IN THIS ISSUE:

1. Overview: 2020 Economy Worst in 74 Years

2. Worst Economic Slowdown Since World War II

3. Fed Again Promises to Keep Rate Near Zero… But

4. President Biden’s Policies to Cost Millions of Jobs

Overview: 2020 Economy Worst in 74 Years

We’ll touch on several bases today. We start with the latest news from the Commerce Department which just released its initial estimate of 4Q economic growth (or lack thereof). 2020 goes down as the worst economic year since the end of World War II.

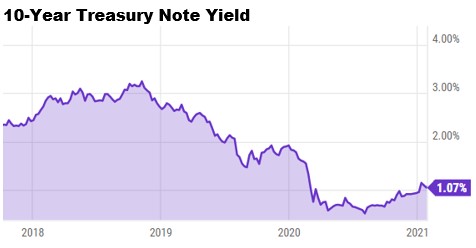

The Fed policy committee met last week and again pledged to keep the Fed Funds rate near zero indefinitely and will continue its monthly purchases of Treasury bonds and mortgages. However, the large gap between the Fed Funds rate and the 10-year Treasury Note remains worrisome. Something’s gotta give, as I will discuss below.

Finally, while President Biden promises his climate change-oriented economic policies will result in millions of new jobs over time, he is obliterating millions of US jobs in the first weeks of his presidency. Whether it’s the Keystone XL Pipeline, halting new oil and gas drilling on federal lands or his climate change initiatives, he is killing millions of US jobs at a feverish pace. Without getting too political, I think all Americans should be aware of what is happening with Biden’s ‘stroke of the pen’ Executive Orders.

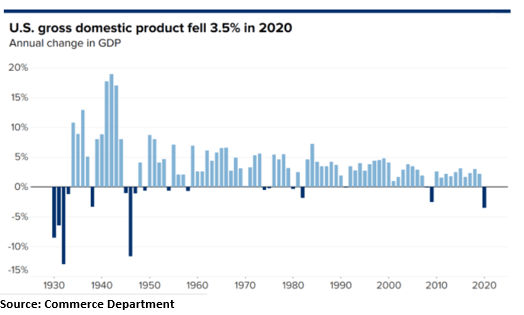

2020: Worst Economic Slowdown Since World War II

Last Thursday the Commerce Department released its first estimate of 4Q Gross Domestic Product showing the economy grew at an annual rate of 4.0% in the final three months of last year. That followed the 3Q record expansion of 33.4% (annual rate) as the economy rebounded strongly following the COVID-19 lockdowns.

2Q GDP plunged by a record-shattering 33.4% (annual rate) following the 1Q slide of 5% in the first three months of the year. For all of 2020 the economy shrank by 3.5%, the worst annual decline in 74 years (WWII).

The pandemic’s blow to the economy early last year ended the longest US economic expansion on record – nearly 11 years. The damage from the virus caused unknown thousands of businesses to close (many permanently), nearly 10 million people remain out of work and more than 400,000 Americans have died from the virus.

The government’s latest GDP report showed consumer spending, which accounts for about 70% of the economy, slowed sharply last quarter to a 2.5% annual gain from a 41% surge in the July-September quarter, when the economy staged a powerful initial comeback.

Last quarter’s economy was instead driven in part by business investment and housing, which has been a star performer during the past year – reflecting record-low mortgage rates and growing demand for larger houses. Housing grew at a sizzling 33.5% annual rate last quarter, and business investment at an impressive 13.8% rate.

Government spending, though, shrank at a 1.2% rate last quarter, after an even bigger 4.8% drop in the July-September quarter. State and local governments have started to resort to layoffs to deal with falling tax revenues during the recession.

The estimated drop in GDP for 2020 was the first annual decline since a 2.5% fall in 2009, during the recession which followed the 2008-09 financial crisis. That was the deepest annual setback since the economy shrank 11.6% in 1946, when the economy was strained after World War II. The government’s report last Thursday was its first of three estimates of growth last quarter; the figure will be revised twice in the coming weeks.

The outlook for the 2021 economy remains hazy. Economists warn that a sustained recovery won’t likely take hold until vaccines are distributed and administered nationwide and another large government-enacted rescue package spreads through the economy – both of which will take months.

On Thursday, the government also reported applications for unemployment benefits declined last week but remained near historic highs at 847,000 – evidence that companies continue cutting jobs as the pandemic is on the rise once again. Before the virus erupted in the United States in March, weekly applications for jobless aid had never topped 700,000, even during the Great Recession in 2008-2009.

