Key Points

-

China’s growth for 2021 appears strong, but February holds key developments that could impact this outlook.

-

Key developments include stock delistings, trade, and COVID-19.

-

China’s stock market is the best performing in the world so far this year and the country’s economic growth is driving the world’s recovery, so these developments can have far reaching impacts.

The Year of the Ox looks bullish for China with economists and analysts forecasting GDP growth of 8.1% and earnings growth of 18% for the MSCI China Index. But February holds key developments for China that could impact this outlook, including stock delistings, trade, and COVID-19.

Delistings

The NYSE may send valentines to China. The week of February 14 is the earliest that Chinese companies delisted by the NYSE on January 11 can be reviewed for re-listing, removing the trading ban.

At the end of December, the NYSE announced it would delist the U.S. traded ADRs that track the underlying stock listings of China Mobile Ltd., China Telecom Corp., and China Unicom Hong Kong Ltd. to comply with a November executive order by the Trump administration. This came after the Treasury’s Office of Foreign Assets Control designated these telecom subsidiaries subject to the bans on their parent companies identified as Chinese “military companies.” On January 4, the NYSE reversed this decision after talking with regulators. But, after pressure from the Trump administration, the exchange reversed their reversal and reinstated the delistings the following day. Subsequently, index providers including MSCI, FTSE Russell and S&P Dow Jones Indices started to remove companies affected by Trump’s order from their investment products in response to the trading ban. More Chinese companies may be subject to delisting.

How likely are re-listings? President Biden could rescind the executive order at any time. Alternatively, the Treasury, under the new leadership of Secretary Janet Yellen, could reinterpret the directive. Even if this top-down action is not forthcoming, the NYSE could reverse its decision yet again after further review. Delisting was not a term used in the original executive order or its interpretation by the U.S. Treasury. It is believed the intention of the order was to prompt investors to sell the shares of these firms, yet delisting results in the halt of all activity on these securities.

How big of a deal are delistings? The signaling effect of this action on U.S.-China relations is huge, but the impact on actual U.S. trading may not be very significant for key two reasons:

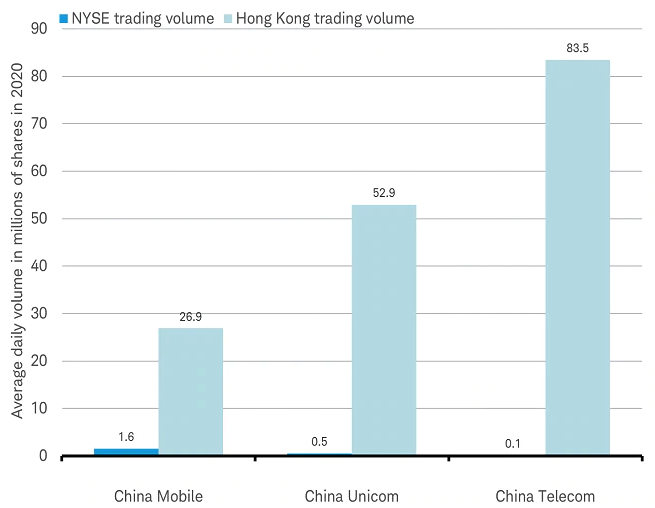

- Average daily U.S. trading in these stocks over the year prior to delisting is a tiny fraction relative to their trading volumes in Hong Kong, as you can see in the chart below.

- On the primary Hong Kong exchange, all three stocks have posted gains so far this year.

Insignificant U.S. listings?

Source: Charles Schwab, Bloomberg data as of 2/15/2021. For illustrative purposes only.

Trade

The World Trade Organization appointed its first female leader on Monday, marking a fresh start to an organization with a renewed focus on China. February could see some announcements of intensions by the U.S. and Europe on the priorities they wish to pursue this year, with China at the top of the list.

One year after the phase one U.S.-China deal began, China’s imports of U.S. goods subject to the agreement are only around 60% of the agreed-upon total for 2020.U.S. tariffs on billions of dollars of traded goods remain in place. Despite these headwinds, China’s trade balance has grown to an all-time high.

