Is it possible to travel in two directions at the same time? Imagine walking to the restroom at the back of an airplane while in mid-flight. One would have, quite deliberately, been completing two missions at once, in completely opposite directions, and at very different speeds.

Economic cycles can display similar characteristics: there are longer demographic cycles that are in a downtrend today (further accelerated by Covid), which suggest lower levels of potential growth and a greater need for commercial efficiency to mitigate a shrinking workforce. Simultaneously, this very same need for efficiency is driving a rapid technological revolution that is in the midst of an uptrend (the CC: All economy, as we described previously), which is also accelerated by Covid. Balanced portfolios need to appreciate both of these cycles, among others, while navigating yet another cycle: the market cycle.

Indeed, the market cycle appears to be traveling at warp speed today. In less than 12 months, we have experienced a historic meltdown, a bottom carved out by fiscal and monetary policy action, and a full market recovery. But In the background of this hyper-speed activity, there appear to be some clear and distinct investment regimes evolving. We think we’ve passed through two regimes, are nearing the tail end of a third and are at the precipice of entering the fourth.

Regime 1: Covid gets priced by the market, illiquidity persists

No superlative does justice to the market carnage in March 2020. The S&P 500 experienced its fastest 30% drawdown in its history, leaving the Great Depression a distant second (it took twice as long then). What started as a social/humanitarian crisis threatened to become a full-blown credit crisis, as the uncertainty around future cash flow streams resulted in spread blowouts, inverted spread curves, and frozen capital markets. Investors sought liquidity by raising cash, in order to meet impending redemptions, as evidenced by record money market inflows. Yet, surprisingly perhaps, the cleanest indicators of an illiquid panic were to be found in the rates market – through a spike in real rates and collapse in inflation breakevens – suggesting a deflationary bust so severe that it required an immediate policy response.

Regime 2: Central bank steps in and provides liquidity

And what a policy response it was. Global liquidity increased by a staggering $7.5 trillion in 2020, setting a new record, as policymakers sought to force real rates down, and restore inflation expectations (spoiler alert: they succeeded at both). Our investment response at the time was to follow the Federal Reserve by buying both duration and high-quality assets. The spreads on offer in AAA securitized (auto loans at 400 basis points (bps); student loans at 600 bps) and yield pickups from moving one notch down in investment grade credit (100 bps to move from single A to BBB, for example), made it quite unnecessary for fixed income investors to reach much further down the capital stack in order to hit 4% to 5% yield targets. And returns very much reflected this wave of liquidity lifting all boats – almost all major asset class performed extremely well from April through July.

Regime 3: Monetary, fiscal policy and vaccine effectiveness begin to get priced

As investors began to appreciate the sheer magnitude of the policy response in the later part of 2020, news of successful vaccine trials also began to infiltrate markets and price action, reaching a climax in just the last few months. Since at least August, investors have been rewarded for moving down in quality, out of duration and rich high-quality assets and into beaten down assets including high yield, emerging markets, and equities. Viewed through the interest rate lens, real rates remained low and stable, while breakevens continued their recovery into above-average territory, reaching highs not seen since at least 2014 (roughly where we stand today) and supporting risk sentiment.

Regime 4: The market starts pricing in more robust real growth

So, what happens next? As in prior regimes, asset allocation going forward will likely be about determining what drives nominal interest rates, the correlation between breakevens and real rates, and whether the spread between breakevens and real rates widens or narrows. We think Regime 4 will likely be characterized by one final real rate/breakeven permutation: rising real rates and high but stable breakevens, as we have already begun to see. Going forward, changes in the composition of nominal rates should better reflect changes in the composition of nominal GDP – and with real GDP potentially hitting 7% by the end of the year, with inflation at a healthy 2% to 3%, 10-Year real rates no longer need to stay at negative emergency levels of -1%. And while 10-Year breakevens could rise further, substantial inflation expectations are already baked into a roughly 2.25% price.

Said differently, betting on real rates dropping significantly further from the lowest point in their history, ahead of the biggest positive demand shock in decades, is not a bet we want to make today.

The economic and market backdrop that policy built

The $30 trillion in global stimulus, of which the U.S. portion accounts for 54% of U.S. GDP, is starting to find its way into consensus growth estimates. Last year, U.S. GDP estimates rose by more than 3% between May and December, to finish the year at about -2%; no mean feat considering the magnitude of the crisis the world went through. If the same pattern were to play out this year, GDP estimates would be sitting north of 7% at year-end, given 2021’s 4.1% starting point. Corporate profits, sales revisions, forward guidance, and earnings surprises are all showing signs of an impending (and still underappreciated) economic boom. In fact, S&P 500 earnings are expected to surpass 2019 levels as soon as this year, with double digit growth the year after (and likely again the year after that).

