Emerging markets have had different approaches to coping with COVID-19 and are at different stages of recovery. Our emerging markets equity team examines trends, news and data shaping emerging markets in the third quarter, and shares its latest outlook.

Three Things We’re Thinking About Today

-

Brazil has been among the hardest hit by the COVID-19 pandemic, just behind the United States and India in the number of reported cases. However, we have started to see the number of new cases in Brazil start to decline. Ironically, we believe that the government’s decision against implementing a country-wide lockdown at the onset of the pandemic has reduced the likelihood of a second wave. Heavy government spending and monetary policy easing have helped bring some stability to the economy. Moreover, Brazil has continued to implement key reforms despite political noise. In terms of investment opportunities, we continue to favor the financials sector, especially companies with strong capital market exposure. Interestingly, Brazil’s stock exchange itself has a strong sustainability agenda, while environmental, social and governance (ESG) principles are not only implemented within the exchange itself, but also promoted in the Brazilian stock market broadly. E-commerce is another exciting investment theme, with several large players competing in the online space. As in other countries, the COVID-19 crisis has accelerated the adoption of internet-based retailing in Brazil. Despite continued uncertainties, our view on Brazilian equities is generally positive.

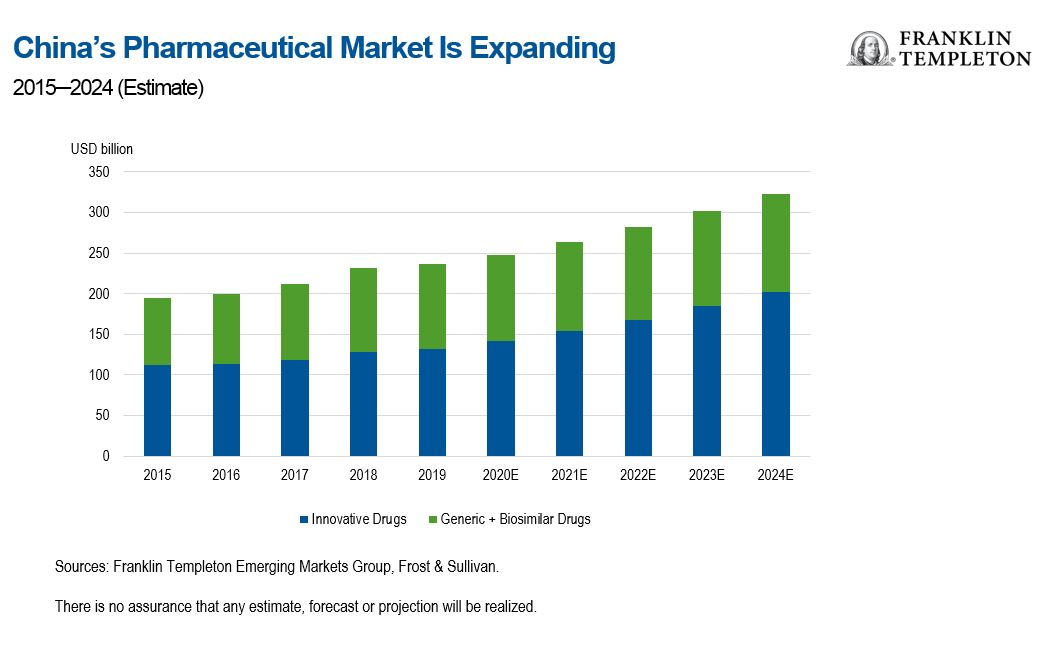

- The COVID-19 pandemic has underscored the importance of health care in China, reinforcing existing structural trends that could drive a new wave of innovation in the country. Multiple factors are propelling domestic drug and medical device development including rising health care demand, an aging population, growing lifestyle diseases and rising income, coupled with government efforts to strengthen the health care system. In addition, the growing numbers of overseas-educated Chinese scientists and entrepreneurs returning to the country constitute an abundant pool of homegrown talent. We see greater long-term potential in innovative drug makers with strong portfolios or pipelines of treatments, compared with generics companies that are likely to face price pressures from government reforms. Some Chinese biotech firms have shown remarkable speed in bringing novel treatments to market. Companies in the pharmaceutical outsourcing industry also show promise. Meanwhile, we also see examples of innovation in medical equipment makers—leading domestic suppliers, which already have a cost advantage over foreign competitors, whose growth could be encouraged on the back of government policies supporting localization. We think these companies reflect a new breed of innovative enterprises that could transform health care outcomes in the years ahead. Together with flourishing capital markets, favorable policies and motivated talent, a vibrant ecosystem is potentially taking shape.