China trade balance hits all time high

Source: Charles Schwab, Bloomberg data as of 2/15/2021.

What’s next? Instead of experiencing the start of phase two, the Year of the Ox is more likely to see phase one get phased out. However any reset to the U.S. – China trade relationship may come gradually. A multi-lateral agreement that emphasizes the Biden administration’s focus on labor and environmental standards (above manufacturing jobs and the trade balance that were the priorities of the Trump administration) could take some time.

While announcements by the U.S. and Europe on their priorities may be coming soon, the actual U.S.-China trade relationship may not change all that significantly in the Year of the Ox:

- The U.S. and the European Union may push for changes to World Trade Organization (WTO) rules for developing countries, industrial subsidies and state-owned enterprises. Because WTO reform must be sanctioned through member consensus and China has veto power, any sweeping changes that would derail China’s growth are unlikely

- The 2020 export controls on Huawei and SMIC, China’s largest semiconductor manufacturers, may remain in place.

- The Biden administration appears unlikely to add significantly more tariffs on China.

In conclusion, trade developments are unlikely to pose a significant threat to China’s strong 2021 economic and earnings growth outlook.

COVID-19

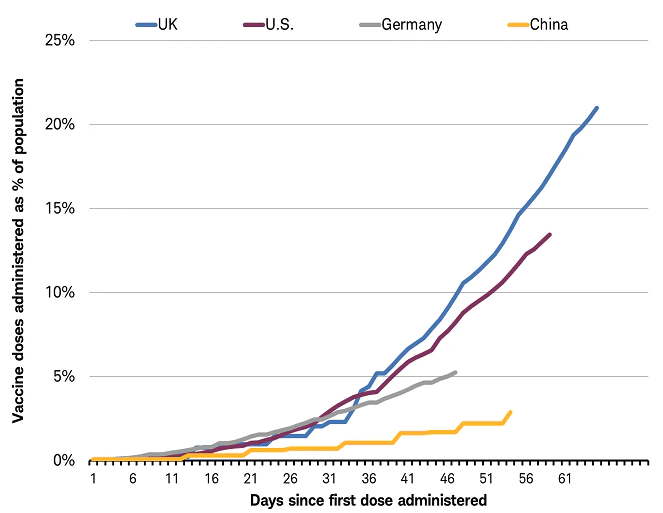

China’s relatively slow rollout of COVID-19 vaccine has been offset by stringent containment of cases using public health measures during outbreaks. While effective, this created little urgency for people to get vaccinated, China’s was the only economy to grow in 2020. Per the latest IMF forecast, it is set for the strongest growth in a decade for 2021 at 8.1%.

China’s slow vaccine rollout

Source: Charles Schwab, Bloomberg data as of 2/15/2021.

Will travel surrounding this year’s February 12 Lunar New Year result in new outbreaks of COVID-19 cases, putting China’s growth at risk? Known as the largest migration in the world, billions of trips across China are logged in the 40-day travel period around this cultural holiday. China’s government is urging people to stay home this year and are requiring testing and quarantines to discourage travel. These initiatives appear to be working. China’s Ministry of Transport estimates travel will be down 61% compared with 2019 and 22% compared with 2020 over the 40-day period.

COVID-19 cases may remain contained, but the lack of travel may also weigh on consumer activity in February, compared to prior years. China’s purchasing managers’ indexes for January showed the economy continued to expand in January but lost more momentum than expected. The slowdown was sharper in services than manufacturing, reflecting an increase in virus containment measures, which affect consumption more than production. Looking ahead, we expect heightened virus risks to dampen growth in the near term, but growth is likely to continue.

China’s stock market is the best performing in the world so far this year and the country’s economic growth is driving the world’s recovery, so these near-term developments on delistings, trade and COVID-19 can have far reaching impacts and bear watching.

Director of International Research Michelle Gibley, CFA®, and Research Analyst-Global Investment Strategy Heather O’Leary contributed to this report.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

© Charles Schwab

Read more commentaries by Charles Schwab