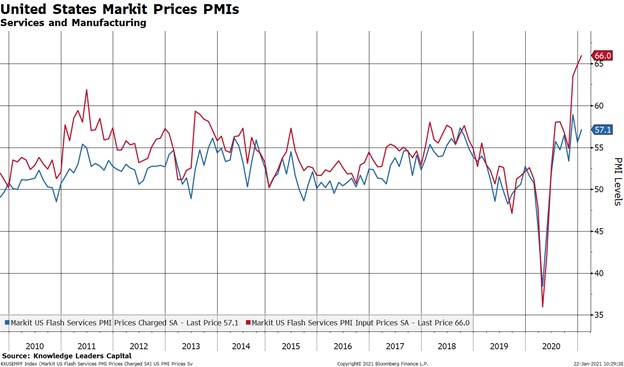

We’re going to keep this post short and sweet because the charts speak for themselves. Today, preliminary Markit PMIs were released for January. Headline numbers ticked up, which is great and shows a continued expansion into the new year. The release also showed that input prices for services exploded higher again, to another all-time high by a wide margin. However, those input prices have not yet fully fed through to prices charged for services. Given the tight relationship between input prices and prices charged, we would expect prices charged to accelerate higher over the coming months. This makes since since service providers will naturally seek to protect their margins.

Moreover, core personal consumption expenditure prices, which is the Fed’s preferred inflation indicator, also appears set to move considerably higher in order to catch up to input prices. This has obvious implications for Fed policy. Does the taper discussion continue? Do expectations for rate hikes get moved forward? Or, does the Fed sit back and watch as prices move to and through their inflation target? They have told us they will do the latter, and we may soon see how strong their commitment is.

The market implications here are pretty straightforward. Tapering is tightening. Bringing rate hike expectations forward is tightening. Allowing inflation to run hot while doing nothing could be seen as de facto easing, which could give even more fuel to the cyclical trade and make those inflation hedges even more attractive.