A growing narrative today is that the financial markets are not correctly priced for the dour “realities” of a real economy that is crippled by the ongoing pandemic. Indeed, on the heels of an historic risk-asset rally from March’s peak panic, it appears on the surface that nothing is truly cheap anymore, leaving many investors wondering “what are my alternatives?” Our response to that? “Exactly.”

We need an alternative(s) plan to generate returns for the rest of 2020 and into 2021. We’re convinced that durably robust total returns can be achieved by establishing a barbell-styled portfolio, through positioning tactically in pockets of mid-quality income-producing assets, by holding some equity risk, by allocating to alternative asset class supplements, and by holding generous levels of cash, along with an anti-fiat currency, like gold. Our plan rests on both understanding the critical facts that are influencing where cash-flow driven asset markets are heading, as well as comprehending how today’s market myths can lead investors astray and how to avoid those missteps.

Myth: The disconnect between stock market strength and economic uncertainty is a conundrum.

A tremendous amount of ink has been spilled discussing the supposed quandary of the equity market’s robust recovery, while at the same time economic improvement has been more uneven and uncertain. At the heart of this misunderstanding is an apples-to-oranges comparison: the fact is that the stock market and the economy, while connected, are two distinct entities. Indeed, they can even move in opposite directions.

As a case in point, the correlation between domestic corporate profits and GDP growth collapsed in the 1990s and has hovered near zero for the past three decades. Further, in today’s environment, the industries that have been most adversely affected by the pandemic lockdowns (hotels, restaurants, leisure, airlines) hold an outsized impact on labor markets, but a relatively minimal influence over financial markets. And at the same time, those firms that hold the greatest weights in major market indices also tend to employ relatively fewer people than did the top firms several decades ago.

None of that is to ignore the genuine economic pain being felt by many small businesses, which are truly struggling through this period with massive revenue and employment losses, but those firms are not the same as those in the major equity indices. Finally, many commentators dramatically underestimate the impact of monetary and fiscal support.

Fact: The historic marriage of U.S. monetary and fiscal policy, in response to the pandemic, will provide a powerful and persistent financial economy tailwind; ultimately offsetting near-term economic duress.

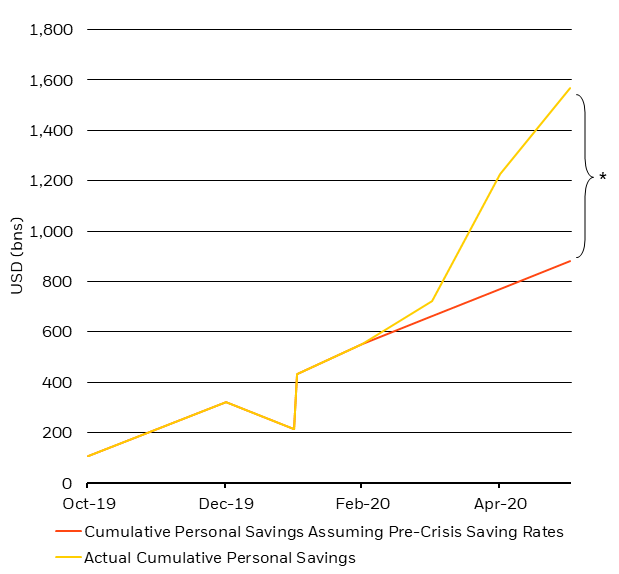

The massive and rapid crisis policy responses truly softened the blow of the black swan pandemic moment. Historic monetary policy assuaged the financial markets by insulating broad swaths of vulnerable private sector entities from a looming liquidity crisis and by facilitating a migration of investor capital back into risk down the asset stack. Furthermore, bold and overt fiscal policy supplanted an unprecedented crisis-driven loss of household income and simultaneously bolstered systemic savings (see Figure 1), which created a much-needed buffer for an uncertain year.

Figure 1: U.S. personal savings (through May) was $688 billion higher due to stimulus

Myths: Risk-free rates depend on what the economy does, and all this monetary policy action risks dramatically higher future inflation.

Amid the Global Financial Crisis policy response, a mythic narrative arguing for the increasingly greater risk of high inflation took hold, and despite not ever materializing, has never really disappeared. Indeed, despite the astonishingly powerful deflationary influence of government-mandated economic lockdowns around the world, this narrative of monetary policy rescue actions leading to a repeat of 1970s-styled inflation has come back with force. We suggest the argument today has as little validity as it did in 2007/08, and neither short-term periods of above-trend growth, nor the increased money supply stemming from crisis rescue measures is likely to cause a hyper-inflationary outcome.

