Key Points

-

Risk is often the result of a very high degree of confidence among market participants in one specific outcome.

-

The top five global risks for investors in 2021 are all surprises to the consensus view: problems with the vaccine rollout, geopolitical and trade tensions do not subside, fiscal and/or monetary policy tightens, a “zombie” economy, and interest rate/dollar shock.

-

Having a well-balanced, diversified portfolio and being prepared with a plan in the event of an unexpected outcome are keys to successful investing.

After a powerful rally for stocks for much of 2020, let’s take a look at the biggest potential downside risks for investors in the year ahead. While none of these scenarios make our base case for 2021, a review of the top investment risks in greater depth may be prudent as we enter the New Year.

Hiding in plain sight

History shows us that the biggest risks in a typical year aren’t usually from out of left field (although that sometimes happens, as it did in 2020 with the COVID-19 outbreak). Rather, they are often hiding in plain sight. As goes one of my favorite quotes attributed to Mark Twain: “It ain’t what you don’t know that gets you in trouble, it’s what you know for sure that just ain’t so.” Risk appears when there is a very high degree of confidence among market participants in a specific outcome that doesn’t pan out. So, by identifying the unexpected, here are the top five downside global risks for investors in 2021, in no particular order:

- Problems with the vaccine rollout

- Geopolitical and trade tensions do not fade

- Fiscal and/or monetary policy tightening

- A zombie economy

- Interest rate/dollar shock

Diving into the big five

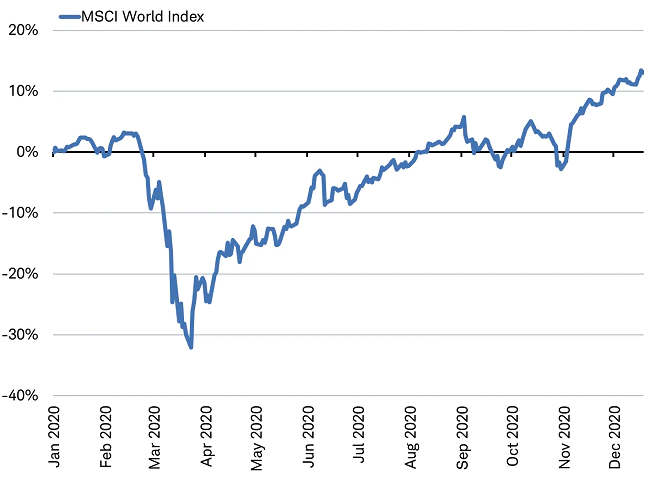

1. Problems with the vaccine rollout. The market has high hopes for a successful and on schedule rollout of the COVID-19 vaccines globally, anticipating a majority of people having been immunized by July for major countries like the United States and United Kingdom. November’s good news on Phase 3 vaccine trials contributed to the strongest month for global equities in over 45 years as markets priced in a more rapid timeline for economic recovery. There is potential for the stock market to pullback some of those gains if vaccine distribution, adoption, or efficacy lags, resulting in delays to the recovery timeline. Bottlenecks with virus testing capacity and turnaround times in both the U.K. and U.S. raise concerns about the ability to roll out widespread vaccination, an even larger operation. Also, we believe the market has not yet discounted the potential return to lockdowns in early 2021 should December holidays result in new waves of cases and hospitalizations, or the potential for the virus to mutate and render current versions of the vaccine less effective.

Vaccine news powered November and December gains

Source: Charles Schwab, Bloomberg data as of 12/18/2020. Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

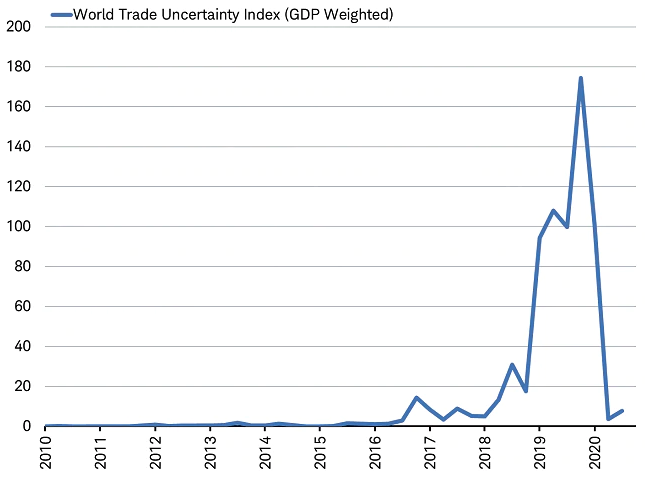

2. Geopolitical and trade tensions do not subside. The market does not anticipate any flare up in foreign policy tension in 2021, following 2020’s plunge in trade policy uncertainty according to the World Trade Uncertainty Index from the Economist Intelligence Unit. Yet, there are hot spots that could spill over into markets.

