A Full Troop of 800-Pound Gorillas: Elections, Taxes, COVID-19, and the Markets

In this letter:

- Without statistical support, political party and tax regime changes have not translated to discernable market performance.

- Global fiscal and monetary stimulus during COVID already far surpass what the world saw during and after the Great Recession.

- Equity and credit markets domestically and abroad continued to shrug off headlines, helping recoup some if not all of the losses from earlier this year.

- Anchored short-term interest rates helped investment grade fixed income yet another quarter.

- For those interested in an election-oriented discussion around financial planning, we are hosting Charles Schwab’s VP of legislative affairs for a virtual non-partisan discussion on the 2020 election on Tuesday October 20th.

We habitually write about the folly of investing based on headlines. Shocks, pandemics, geopolitical upheaval, elections, and the perceived fallout of the aforementioned rarely follow a pre-conceived formula. One does not have to look back far in our history to see how those predictions miss the mark (e.g. last election, initial Brexit news, the Fiscal Cliff, a U.S. downgrade back in 2011, the Greek crises, etc.). All that said, sometimes it is just hard to avoid all of the 800-pound gorillas in the room. It seems like forever ago that we put together a summary right before and right after the last election about what market consensus perceived to be the likely reactions, and what actually transpired. Let us say that the consensus fared poorly.

Now to some statistics (or lack thereof) surrounding upcoming elections. The main issue, and most statisticians would agree, is that our country is too young. There is not a large enough sample size to say what mixture of Democrats and Republicans in the White House and Congress yield better investment returns. That also goes for changing tax regimes. Stealing from something we wrote four years ago; the U.S. did not have income taxes until 1861. They lasted for about a decade, and then taxes again disappeared for over 20 years. At one point they were even declared unconstitutional by the Supreme Court in Pollock v. Farmers’ Loan & Trust Co., 1895, only to come back with the 16th Amendment in 1913. All of this means that we cannot reasonably look at the past for statistical guidance for an average or, a term quite rare these days, for what is “normal”. What follows are more curiosities to help answer concerns than a statistical study.

Both parties often come with aggressive tax increase/cut and spending increase/cut agendas. Yet, this dynamic yielded little in the way of discernable market reaction. For example, Democrats have controlled all three (White House, House, Senate) in 18 calendar years going back to the end of WWII (mostly under Truman, Kennedy, Johnson, and Carter). The most recent was 2009-2010 during the Obama administration. Only three of those years had negative market performance (1962, 66, 77). In fact, the average return in those periods was almost 10% per year. Returns during an all Republican mix have been even better at almost 13% per year. Yet, Democrat and Republican control only happened 27% and 11% of the time, respectively. It may surprise you that under a split government, the markets have averaged a lower number (7.8% per year).

Unfortunately, despite this information being readily available, rational behavior fails to follow. Time and time again we see that investor perception of markets and the economy are directly tied to their political affiliation. In one recently updated paper “Political Climate, Optimism, and Investment Decisions” the authors show that when one’s party is in power, they are more optimistic and willing to put more money into stocks. Not only that, but they also trade less often and are more willing to invest in passive vehicles. When the opposite party is in power, perceptions of uncertainty rise, trade activity increases, and investors look toward more active portfolios that dovetail with their perception of safety and quality. As stock markets historically rise more than two thirds of the time, these decisions can be quite punitive.

