INTRODUCTION

After a volatile and historic 2020 we are optimistic headed into 2021

2020 was a year of surprises - an unexpected pandemic, a global economic shutdown, the sharpest US recession since the 1930s, and then the fastest ensuing economic recovery in history. Equity markets faced similar volatility with the S&P 500 experiencing the fastest bear market in history, and then the accompanying fastest bull market recovery in history. And yet by late-summer the market was once again in full stride and making new all-time highs, even as the wounds from the global pandemic remained.

Heading into year-end the world (and global economy) faces a difficult winter as the labor market recovery is slowing, COVID cases are spiking, and the sustainability of economic growth is uncertain amid new lock-downs. However, as we turn the corner and enter 2021 our outlook is positive. Much of the uncertainty that plagued markets this year appears resolved (US election, COVID vaccine), and we believe the worst to be behind us. We expect the economic recovery to resume in 2021, with widespread distribution of COVID vaccines the key catalyst.

Our theme for 2021 is “restart”, and with a restart comes optimism and the chance to begin anew. The post-COVID era provides that chance for investors, with both opportunities to capitalize on and challenges to avoid. The combination of COVID vaccines and accommodative monetary policy should help restart latent services sector businesses, while also emphasizing the strength of cyclical ones. At the same time, business models will need to adapt, and so labor market slack may persist into the near-future. Accommodative fiscal policy should provide a safety net for individuals and businesses, and help to soften the drag on the economy as this happens.

For investors, portfolios and investment strategies will need to adapt to the current environment. There will be volatility and bumps along the way as this happens, but for those that are disciplined and able to look past them, we see more opportunities ahead for upside than downside.

Five key investment themes for 2021

Heading into 2021 we expect a pick-up in global economic activity to provide tailwinds for further market upside, but caution that it will likely be a volatile path given COVID-uncertainty. Our five key investment themes discuss how the ongoing recovery is likely to impact the broader economy and markets. Our outlook is highly contingent on the trajectory COVID cases, including a successful global vaccine distribution, as well as ongoing fiscal and monetary policy.

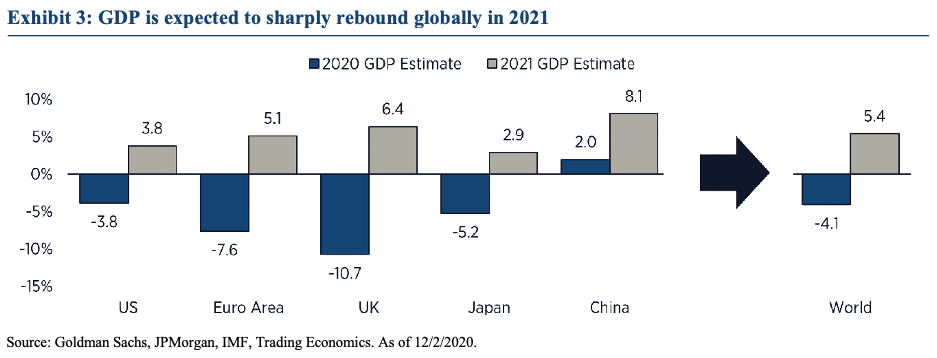

1. The economic recovery will continue, helped by COVID vaccine roll-out

The market recovery in 2020 was impressive and historic, but economic activity still remains well below pre-COVID levels. Specifically, the recovery has favored technology sectors and consumer goods, while services sector (e.g. entertainment, travel, dining) business activity has stagnated. For the recovery to progress a pick-up in services sector activity is essential, which we see as contingent on, 1) stability in COVID case trajectory, 2) the ending of “lockdowns” across cities and counties, and 3) a successful COVID vaccine roll-out.

As the COVID vaccine(s) is rolled out for global distribution, we expect consumer sentiment towards services activities to recover, driving a rebound in leisure spending and further economic expansion.

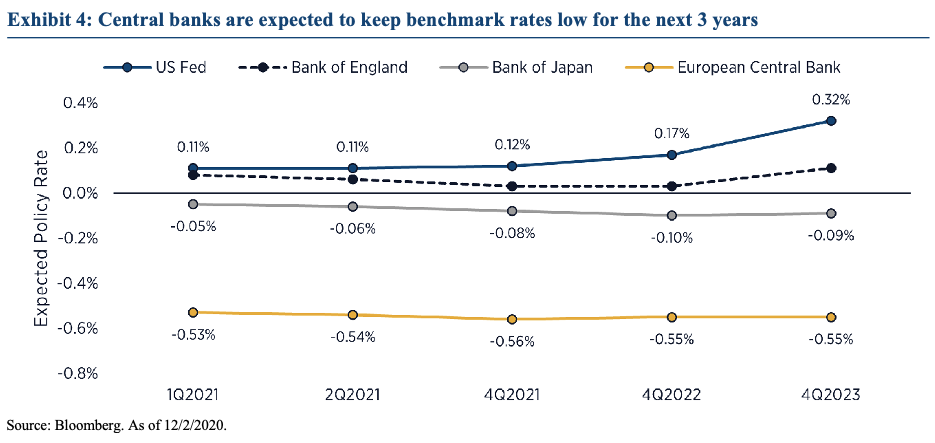

2. Persistent fiscal and monetary policy support should keep markets stable

Heading into the Biden presidency there is uncertainty around the direction of fiscal policy going forward. We expect with Yellen as Treasury Secretary the new administration will favor easing measures, providing additional fiscal support measures to aid the economic recovery.

On the monetary policy front we look for the Fed (and most global central banks) to hold rates low well past- 2021 in support of market stability. The Fed has committed to not raising US rates until inflation averages 2%, and employment reaches maximum levels. And with the availability of the Fed's emergency facilities (if needed), we expect markets to favor risk-on investing, especially equities in cyclical sectors and lower quality credits.

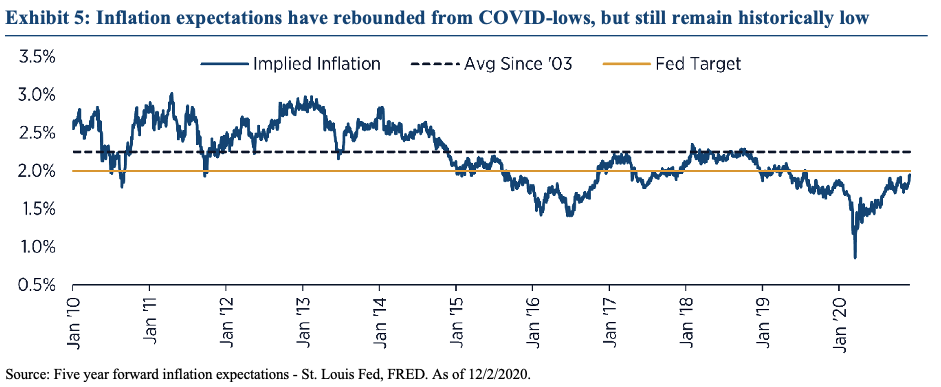

3. Inflation isn’t a concern right now, but could start to pick-up in 2H21

Inflation uncertainty remains prevalent across investors and markets. While inflation expectations (looking out five years) have recovered from their COVID-lows, inflation (and expectations) remain low by historical measures. Near-term with labor market slack prevalent, easing/accommodative monetary/fiscal policy, and the ongoing shift to digitization/remote-work across industries likely to persist, we think inflation catalysts are minimal.

However, as the labor market continues to recover in 2021we think the Fed may start to reduce its use of emergency facilities. In doing so we think markets maybe begin to price in higher inflation expectations which would likely drive yields higher in 2H21 (even as the Fed keeps benchmark rates low).