- U.S. President-elect Biden has made it clear he won’t be easing trade tariffs immediately and intends to confront China on environmental and labor issues in addition to intellectual property rights. China may respond by alerting other countries that new alliances with the incoming Biden Administration against China might prompt retaliation.

- Australia and China have been in low key conflict over the past couple of years, but tensions have now escalated, with the potential for meaningful economic damage.

- Iran’s mid-year Presidential election could see a hardline conservative come to power, hampering any U.S. attempt to return to the Joint Comprehensive Plan of Action to contain Iran’s nuclear ambitions.

- Failure to craft a post-Brexit U.K.-EU trade deal could lead to conflict; heightened by a transition to new leadership in Europe (German elections in the fall and the lead up to the spring 2022 French elections).

- There is the potential for renewed U.S. tensions between North Korea, Russia/Syria, Venezuela, and others with interests in conflict with U.S. goals.

World Trade Uncertainty Index plummeted in 2020

Source: Charles Schwab, Bloomberg data as of 12/18/2020.

3. Fiscal and/or monetary policy tightens. Markets are clearly betting on continued easy policy in 2021. Premature monetary or fiscal policy tightening in major economies could slow the recovery and deal a setback to the stock market. This happened when the global economy emerged from the last recession.

- Fiscal and monetary tightening in the name of austerity following the Great Financial Crisis of 2008-09 contributed to corrections of more than 15% in both U.S. and global stock markets for2010 and 2011.

- The Fed signaled a coming slowdown its QE bond purchases in 2013, causing the “taper tantrum” which sent emerging market stocks down more than 15%.

- More recently, U.S. stocks pulled back by more than 5% in June 2020 as the CARES Act headed for expiration without another program to replace it.

Policymakers are unlikely to tighten policy anywhere near as rapidly following this global recession compared to recent history. But signs of less easing may prompt a market pullback, should policymakers begin to seek ways to contain runaway budgets and balance sheets. This could take the form of discussions of tax increases or lightening up on QE asset purchases.

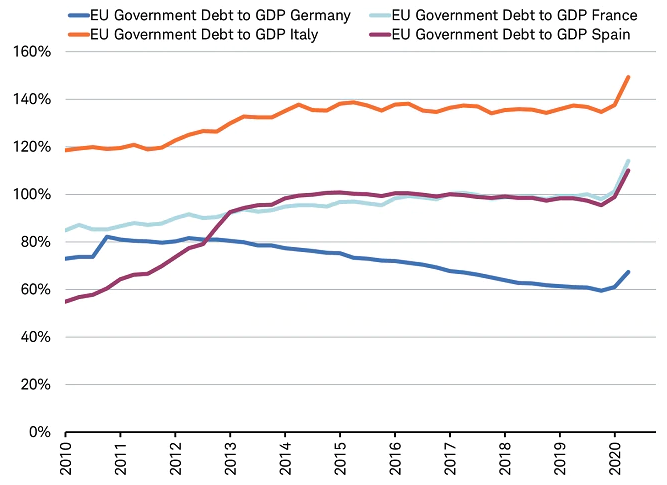

Taxation might come into focus to counter higher government debt

Source: Charles Schwab, Bloomberg data as of 12/18/2020.

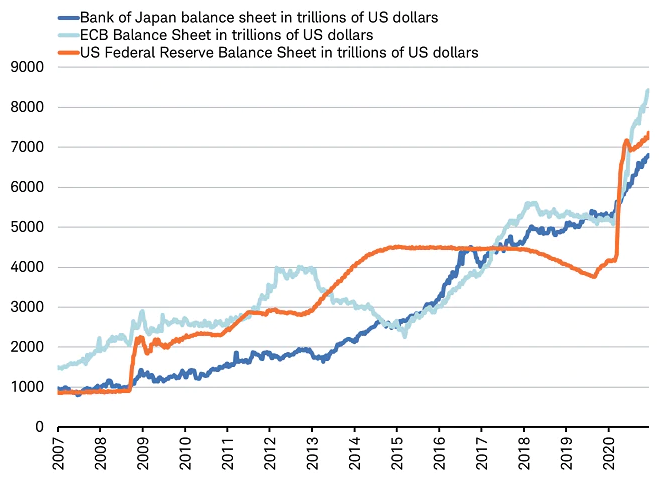

Major central bank balance sheets ballooned 30-70% in 2020

Source: Charles Schwab, Bloomberg data as of 12/18/2020.