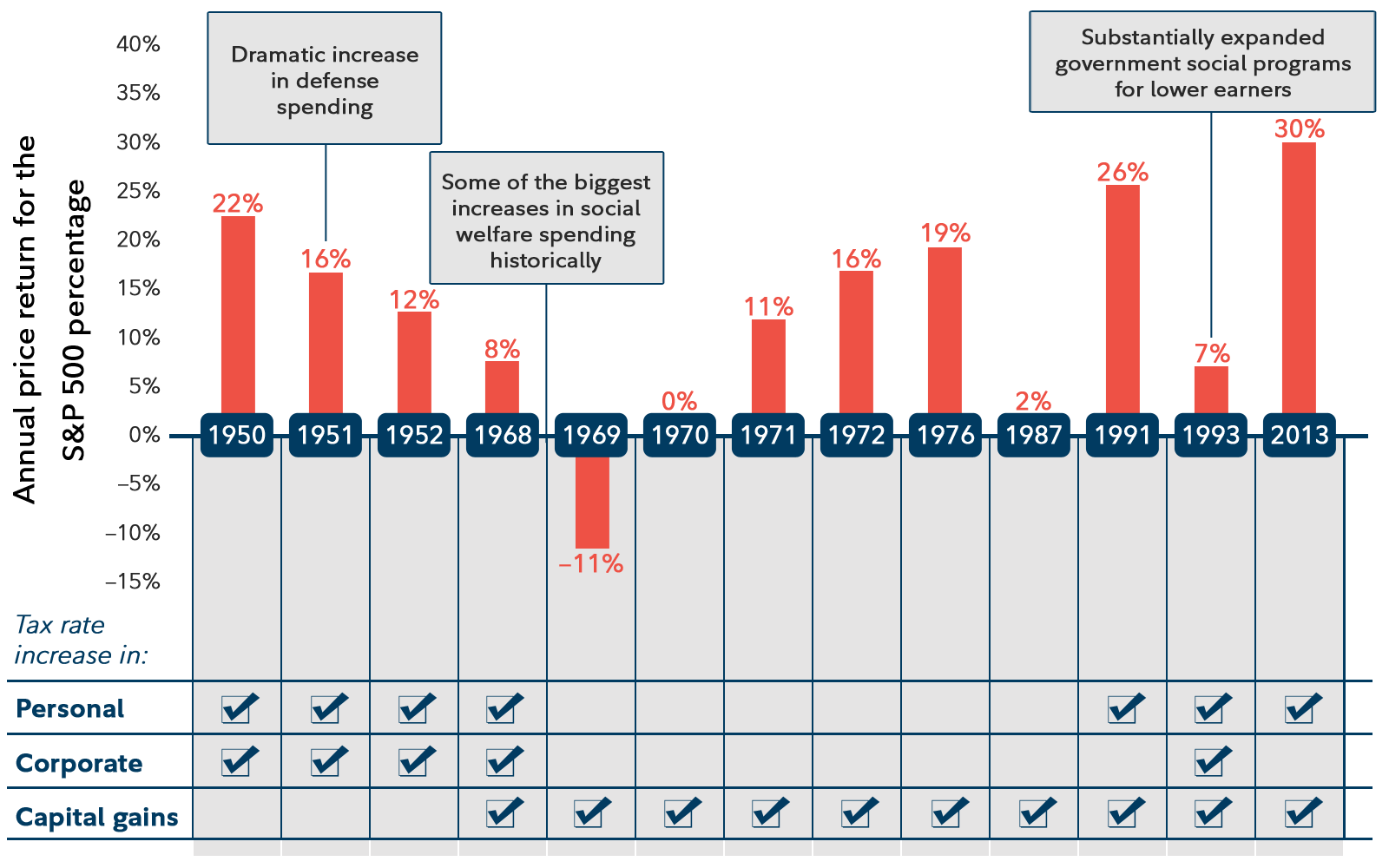

Now to taxes. Hopefully not surprising (given how we frame this missive), market reactions to increased tax rates rarely coincide with expectations. Thanks to the people at Fidelity Management & Research and Haver we have the following chart.

There have been 22 instances of an increase in one or more of these tax rates (personal, corporate, or capital gains) going back to 1950. In all those years, only two had flat to negative market performance (1969 and 1970). The rest (even 1987) were positive years for large cap U.S. equities. On the flip side, in 1981 capital gains taxes were cut from 28% to 20%, and the S&P fell more than 20% in the subsequent twelve months. The short answer is that changes in tax-code historically do not happen in a vacuum. If we take a closer look at any of the past scenarios, some came with a substantial pickup in fiscal spending, others came in times of inflation fears (two before an oil embargo) or some other economic paradigm. In short, one cannot easily tie one to the other.

Source: FidelityThere have been 22 instances of an increase in one or more of these tax rates (personal, corporate, or capital gains) going back to 1950. In all those years, only two had flat to negative market performance (1969 and 1970). The rest (even 1987) were positive years for large cap U.S. equities. On the flip side, in 1981 capital gains taxes were cut from 28% to 20%, and the S&P fell more than 20% in the subsequent twelve months. The short answer is that changes in tax-code historically do not happen in a vacuum. If we take a closer look at any of the past scenarios, some came with a substantial pickup in fiscal spending, others came in times of inflation fears (two before an oil embargo) or some other economic paradigm. In short, one cannot easily tie one to the other

