To say the market is bubblelicious is a bit of an understatement given that retail “investment” in call options and penny stocks is quite literally off the charts, dwarfing numbers we saw in 1998-2000. We’ve hit on those worries like a broken record here and here so no need to rehash the argument. What strikes us today is the high price investors/speculators/whoever are willing to pay for “growth”. We suspect price or value isn’t much of a concern these days given the absurdity of dollar flow chasing “high growth” names. It is, after all, a greater fool’s game at the moment. There is no actual intention to hold the “stonks” for the long term, but only to sell them at a higher price to a greater fool who comes into the bubble at a later stage.

For long-term investors though, the calculus just doesn’t add up. Actually, “calculus” is too strong a word. What were talking about here is 5th grade math.

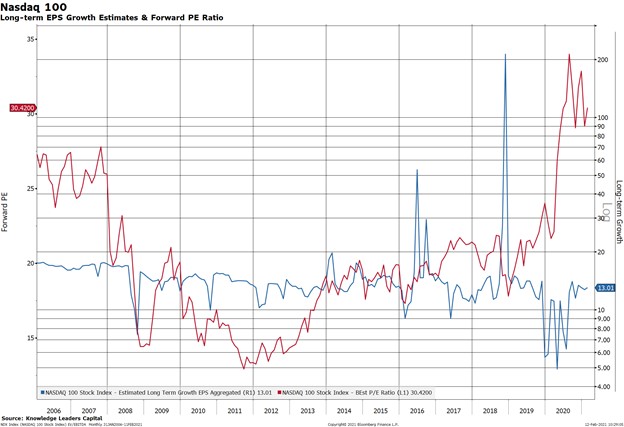

Let’s take the Nasdaq 100 as an example, since it is the stock index with the largest number of “growth” names as constituents. The forward price to earnings multiple on the Nasdaq 100 is currently 30 times. It’s quite clearly above any forward multiple as far back as the data go. The average forward PE over the last 15 years is 19 times. Meanwhile, long-term growth estimates call for 13% EPS growth annually whereas the average over the last 15 years is 15% annually. Already, we can see that the market is applying about a 50% premium for a below average level of growth for Nasdaq 100 companies.

So far so good. Here is where the hard core 5th grade math comes in. Let’s assume forward multiples trend toward the long-term average over the next 5 years and growth comes in right as forecast at 13% per annum. I know, I know. Some of you are yelling at me silently because…rates. There is no alternative, and all that, so valuations will stay elevated forever and ever, amen. I’m sympathetic the argument, but a simple study of longer term valuation trends shows they are mean reverting, eventually. But, I digress. Let’s get back to the 5th grade math.

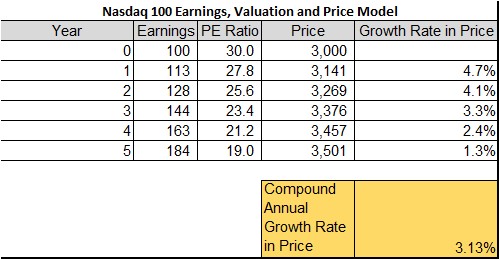

Ok, so let’s assume earnings are 100 today and will grow at 13% annually for the next 5 years. This would put earnings 5 years from now at 184.2, as you can see in the table below. If we assume valuations will fall linearly toward the mean of 19x, then we’d get about 2.2 points in valuation compression each year. Since price is just a function of the PE multiple times earnings per share, the theoretical price would rise from 3000 today to 3500 in 5 years. This would equate to a compound annual growth rate of 3.13%. Yep, that is a positive growth rate and it even exceeds the 1.1% you could earn from a 10-year Treasury bond! If inflation averages 2% over the period, you’d even earn a “real” rate of return of 1%. What value! This without even mentioning that the Nasdaq 100 has an annual volatility between 22%-40%…

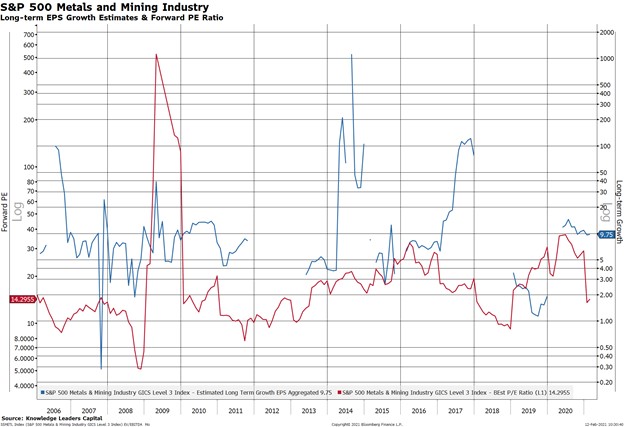

Now, let’s run this same exercise on another investment option, the S&P 500 metals and mining industry. It’s not as sexy as tech stocks. In fact, it’s quite dirty. It’s cyclical as heck too. Some years are blowouts in profits and others in losses. But, it just so happens that forward valuations are actually below the long-term average (14x vs 21x). To be fair, forward growth estimates are below average too (9.75% vs 13%). But, as opposed to paying a 50% premium for below average growth, investors pay a 28% discount in this space.

As a side note, let’s also not forget the big upside potential for growth in metals and mining stocks from one theme alone: renewables. Yes, renewables will be a huge source of marginal demand for raw materials from copper to aluminum to nickel to platinum. So, there is kind of a free embedded call option for this group if policy moves to strongly favor renewables. I’m getting off topic again though, so let’s get back to the 5th grade math.

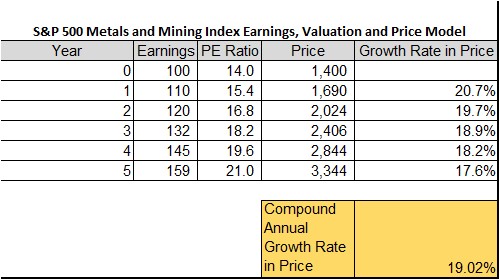

Let’s make the same assumptions as we did above, that forward multiples trend linearly toward the average and growth comes in right as forecast. After 5 years, this would result in a price appreciation of 19% annually. The investor would handily beat Treasury bonds, inflation and…tech stocks.

The moral of the story is…TIA…There Is an Alternative. It’s hiding in plain sight, we just need to remove our kaleidoscope glasses.

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital