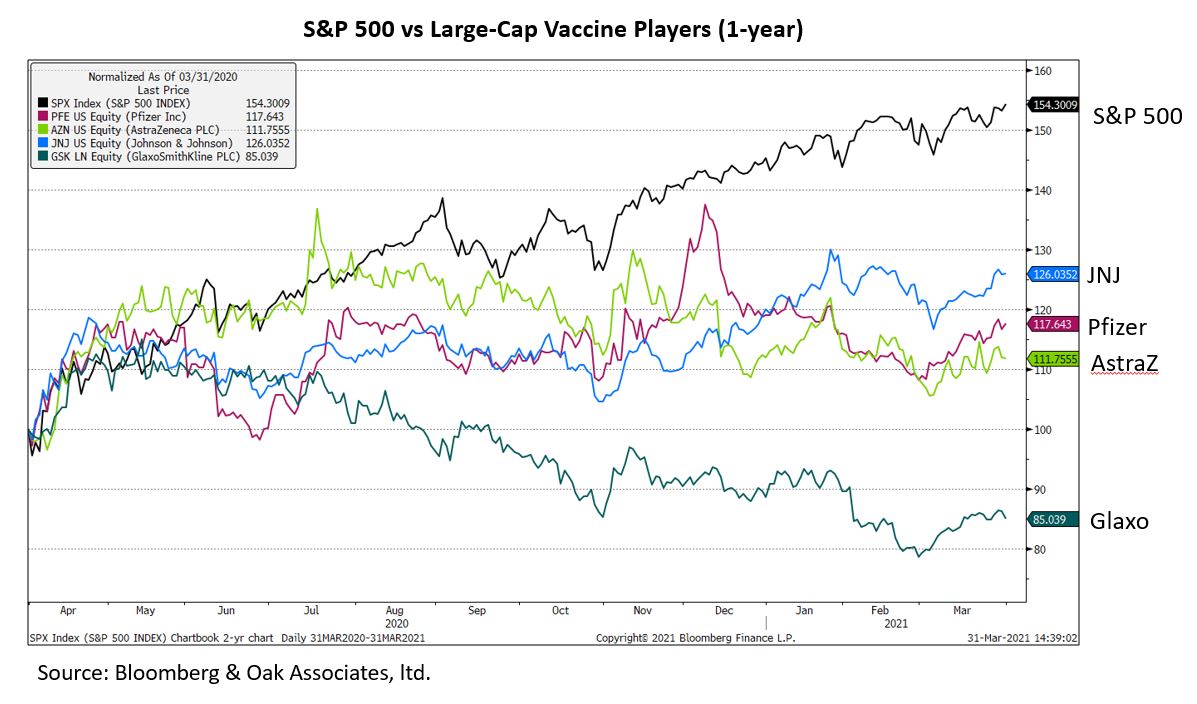

Finally, large-cap pharmaceutical companies deserve enormous credit for the development of multiple coronavirus vaccines. While other countries successfully managed outbreaks of the Coronavirus (ultimately limiting its mortality), the US’s laissez faire approach has necessitated an external intervention to break the chain of contagion to defeat the pandemic. In this regard, what multiple pharmaceutical companies have achieved is impressive and as a nation we should be extremely grateful. Yet, as investors, the vaccine has been mostly invisible to share prices. Yes, several small unprofitable biotechs have skyrocketed due to the sudden market opportunity that developed, but the main players in vaccine production and development have been laggards. The charts below show the performance of the S&P 500 relative to leading vaccine players over the past two years. Nowhere is the pandemic evident in their performance.

The groups’ relative underperformance might be due to the highly competitive vaccine market and the fact that the opportunity may disappear once herd immunity is reached. Governmental pressure to keep pandemic-induced profits down may also have weighed on the sector, not to mention the prospects of more aggressive price controls for drug companies. Regardless, we are somewhat amiss at the underperformance of pharma during the first pandemic in 100 years given their crucial role in its eradication.

In conclusion, the most important factor for equity investors is the underlying investment environment. The outlook for inflation, interest rates, and unemployment all play a key role here. Thus far, the level and direction of these components remain favorable for the economy and equity markets. The Fed has reiterated its intentions to keep interest rates low for an extended period. Inflation seems absent in traditional segments that often warn of building pressures. Slack in the labor market remains due to the pandemic’s spike in unemployment and this should help keep wage pressure down. Although interest rates have risen some, in the big picture they remain very low. Certainly, areas of high valuation may struggle relative to other areas of the market, but as a whole, a return to economic normalcy continues.

Thank you for your investment with Oak Associates. Stay safe.

Robert Stimpson, CFA, CMT

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell.

To determine if this Fund is an appropriate investment for you, carefully consider the Fund's investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Fund's Prospectus which may be obtained by calling 1-888-462-5386 or visiting our website at www.oakfunds.com. Please read it carefully before investing. Mutual fund investing involves risk, including possible loss of principal.

This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC. Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.

Ultimus Fund Solutions, LLC is not affiliated with Constant Contact.

Read more commentaries by Oak Associates