The year of recovery

Emerging Markets (EM) have undergone their most meaningful and abrupt stress test in recent history and passed, which is testimony to their greater resilience and maturity. 2021 is set to be a period of recovery, with successful vaccination implementation accelerating the trajectory. This is positive for EM economies, corporate earnings and their potential stock market performance.

2020 was characterised by significant divergence as each EM confronted the global pandemic with varying degrees of success. China and North Asia economies led the world in their administration of the crisis, enabling their economies to recover strongly and ahead of most peers, earning the nickname ‘FIFO’.1 Meanwhile, Latin American countries in particular struggled. Their confinement measures were less effective given, in part, large informal labour markets. 2021 should see greater positive convergence as North Asian economies sustain trajectories while laggards reopen and rebound. In the latter case, driven by improved pandemic containment (e.g. India) or strong policy support (e.g. Brazil). As economic growth broadens, it will likewise increase the breadth of investment opportunities.

This unfortunate yet remarkable episode has been unprecedented in many ways. Probably one of the most important facets, especially as we look forward to 2021, is to recognise its ‘directed’ nature. Economies underwent government-mandated lock down and their recovery will also be policy dictated. Rarely has striking the balance between a population’s health and its economic prosperity been so starkly defined. The pandemic’s state of flux means the pace of economic ‘normalisation’ is likely to remain fluid requiring active portfolio management.

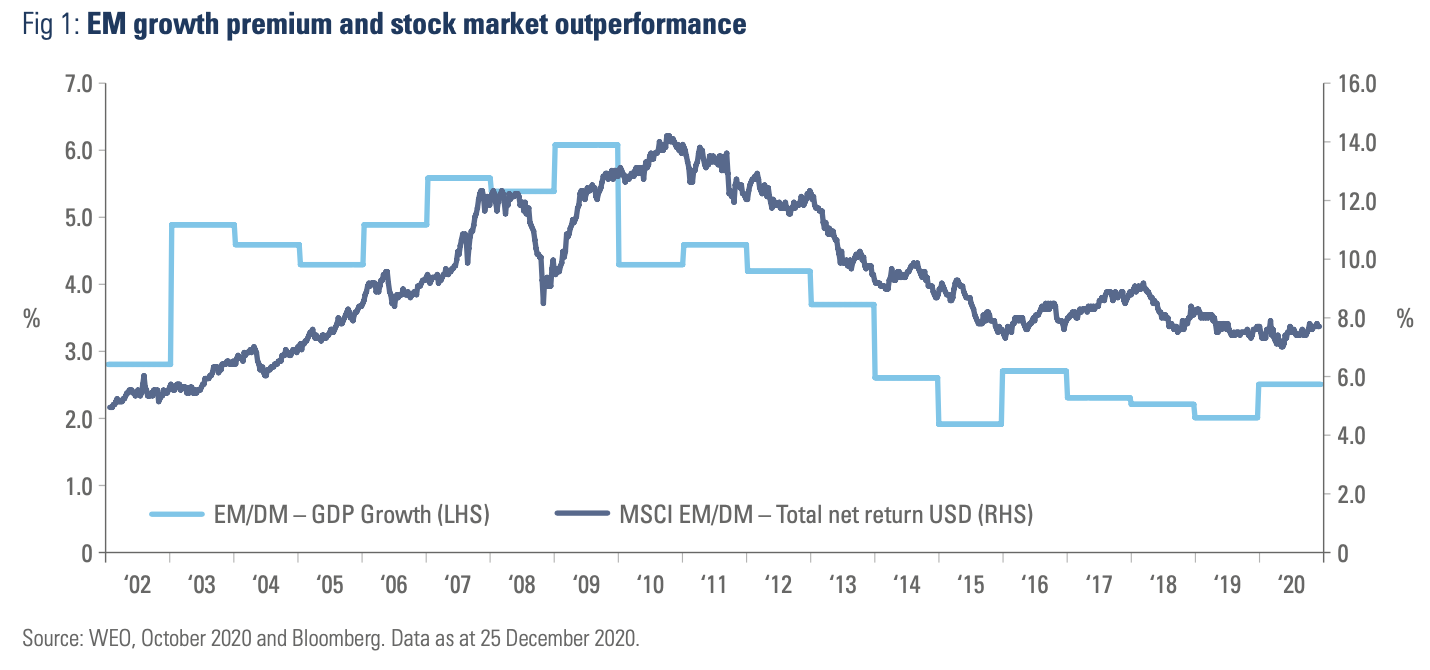

EM economies have overall weathered the pandemic better than developed countries and are expected to lead the global recovery. The IMF forecast EM to rebound from -3.3% in 2020 to +6.0% in 2021. A stronger economic growth path has historically led EM stock markets to outperform developed markets. A tailwind driven by brighter operating environments, capital inflows and local currency support, among other factors.

