Despite the worst economic and health crisis in generations, U.S. consumers are defying the pessimists.

Online commerce continues to surge while the pickup in consumer spending has broadened to include more traditional categories, notably autos and housing. As spending has rebounded so have consumer stocks. Third-quarter gains in the global consumer discretionary sector have been led by internet commerce companies, but other industries have also rallied, most notably home improvement, general merchandise retailers and home builders.

While the fading possibility of additional fiscal stimulus is a risk to future consumer stock gains, we see three factors that could offset this risk and support future growth:

- Lower household debt. Household debt as a percentage of disposable income remains at a 20-year low while debt servicing costs have never been lower. Meanwhile, net worth is supported by both a rising stock market and a housing rebound.

- Snapback in jobs. The unemployment rate fell from a peak of 14.7% in June to 7.9% in September. While we believe that the labor market is going to heal slowly from here, the snapback in the last 3 months has been very strong.

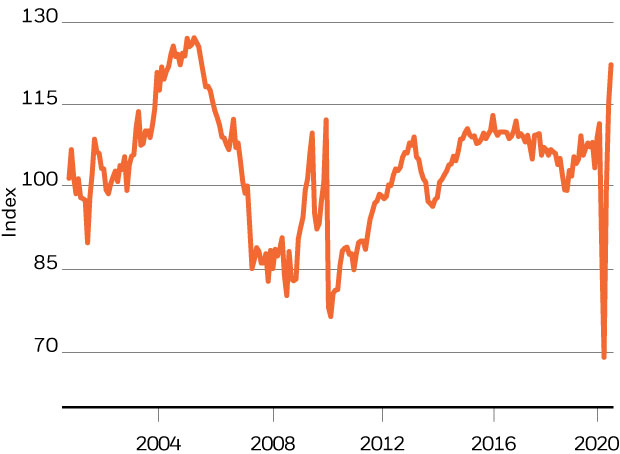

- Housing surge. Record low mortgage rates and a renewed interest in home ownership and suburbia has fueled a recent surge in housing. The below chart illustrates the sharp increase in pending home sales.

A sharp increase in U.S. home sales suggests consumer strength

Pending Home Sales Index