-

Company engagement remains a crucial part of emerging market (EM) investing. Bringing about better corporate behavior and a better understanding of companies’ responsibilities toward all stakeholders are efforts we continue to push in our stewardship of client capital. The tone of engagement in EMs has shifted in recent years: companies that formerly took a narrow, hard-nosed approach to returns are adopting more accommodative measures. In countries such as South Korea, South Africa and Brazil, companies are placing more emphasis on ESG issues. We have seen leading companies in South Korea publicly apologize for governance missteps and manage their balance sheets more effectively through returning capital to shareholders. ESG reporting has become mandatory in some countries, a trend we expect to continue elsewhere. The ESG conversation is changing further amid the COVID-19 pandemic, with a greater focus on the social impact of policies. Many governments are supporting jobs, while companies are more cognizant of the reputational risks of layoffs. ESG has become more important, with companies considering it critical to sustainable business performance. In our view, this “delta” of improving ESG in EMs is a further tailwind supporting the secular outlook for the asset class as the world emerges from this crisis.

Outlook

The market had expectations for greater normality into the final quarter of 2020, but with rising COVID-19 cases in Europe and select countries globally, it is evident the virus will persist. As a result, policymaking looks to remain reactive. A silver lining is that these countries have not seen a corresponding jump in mortalities, reflecting improved treatments and wider testing to reveal asymptomatic cases. Despite one of the most stringent and comprehensive lockdowns globally, India could not prevent a late surge in COVID-19 cases and has surpassed Brazil as the country with the second-highest number of cases in the world, behind the United States. However, given that mortality has been contained with daily deaths declining markedly since the peak, the Indian economy continues to reopen despite the surge in cases.

We expect a continuation of the current political, economic and market environment in EMs until a vaccine is widely dispensed or herd immunity achieved, with results and outcomes varying widely by country. In these circumstances, a recovery is likely to be far shallower (taking far longer) and volatile (in response to stop-start policy) than the steep declines earlier in the year. Governments have already spent enormous amounts of money, but many businesses continue to shut down as lockdowns and other policies restructure economies.

US-China relations have been steadily deteriorating and the political jostling in the lead up to the US presidential election could result in more noise and negative policy developments in the interim. Market volatility could continue, especially if the election results are disputed. In any event, we expect both US political candidates to maintain pressure on China. We also expect the ongoing US-China trade and technology conflict to place continued pressure on supply chains, resulting in more localization and reshoring.

The information technology and communications services sectors have been exceptionally resilient, a trend we expect to continue amid the current environment. We expect EM leadership and growth to continue in various areas such as semiconductors, online gaming and fifth-generation wireless technology (5G) deployment.

Emerging Markets Key Trends and Developments

EM equities rose over a volatile quarter and pulled ahead of developed market stocks. Post-lockdown economic upturns, continued policy dovishness, and progress in coronavirus vaccine trials fueled an initial rally, but it unraveled amid fresh COVID-19 outbreaks and heightened US-China tensions ahead of the US presidential election. EM currencies broadly strengthened against the US dollar. The MSCI Emerging Markets Index increased 9.7% during the quarter, while the MSCI World Index returned 8.0%, both in US dollars.1

The Most Important Moves in Emerging Markets in the Third Quarter of 2020

- Emerging Asian equities outshone broader EMs with a sharp advance over the quarter. Markets in Taiwan, India, South Korea and China soared on the back of strong investor interest in technology heavyweights. In India, better-than-expected corporate results also cushioned the market against COVID-19’s sustained spread. China’s economic recovery broadened, though escalating US restrictions against Chinese technology companies sparked caution. Bucking the regional uptrend, stocks in Thailand, Indonesia and the Philippines fell. Cabinet resignations and anti-government protests in Thailand fed political uncertainty. Indonesia reintroduced mobility restrictions in its capital to combat rising COVID-19 infections.

- Latin American equities saw broad declines for the quarter despite a strong July, partly due to weaker domestic currencies. Political noise and worse-than-expected second-quarter gross domestic product (GDP) data weighed on sentiment in the Brazilian market. The government also unveiled the first phase of its administrative reform and extended monthly emergency aid to support those impacted by lockdown measures, while the central bank lowered its key interest rate to a record low of 2.0%. Mexico, however, ended the quarter with positive returns, largely due to a stronger peso. The Central Bank of Mexico also cut its key interest rate by 0.75%, bringing borrowing costs to their lowest level in four years. A gradual resumption of economic activity and a recovery in business expectations supported confidence in Peruvian equities.

- In the Europe, Middle East and Africa region, European markets underperformed their Middle Eastern and African peers as a resurgence in new COVID-19 cases led to a tightening of quarantine measures in several economies in Europe. Lower oil prices, geopolitical worries and a depreciation in the ruble offset the development of a COVID-19 vaccine and better-than-expected second-quarter GDP data to push Russian equities lower. Elsewhere, the South African government continued to ease COVID-19 restrictions, opening the country for domestic travel, with plans for international travel to resume in October. The central bank cut its key interest rate by 0.25% to a record low of 3.5% in July before leaving the rate unchanged at its September meeting.

Regional Outlook

Scroll over the map to view comments on the countries indicated and our sentiment.

Green = positive, Red = negative, Blue = neutral

The graphic reflects the views of Franklin Templeton Emerging Markets Equity regarding each region and are updated on a quarterly basis. All viewpoints reflect solely the views and opinions of Franklin Templeton Emerging Markets Equity. Not representative of an actual account or portfolio.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security. Past performance does not guarantee future results.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

1. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

© Franklin Templeton

Read more commentaries by Franklin Templeton