But in the absence (for now) of a lockdown-free consumption market, a slice of the $30 trillion of global stimulus is clearly trying to find a home in financial markets instead. That creates a series of problems: 1) the size of the stimulus is much larger than the size of most markets today; 2) the largest markets in fixed income have minimal levels of income available today; and 3) the markets that do have income are not large. In fact, the $1.6 trillion U.S. high yield (HY) market, as measured by the Bloomberg-Barclays High Yield index as of February 12, is fairly minuscule, or less than a tenth the size, when compared to the $17 trillion negative yielding debt market; measured by the Bloomberg Negative Yielding Debt Index, as of the same date. The need for return, or yield, in this high-growth, high-liquidity environment places today’s sub-4% HY market into perspective.

So, where is all that money going?

Some of the global liquidity that has been injected into the system over the last year is staying as cash for now, to be spent in more traditional ways once lockdowns ease. Vaccine penetration and herd immunity will likely go a long way toward unlocking (no pun intended) this pent-up consumption. The average U.S. household has saved more than $22,000 during the pandemic, equaling more than 31% of realized average income, according to data from the Bureau of Economic Analysis, as of the end of 2020, which is an unprecedented (and likely unsustainable) savings rate. Still this is positive for future consumption potential.

Another portion of that global liquidity has gone into non-traditional consumption, into things that have inelastic supply curves, like houses ( on the more traditional side), but also into things like Bitcoins and baseball cards, the latter two of which are not in any consumption basket. Fascinatingly, 8 of the 10 highest priced baseball card sales occurred in the last 12 months, with a Mickey Mantle card that sold for $2.88 million in April 2018 selling again for $5.2 million just last month (at a 40% annualized inflation rate). Bitcoin’s price is up 455% since the end of 2019, and oceanfront property is inflating at 10% to 15% per year. Indeed, prices are rising in places that are not only unexpected, but in ways that elude traditional metrics like CPI.

Last, but certainly not least, a lot of that global liquidity has gone into stocks, given the ongoing reduction in barriers to entry, information symmetry and in some cases just the sheer boredom of retail investors. Isn’t the Reddit/Robinhood phenomenon just another example of how a large increase in the money supply finds its way into some form of increased prices in the frictionless “CC:All” economy? Pink sheet volumes, call option volumes, and r/WallStreetBets subscriber charts have all had a near-perfect correlation recently – and the top 100 stocks traded on Robinhood have returned almost double what the Nasdaq returned over the last year and almost quadruple the return of the S&P 500. Still, at the end of the day, the equity market is, at least, one that can absorb a few trillion dollars, as evidenced by the record-breaking inflows into equity markets recently ($58 billion in just the week ending February 12), while still offering a free cash flow yield above the yield of the U.S. HY market.

These dynamics move markets, and open the door for opportunities

While the rates market has been going through a pricing readjustment of late, it may still not yet fully appreciate the transition to investment Regime 4. Without a severe Covid-driven double dip, it is hard to bet that the 60% chance of one Fed policy rate hike by 2023 (implied by market pricing, as of February 12, 2021) is too high, meaning that rate-hike convexity is probably to the upside. We are not saying that there will be a hike, could be a hike, or should be a hike, but rather that some outcomes in the distribution are being mispriced by the market, in our estimation. At some point, the financial stability risks that emanate from an extremely low discount rate, coupled with the real economy boom that we expect, could force the Fed’s hand. Nonetheless, we think policy adjustments will be gradual, and in response to spectacular growth, such that dips in risk asset prices (in response to nothing more than policy normalization) should be viewed as buying opportunities.