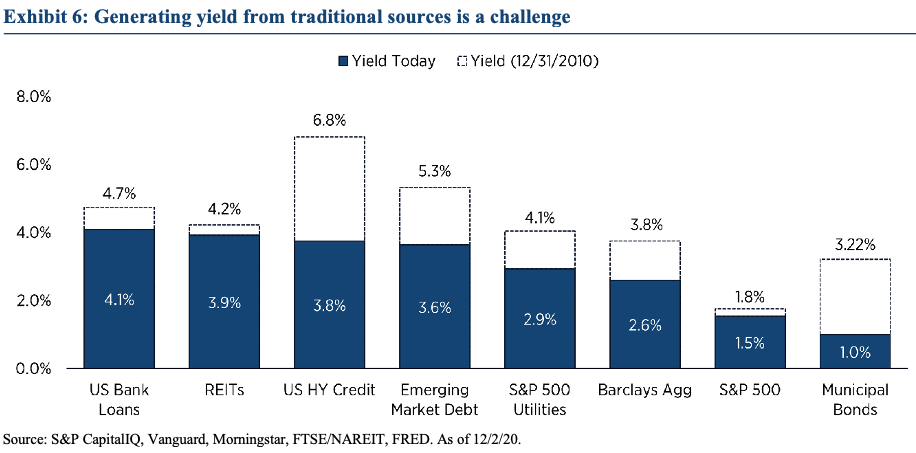

Near-term we see opportunities for investors seeking yield to increase exposure to high yield bonds, while also making strategic allocations to cash flowing real assets such real estate and infrastructure.

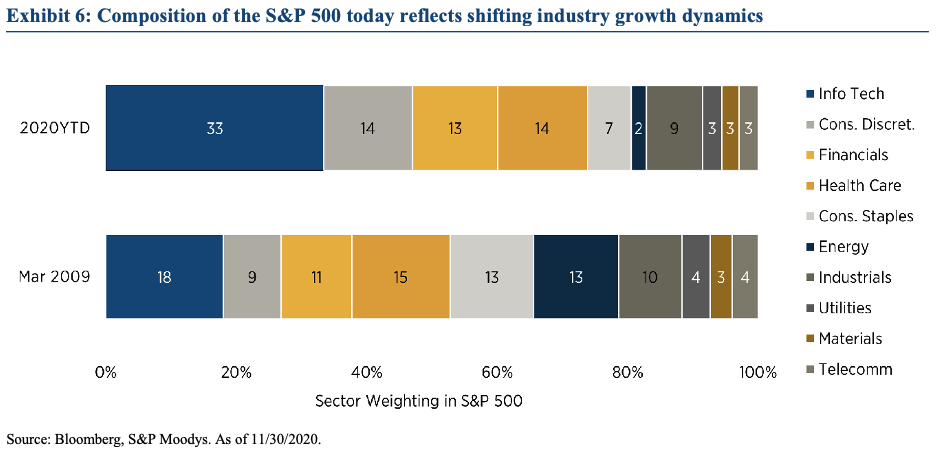

4. Equity markets will likely run higher as economic conditions improve

As the economic expansion broadens in 2021 we expect the equity market rally to continue, but with broader sector participation than in 2020. Specifically, we think services sector businesses will start to experience greater participation in the rally. Cyclical businesses, and especially those more technology focused, will likely still outperform amid consumer and business emphasis on adaptable business models, and those favoring remote/virtual operations.

Shifting composition dynamics within the S&P 500 toward these investor-focused sectors is also likely to provide tailwinds for further market out-performance.

The five largest stocks in the S&P 500 (AAPL, MSFT, AMZN, GOOGL and FB) are all forecast to grow revenues faster than the other 495 names, with similar/better earnings. Furthermore, the combination of a weak USD and labor market slack (as businesses continue to streamline operations) should support corporate margins and drive earnings improvement.

Lastly, we think persistent low rates and a willingness of market participants to pay a premium for consistent topline (and bottom line) growth will help outweigh concerns and potential headwinds over rich valuations.

5. Portfolio yield opportunities exist, but from non-traditional sources

With rates near zero generating sustainable portfolio yield is challenging. Opportunities for yield from traditional fixed income investments (e.g. corporate bonds) is low, but the prevalence of accommodative fiscal/monetary policy is creating opportunities to look at lower quality credits for income needs.

For investors willing to extend credit risk we think US high yield bonds provide compelling opportunities for adding yield to portfolios, both on the corporate and municipal side. Outside of traditional fixed income, non-traditional sources such as hard assets, infrastructure, and private debt (including those with multi-year lock-ups) provide compelling opportunities for yield. These investments are supported by the fiscal environment, which we expect will help reduce the risk of corporate defaults.

In seeking yield it’s essential investors do not blindly add risk to portfolios, but evaluate and understand all investments. Investors must also re-evaluate their own risk profile to determine the risks they’re comfortable taking for income.

Moving forward from here

Investing is a journey. At the beginning of 2020 many investors looked to de-risk portfolios, fearing the uncertainty of COVID and how the economy would recover. And yet by the fourth quarter markets and the economy staged one of the strongest rallies in history.

