China’s recovery from the lows of February has been quicker than I anticipated. Stronger-than-expected PMIs and recently reported industrial profits indicate growth is gaining further traction.

China’s economic growth played a big role in the global recovery from the Global Financial Crisis. Now that China has made an impressive recovery, many market participants are expecting other major economies to follow a similar path. However, I see three key differences this cycle that suggest China’s recovery may be on its own trajectory:

1. The size of China’s service sector

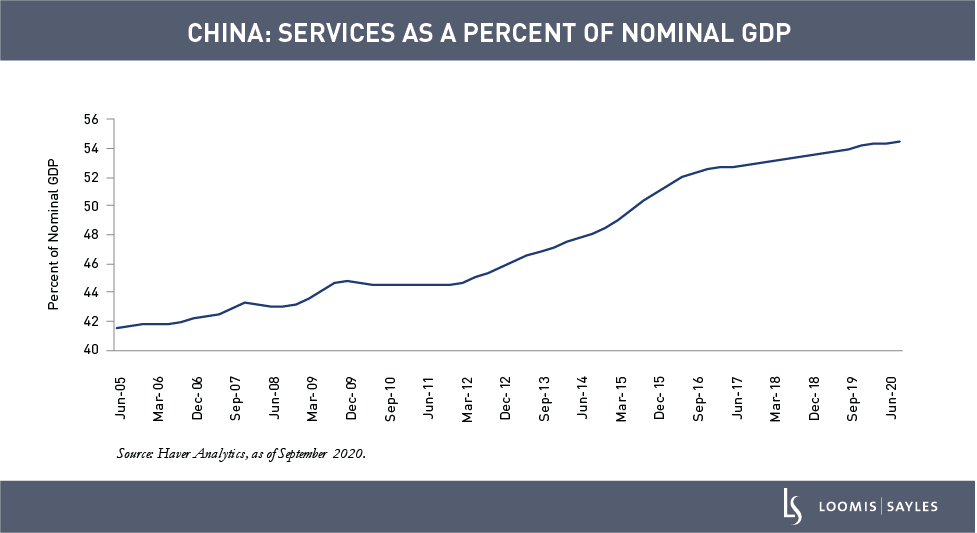

China’s service sector has grown in recent years and increased as a share of total GDP. That said, its service sector remains relatively small compared to other major economies, which suggests it still has plenty of room to grow.

I believe the lift that China can provide to global growth may be smaller this time around due to the increasing share of domestic-oriented services versus traditionally trade-oriented manufacturing activities. Furthermore, because the services sector has been hit particularly hard by the COVID-19 pandemic, countries with larger services sectors are likely to have a different recovery trajectory.

2. Geopolitics

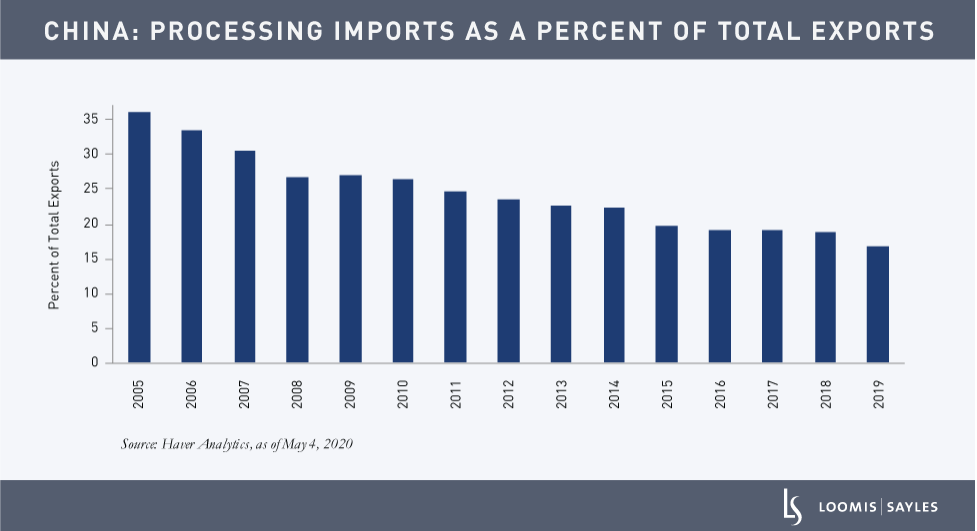

China’s relationship with the US (and other countries, like Australia) has fundamentally changed. While China emphasizes that it will continue to open up its economy, it is increasingly focused on self-reliance, which is reflected in decreasing imports and a growing share of exports from domestically owned firms. I believe this structural shift could reduce the economic boost that China has historically provided to its trading partners. We believe China will continue its long-term plans to achieve self-sufficiency, especially in the technology sector where it aims to produce approximately 70% of semiconductors it uses by 2025.