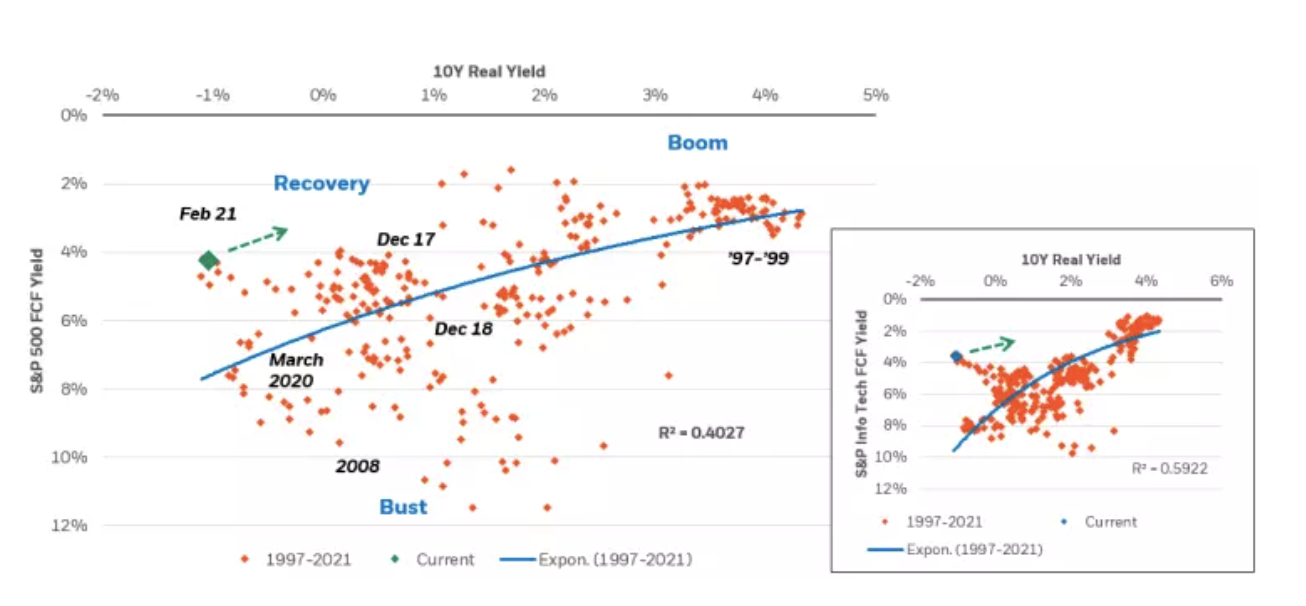

Indeed, some market commentators seem enthralled by the idea that higher real rates should hurt risk assets, but the evidence suggests that there is a dynamic equilibrium real rate for an economy, and for risky assets. Deviations from that equilibrium that are too high or too low can be viewed as a policy mistake, and hurt assets down the capital stack. In October 2018, it was the former that was more likely, yet today it is the latter. Equity free cash flow (FCF) yields have generally been negatively correlated with real rates (see graphs) since the advent of the U.S. TIPS market in 1997. FCF yields are already at their lowest point for the current level of real rates, suggesting that the equity market believes real rates can and should be higher, in line with economic realities (the tech sector, which tends to come under particular scrutiny, shows a similar pattern). The fact is, it is far more important what real rates are responding to rather than the absolute level of rates themselves. Both real rates and policy are likely to be guided by economic outcomes this year, just as they were last March (albeit in the opposite direction).

Equity Free Cash Flow Yields Tend to Be Negatively Correlated With Real Rates

In a higher real rate investment regime, duration can be a tricky hedge for portfolios, as its correlation with equities can be unstable. We think we are getting closer to yield levels where duration can act as a hedge again, but until then, our solution is to use cash as a hedge, which we have written extensively about in recent commentaries, such as: The Queen’s Gambit Declined and The Case for More Cash, Fewer Treasury Bonds. In a nutshell, cash can help reduce portfolio volatility by lowering duration risk, can allow for more risk taking in other parts of a portfolio and can be rapidly deployed should more “Gamestop-like” episodes create investment opportunities as weak hands are forced to liquidate crowded trades.

If financial assets continue to be the primary beneficiaries of past and future stimulus efforts, fears of excessive speculative behavior, in assets like Bitcoin, higher taxes (and wealth redistribution) under the new administration, or the probability of an imminent Fed taper could all come to the fore. It is likely that recent bouts of financial market volatility are not entirely behind us. Still, today’s starting point of 7% real GDP and a -1% real yield means that the return on invested capital for companies (and particularly in the Tech sector), even at marginally higher rates and with the lack of income-producing alternatives, are likely to render these fears greatly exaggerated.

As we contemplate the myriad economic, investment and market cycles facing portfolios today, traveling in directions and speeds that would rival a Brownian motion chart, we cannot help but contrast them with the steady, unflinching rhythm of the Earth’s celestial cycle. The average season lasts about 91 days 7 hours 27 minutes and 15 seconds, with a maximum range of about 4% (or 4 days, summer being about 93 days and winter being about 89 days long). While markets can never, and will never, turn as precisely and predictably as the Earth’s axis, we think we’ve effectively been through a market winter (raising cash in an illiquid panic), a springtime thaw (a recovery in quality assets and duration), and a summertime wave of liquidity that has lifted risk assets to where they stand today (where a risk + cash barbell orientation made sense).

With valuations at elevated levels in some assets, but with tangible upside potential in many others, we think we are now approaching autumn for financial assets, marked by accelerating real economic velocity. We will position for the change in season by being underweight real rates and continuing to shift out of rich high-quality assets and into cash. The really hot days of rapid spread improvement in fixed income are likely over, but the cold days are probably still far enough away for yielding assets, growth and income producing equities and alternatives, such that being overweight risky assets still makes sense.

Investing involves risks, including possible loss of principal. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. It is not possible to invest directly in an index.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks may be heightened for investments in emerging markets.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of March 8, 2021 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Prepared by BlackRock Investments, LLC, member FINRA.

© 2021 BlackRock, Inc. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. All other trademarks are those of their respective owners.

USRRMH0321U/S-1549551-1/9

© BlackRock

Read more commentaries by BlackRock