Successful long-term investing requires having a plan, patience, and the fortitude to remain disciplined. Staying invested and capitalizing on investment opportunities is essential, as is finding opportunities that can consistently perform across economic environments. The market remains volatile, but as the economy restarts there are trends and opportunities to capitalize on for those willing.

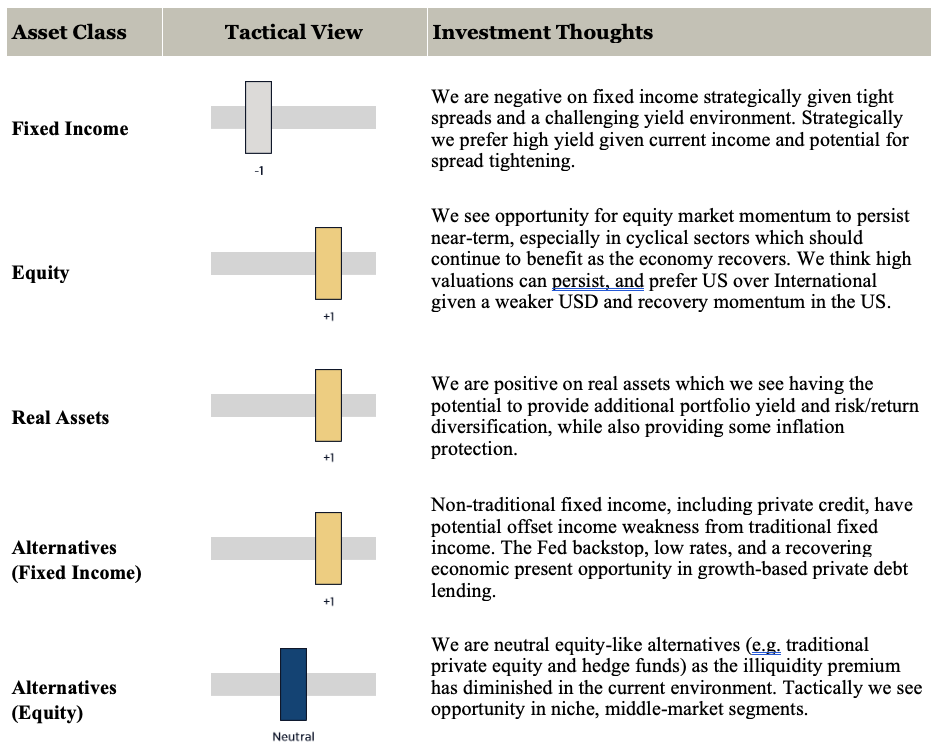

Major asset class views

For 2021 we continue to favor a risk-on tilt across our portfolios. Equity market momentum is likely to persist, driven by technology sector leadership. With interest rates low and the current yield environment unlikely to change near-term, investors requiring yield may need to look to non-traditional asset classes. Real assets and alternatives continue to provide compelling options for income and risk diversification.

ENDNOTES

Disclosures

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This presentation is not intended to be used as a guide to investing, or as a source of any specific investment recommendations, and makes no implied or expressed recommendations concerning the manner in which any client’s account should or would be handled, or warranties regarding investment performance, as appropriate investment strategies depend upon the client’s investment objectives. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance is no guarantee of future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Glossary

MSCI ACWI-All Country World (ex U.S.) Index is a market capitalization weighted index designed to provide a broad measure of global equity market performance excluding the U.S. MSCI EAFE Index is a free float-adjusted market capitalization weighted index designed to measure developed market equity performance, excluding the U.S. and Canada. MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. Russell 2000® Index measures the performance of approximately 2,000 small-cap companies in the Russell 3000 Index, which is made up of 3,000 of the biggest U.S. stocks. Russell 2000® Growth Index measures the performance of the large-cap growth segment of the Russell 2000 Index. Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq. Nasdaq Composite is a stock market index of the common stocks and similar securities listed on the NASDAQ stock market. S&P 500® Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy.

A word on risk

All investments carry a certain degree of risk, including possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-U.S. investments involve risks such as currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. This report should not be regarded by the recipients as a substitute for the exercise of their own judgment. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Investment advisory services provided by Defiant Capital Group LLC, a registered investment adviser.

© Defiant Capital Group

© Defiant Capital Group

Read more commentaries by Defiant Capital Group