Fed Again Promises to Keep Rate Near Zero… But

The Federal Reserve took note of the latest economic threats at its latest policy meeting which ended last Wednesday. The Fed kept its benchmark interest rate at a record low near zero and stressed that it would keep pursuing its low-rate policies until a recovery is well underway.

Keep in mind, however, what I warned about last week: The 10-year Treasury Note yield recently spiked higher and more than doubled from near 0.50% last August to 1.1% this month, as compared to the Fed Funds rate which is 0.00%-0.25%. While the Fed Funds rate is not tied directly to the 10-year T-Note, the Fed has to be very concerned about this development.

The Fed acknowledged that the economy has faltered in recent months, with hiring weakening especially in industries affected by the raging pandemic – notably restaurants, bars, hotels and others involved in face-to-face public contact.

Hiring in the US has slowed for six straight months, and employers shed jobs in December for the first time since April. The job market has sputtered as the pandemic and colder weather have discouraged Americans from traveling, shopping, dining out or visiting entertainment venues. Retail sales have declined for three straight months.

Last month, the government enacted a $900 billion rescue aid package, and President Joe Biden is pushing for lawmakers to follow up by approving his latest $1.9 trillion plan for further economic help. Biden’s proposal has met resistance, though, from many Republicans who contend the cost is too high and some of its benefits are misplaced.

Many economists warn that without further stimulus support, the economy risks succumbing to another recession. They note that much of the aid for individuals from the $900 billion package is set to expire by mid-March.

Mark Zandi, chief economist at Moody’s Analytics, warned last week: “The economy is still struggling. How strong the economy is later this year will depend on how the virus evolves and the effectiveness of the mitigation efforts.” He’s absolutely correct.

The good news is, Zandi predicted the economy will expand at a 4.4% annual rate in the current quarter and achieve annual growth rates above 5% later this year. But he cautioned that his forecast is based on the enactment of further federal economic stimulus relief.

However, Zandi also predicted over 5 million jobs will never return, forcing the unemployed in such industries as restaurants, bars, hotels, etc. to find work in other sectors. I fear this number could ultimately be considerably higher, especially with President Biden’s plan to raise corporate taxes this year. Small businesses have enough to deal with already, without higher taxes.

President Biden’s Policies to Cost Millions of Jobs

Further dashing hopes he would govern as any kind of moderate, President Biden last Wednesday announced plans for what amounts to the “Green New Deal” by another name, at a cost of roughly $2 trillion and millions of jobs.

The left pretends its climate change agenda will boost employment, but the reality is already on display. On Biden’s first day in office, he canceled the Keystone XL pipeline and put thousands out of work immediately. Longer-term, it aborted some 11,000 good paying jobs, mostly for union workers.

Also in his first day in office, the new president ordered a 60-day suspension of new drilling permits for all US lands and water – supposedly to allow for review of the environmental impact. But on Wednesday of last week he made much of that ban permanent, so plainly the science doesn’t really matter.

And there’s more evidence confirming science isn’t mattering a lot to Joe: In the absence of the Keystone pipeline, Canada will still export just as much of its oil – transporting it by less environmentally friendly rail and tanker trucks. What’s green about that? A pipeline has zero carbon emissions.

Economics is out the window, too. The American Petroleum Institute estimates the drilling ban will cost the US economy $700 billion and kill nearly a million jobs by the end of next year. Here too, these estimates may be understated. Never mind this plan will benefit energy competitors such as Russia, Iran, Venezuela and others.

Representative Steve Scalise (R-LA) represents southeastern Louisiana where offshore drilling in the Gulf of Mexico is the lifeblood of coastal communities and funds hundreds of millions of dollars in coastal restoration and hurricane protection projects. Rep. Scalise warned last week that halting offshore drilling will cost at least 48,000 jobs in Louisiana alone by the end of next year.

Then there is President Biden’s Day One decision to rejoin the Paris Climate Accord. The US has reduced its carbon emissions by more than any of the other 195 Paris members in recent years, without being a member. Good job!

There is wide agreement the Paris Accord will mean increasing rules and regulations in the years ahead, which economists agree will eliminate many US jobs. Nevertheless, Mr. Biden wants to be in the club, and he can have the US officially back in on 30-days’ notice (and presumably such notice has already been given).

I’ll leave it there for today. As always, I welcome your comments and suggestions.

All the best,

Gary D. Halbert

|

|

Forecasts & Trends E-Letter is published by Halbert Wealth Management, Inc. Gary D. Halbert is the president and CEO of Halbert Wealth Management, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, Halbert Wealth Management, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. All investments have a risk of loss. Be sure to read all offering materials and disclosures before making a decision to invest. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

|

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management