Source: FidelityThere have been 22 instances of an increase in one or more of these tax rates (personal, corporate, or capital gains) going back to 1950. In all those years, only two had flat to negative market performance (1969 and 1970). The rest (even 1987) were positive years for large cap U.S. equities. On the flip side, in 1981 capital gains taxes were cut from 28% to 20%, and the S&P fell more than 20% in the subsequent twelve months. The short answer is that changes in tax-code historically do not happen in a vacuum. If we take a closer look at any of the past scenarios, some came with a substantial pickup in fiscal spending, others came in times of inflation fears (two before an oil embargo) or some other economic paradigm. In short, one cannot easily tie one to the other

Expanding the Room

In past commentaries we touched on the multi-trillion-dollar (i.e. stimulus, lockdowns, etc.) response to COVID. Numbers that large often fail to register, so we want to provide a bit more context. The U.S. has generated trillions of dollars of stimulus this year, but when combined with global central banks and governments, there has been more than $25 trillion in fiscal and monetary stimulus worldwide. This replaces nearly one fifth of annual global GDP.

From an equity market perspective, there are approximately 3,500 companies in the Wilshire 5000 index (a proxy for all publicly traded U.S. equities - tells you something about how things have changed that only 3,500 names remain). Twenty-five trillion dollars would buy the equity of pretty much everything except for the top 10 names. That’s with two quarters worth of stimulus, and there seems to be more on the way. There is also a non-market way of looking at this (that is important since almost half of the people in this country do not own any stock). U.S. stimulus alone may end up being north of 40% of our GDP. Median household income has actually increased as a result. According to a recent report, over a 180-day window, median household income went from $180 per day to $246 (that is after we account for lost daily income of more than $20 per day). That means the median family was making 37% more than before. We cannot come close to comparing that to the response in the midst of the financial crisis where, even after stimulus, household income didn’t get back to the pre-crisis peak.

Add to all of this a commitment to keep short-term interest rates effectively at zero for at least another three years (markets are pricing in longer), and you have a somewhat altered state of operations where it becomes progressively harder to value assets or look for historical parallels. For a long time, markets have operated under the paradigm of bad news = good results (i.e. more stimulus coming). When faced with the question of how the markets continue to be so resilient in the midst of a recession and everything else going on with COVID, at least some of the answer may lie in the data above.