1 See ‘The triple shock and EM equities: First-in first-out?’, The Emerging View, 2 April 2020.

Global policy floats all boats

2021 will see global monetary policy remain accommodative to the benefit of all. Concerns that such a backdrop will trigger reflationary pressure necessitating tightening measures look premature. The nature of the growth shock, and the degree of uncertainty, mean that policymakers are likely to look through any pick up in inflation to support growth. The monetisation of fiscal policy bears close monitoring. Expanded debt stocks make longer term fiscal dynamics more complex in some countries. Meanwhile, the accommodative policy stance in the US is likely to see US twin deficits reduce support for the US dollar.

Dual ecosystems

China and US policy stances are set to remain sources of market volatility. While a Biden administration is expected to give greater structure to foreign policy, its tone and policy direction are unlikely to change; not least given their domestic popularity and bipartisan support.

The establishment of dual Sino-US ecosystems vying for demand globally is an increasing reality. It already exists in the internet industry (Alibaba/Baidu/Tencent vs. Amazon/Alphabet/Facebook) and the semiconductor industry looks to be on a similar path. While there would be multiple possible ramifications, EM may be a beneficiary in numerous ecosystems given their difficult to replicate technical expertise. EM consumers may also benefit by being coveted by both ‘sides’.

In China, investors should be mindful of steps to moderate stimulus reflecting policy success. Credit growth likely peaked in October at 13.7%, albeit remains high, and short-term credit impulse data has softened. Policy error risk though looks low and recent public announcements have ruled out a (tighter) policy ‘U-turn’. China has recognised the systemic risk that technology giants could bring to the stability of its directed economy. It has responded with increased regulatory intervention, including the suspension of Ant Financial IPO. These steps are positive long term (e.g. ensuring fintech cannot sidestep accountability) although are a likely source of market volatility, and opportunity. The above may reduce the relative attractiveness of China’s technology sector, compared to other areas of EM in 2021, although policy goals around technology advancement and environmental sustainability will trigger opportunities both in and outside of China.

Earnings inflect positively

EM earnings expectations for calendar year 2020 were downgraded to -9%. However, they inflected positively mid-year and the market expects them to rebound to +30% over 2021. By way of comparison, this compares to -16% and +23% for the S&P.2

The positive trajectory for earnings and earnings surprises could prove to be the primary market driver in 2021. Common with other periods of market dislocation, in 2020 EM rerated on the prospect for recovery. The subsequent rebound in earnings has led the MSCI EM price-to-earnings multiple to remain range bound (14 -15x) from end May to year end. This is despite the MSCI EM returning 38%. As 2021 unfolds, we are mindful that EM, like other markets, trade above their long-term price-to- earnings multiples of 12x. This suggests more limited scope for further multiple appreciation.

Meanwhile, the alpha opportunity is only set to expand as growth broadens. The pandemic accelerated and magnified pre-existing structural trends, such as digitalisation/technology and environmental transition, resulting in tight market leadership in 2020. Yet, a combination of greater confidence in the economic recovery, and more attractive valuations, may turn investor heads elsewhere triggering greater breadth of alpha opportunity in 2021.

2 Source. Ashmore, December 2020. Based on market expectations of Net Income growth in USD unweighted by market capitalisation.

Frontier and African Markets primed to catch up

Periods of severe market dislocation often trigger knee jerk investor reactions. This time around is no different. FM stock markets have fallen further and have lagged the broader global market rebound. If the pandemic is bad for developed countries, it must be worse for frontier ones, right?3 This view has little support whether viewed from a societal, macroeconomic or policy perspective. Indeed, FM have generally coped better with the pandemic than developed countries.

This presents an investment opportunity at rarely seen before valuation levels. This includes leading companies that benefit from domestic orientated growth drivers underpinned by low penetration of goods/services situated in economies undergoing meaningful development. The result is sustainably higher return trajectories and attractive long term stock market returns. FM earnings have begun to inflect positively, yet so far absent a corresponding market rerating. Such opportunities should be grasped with both hands, in our view.

3 See: ‘If COVID is bad for developed countries, it must be worse for frontier ones, right... Right?’, Market Commentary, 27 October 2020.