The benefits of a growth/value blend

We believe it’s important to own both growth and value stocks in a portfolio. A blend of the two investment styles has offered the most compelling risk/reward over time, as shown in the Better together chart below, balancing the historically higher volatility in value and lower return in growth.

Our research also reveals that growth and value are essentially anti-correlated: One generally thrives in an environment where the other lags, and vice versa. This means investors can build a more resilient, all-weather portfolio by incorporating the relative strengths of both growth and value – and can potentially enhance those results by working with astute managers that can consistently beat their growth/value benchmarks.

Better together

Risk and reward for growth, value and blend, 1926-2020

Scope to increase value

While both growth and value extend benefits, portfolios may have room for greater value exposure. Market indexes typically tilt toward growth stocks. Because investors assign higher prices to growth stocks, they carry higher market capitalizations – and greater representation in market-cap-weighted indexes. The S&P 500 Index was 67% growth stocks as of mid-February 2021. Value is similarly underrepresented in investor portfolios. A BlackRock Portfolio Solutions (BPS) review of more than 18,000 advisor model portfolios at year-end 2020 showed 62% were underweight value.*

BlackRock’s Fundamental Equities investors have identified the opportunity and are closing the growth/value gap. The most recent data for U.S. portfolios showed a platform-level shift toward value after a long-held pro-growth bias.

Shorter- and longer-term tailwinds

We believe now is a particularly good time to consider increasing value positions, as recent strength could have staying power not seen in years.

The key near-term booster, as we outlined in a recent Market Minute, is value’s history of outperformance in the period rising out of a recession. Cyclically oriented value stocks were the most depressed in the COVID-driven downturn and, we believe, have more room to run in the recovery period.

In the longer term, we see a higher inflation regime as supportive of value stocks. While we don’t see rising inflation as an imminent issue, it is a real risk in the medium term. As we discuss in our latest equity market outlook, the coronavirus crisis compelled the biggest global fiscal and monetary stimulus seen in the post-WWII era. Combined with pent-up demand accrued during lockdowns and consumer savings waiting to be unleashed, the risk for rising inflation is higher than it has been in decades. The BlackRock Investment Institute sees a higher inflation regime in the next five years.

Value’s edge amid rising inflation

Value equities have historically demonstrated greatest outperformance during inflationary episodes.

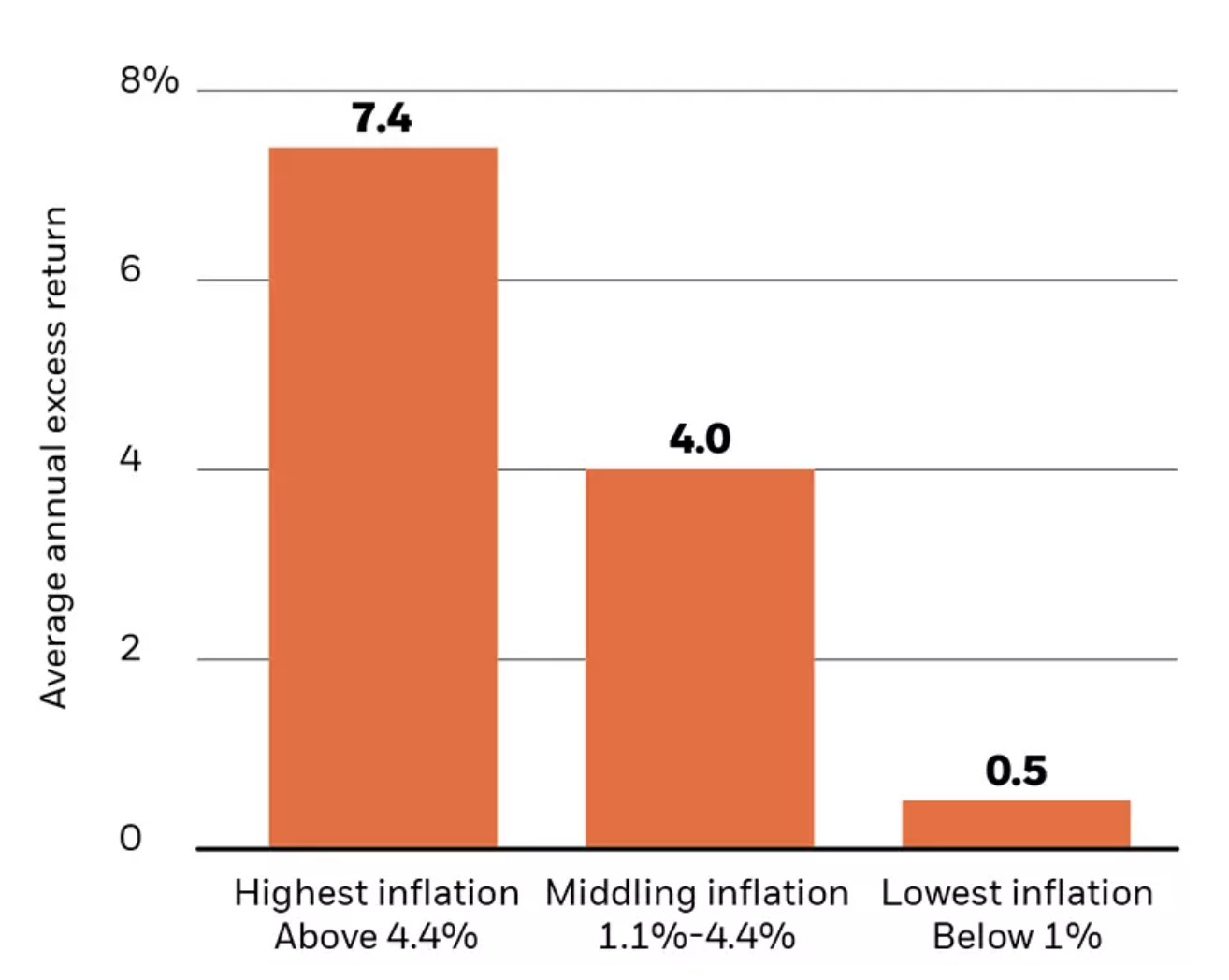

We looked at data back to 1927 and found value has outperformed growth by the largest margin in periods of moderate to high inflation, as shown in the chart below. It is only when inflation is very low that value performance pales – as evidenced in the past 10 years. Notably, it does not take runaway inflation for value to gain an edge. Value outpaced growth in the period of middling inflation, which ranges from 1.1% to 4.4%. This is more in keeping with our outlook this cycle versus the highest inflation periods that averaged 8.4%.

History of inflation fighting

Value outperformance by inflation regime, 1927-2020

Actively managing risks

Whether focused on growth or value, we see an active approach as critical in the current environment where each presents distinct risks.

In the value universe, the key is avoiding “value traps” – companies that are cheap for good reason and unlikely to appreciate. In growth, the question is whether companies can continue meeting investors’ lofty expectations. This means distinguishing between those companies that can continue to deliver earnings growth in a post-COVID world and those where demand was simply pulled forward during the pandemic, pinching future earnings potential. We believe navigating these risks well requires the expertise of a skilled active manager.

© BlackRock

Read more commentaries by BlackRock