Markets

-

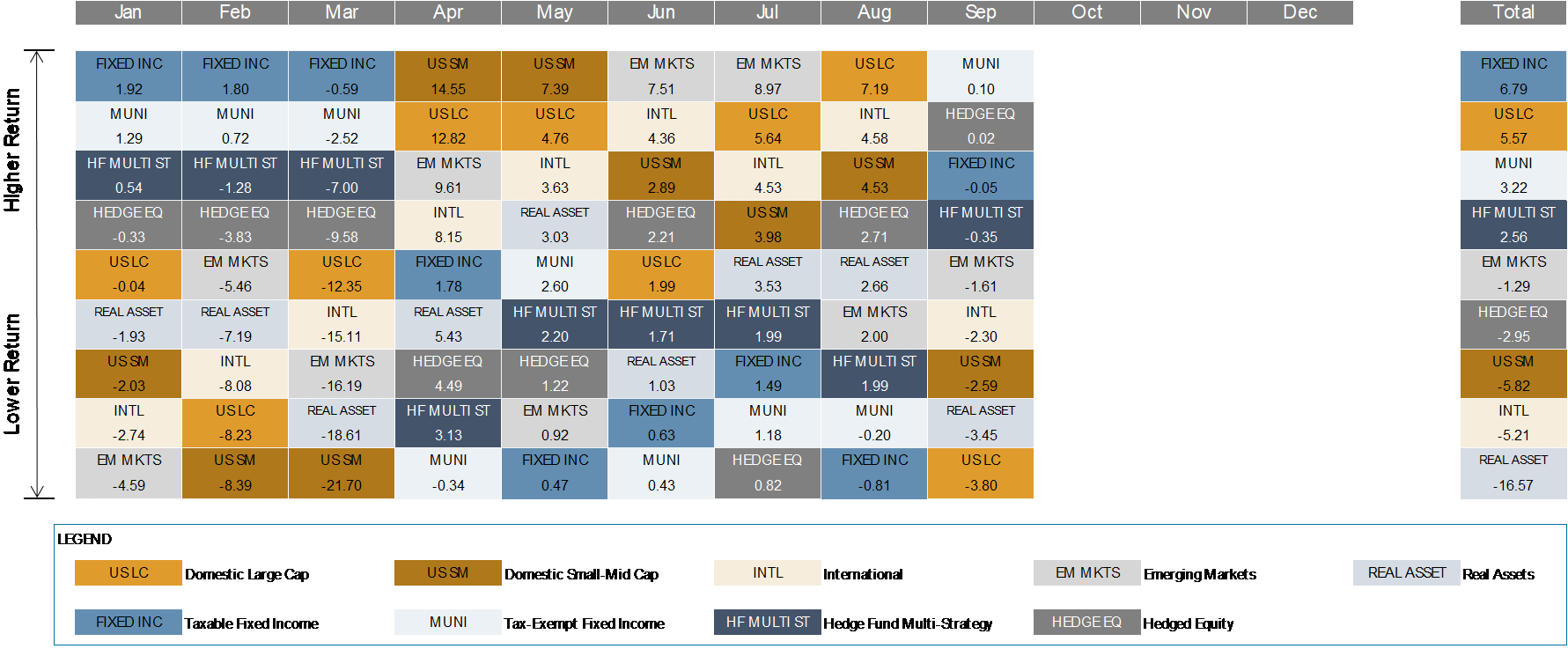

- Equity markets continued where they left off in Q2, recouping a good portion of the losses from earlier this year. One concern we hear often is the narrow leadership in large cap technology stocks at the cost of the rest of the market (the S&P 500 is up 5.6% but an equal weighted version is down 4.8% this year). Although there is definitely truth to that, there is also the reality that these companies are generating a lot more earnings than the often drawn parallel to the tech bubble. Then, technology stocks made up more than one third of the S&P but generated only 16% of the earnings. Today they are 28% of the S&P but generate nearly 24% of the earnings.

- U.S. small-mid cap markets along with markets overseas also recovered somewhat, but at the index level they remain down year-to-date. Much of the rebound is consistent with perceived COVID impact. Technology-heavy and less economically sensitive industries are doing well, as are the countries that have been able to keep COVID cases down. Case in point, China, despite all the headlines of trade and U.S. relations, is up more than 15% year to date.

- In fixed income, credit markets continued to rebound despite rising defaults, as many borrowers were able to tap the corporate credit markets over the summer to extend debt walls. Municipal bond volatility abated even more, with new issuance and central bank backstops aided by renewed demand for tax-free income.

Last Note on Taxes

We recently put out a note on the variations of the tax proposals currently on tap (find it here). We do not know what the probability of a tax regime change is in the current environment, and we may not know for many months after the election. That does not mean that one should stay idle. It is always important to be aware of realized gains or losses coming into year end, and how one’s tax situation can evolve in the coming months and years. As we mentioned in the piece, it is never too early to start evaluating the proposals being put forward, modeling potential outcomes, and planning appropriate action. Doing this can be done without the aforementioned knee-jerk investment decisions.

Wealthspire Advisors is the common brand and trade name used by Sontag Advisory LLC and Wealthspire Advisors, LP, separate registered investment advisers and subsidiary companies of NFP Corp.

This information should not be construed as a recommendation, offer to sell, or solicitation of an offer to buy a particular security or investment strategy. The commentary provided is for informational purposes only and should not be relied upon for accounting, legal, or tax advice. While the information is deemed reliable, Wealthspire Advisors cannot guarantee its accuracy, completeness, or suitability for any purpose, and makes no warranties with regard to the results to be obtained from its use. © 2020 Wealthspire Advisors

Read more commentaries by Wealthspire Advisors

Source: FidelityThere have been 22 instances of an increase in one or more of these tax rates (personal, corporate, or capital gains) going back to 1950. In all those years, only two had flat to negative market performance (1969 and 1970). The rest (even 1987) were positive years for large cap U.S. equities. On the flip side, in 1981 capital gains taxes were cut from 28% to 20%, and the S&P fell more than 20% in the subsequent twelve months. The short answer is that changes in tax-code historically do not happen in a vacuum. If we take a closer look at any of the past scenarios, some came with a substantial pickup in fiscal spending, others came in times of inflation fears (two before an oil embargo) or some other economic paradigm. In short, one cannot easily tie one to the other

Source: FidelityThere have been 22 instances of an increase in one or more of these tax rates (personal, corporate, or capital gains) going back to 1950. In all those years, only two had flat to negative market performance (1969 and 1970). The rest (even 1987) were positive years for large cap U.S. equities. On the flip side, in 1981 capital gains taxes were cut from 28% to 20%, and the S&P fell more than 20% in the subsequent twelve months. The short answer is that changes in tax-code historically do not happen in a vacuum. If we take a closer look at any of the past scenarios, some came with a substantial pickup in fiscal spending, others came in times of inflation fears (two before an oil embargo) or some other economic paradigm. In short, one cannot easily tie one to the other