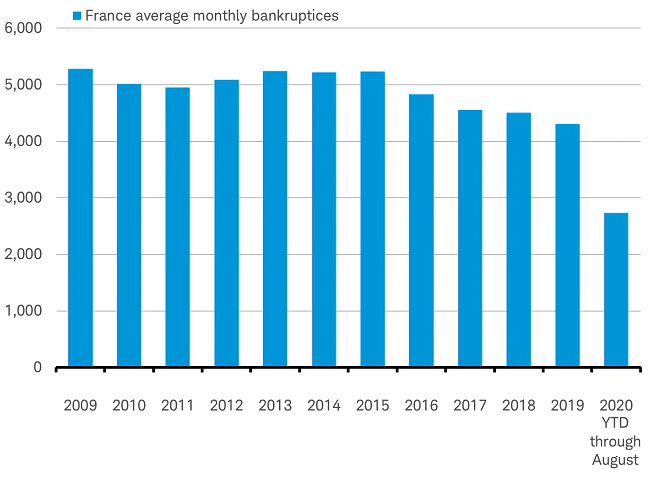

4. Zombie economy. Lingering structural economic impacts from the 2020 crisis and recession could slow the economic rebound. Instead of a quick return to the pre-crisis economy, it is possible we may need a longer period of structural adjustment. Continued easy fiscal and monetary policy could also result in a drag on productivity and growth from hordes of “zombie” companies. About one-fifth of U.S. and non-U.S. companies are considered "zombies," defined as those with income insufficient to cover debt payments. Crisis aid has kept business bankruptcies well below normal levels, meaning companies that would have died off naturally without the pandemic have been kept artificially alive. These companies may use aid to make debt payments rather than fuel economic growth through hiring or spending on equipment.

Thousands of zombie companies kept alive in 2020

Source: Charles Schwab, Bloomberg data as of 12/18/2020.

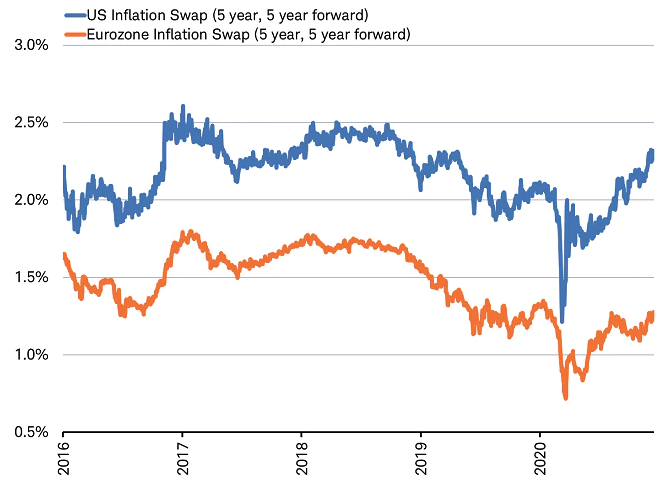

5. Interest rate/dollar shock. An unexpected jump in inflation, surprise surge in bond yields or plunge in the dollar might lead to higher stock market volatility. Inflation expectations have been rising fast, as you can see in the chart below. Any breakout above the five year range may spark tighter financial conditions and prompt investors to reassess stock market valuations.

Inflation expectations have been rising fast in 2020

Source: Charles Schwab, Bloomberg data as of 12/18/2020. For illustrative purposes only.

Be prepared

Whether or not these particular risks come to pass, a new year almost always brings surprises of one form or another. Having a well-balanced, diversified portfolio and being prepared with a plan in the event of an unexpected outcome are keys to successful investing.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Diversification in a portfolio cannot ensure a profit or protect against a loss in any given market environment.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(1220-04CE)

© Charles Schwab

More Alternative Investments Topics >