The fact is that both supporting full employment and maintaining price stability are the prime mandates of the Federal Reserve, and for a long time the focus will be on repairing the former, with the extent of policy action being governed by the latter, as we describe below. And we think both the historical record, as well as continued secular headwinds should prevent any repeats of long periods of excessive inflation.

Fact: Inflation is accelerating from a crisis trough, but not enough to divert future policy away from extreme accommodation during 2021 and beyond.

A simple reversion to the mean suggests that dramatic Covid-induced price cuts for goods and services will eventually be lapped over coming quarters, resulting in price increases that will optically flatter inflation readings. However, the secular deflationary forces that have been entrenched for years (think aging demographics and technological efficiencies) will remain a stubborn anchor on prices. So, while core inflation could meet the Fed’s 2% target in the short term, it won’t be sustainable, or threatening enough, to dictate a retreat from accommodative monetary policy in our view.

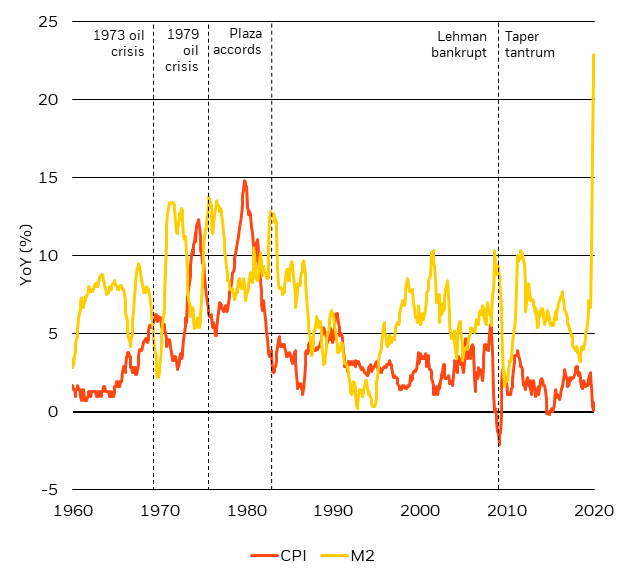

Further, while many commentators argue that heightened policy liquidity could result in a dramatic acceleration of inflation, which could then take monetary policy off its near-to-medium-term path, we would suggest that the historical evidence does not bear that out. Indeed, when looked at from a multi-decade standpoint, there is no discernable link between the growth in M2 money supply and headline inflation levels (see Figure 2), so clearly these relationships are more complex than often depicted.

Figure 2: No discernable link between M2 growth and inflation

Fact: A return to full employment won’t occur for many years, which will keep policy easier for longer.

As the race for a vaccine continues in earnest, the case for incremental policy support will be magnified by a drawn-out recovery in the labor markets. Over coming quarters, the near certainty of stubbornly high unemployment leaves many mainstream analysts predicting massive U.S. fiscal deficits during fiscal 2021 and 2022. If the Federal Reserve were to offset that by pursuing an “in the amounts needed” quantitative easing (QE) policy for the indefinite future, it is likely that most of those deficits would be monetized. The resulting increase in the real economy money supply could be a powerful catalyst for nominal growth (albeit accruing disproportionately to the companies and sectors that are best placed to take advantage of it).

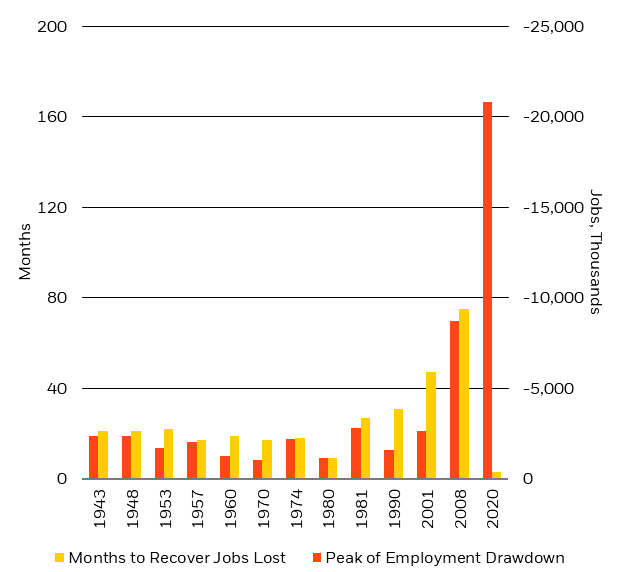

The sobering reality is that we are unlikely to regain full employment for many years. It took almost seven years to recover the jobs from the 2007 employment peak, and the current job losses are almost triple the size of those witnessed in the Global Financial Crisis (see Figure 3). Moreover, throughout the last decade while goods-producing jobs have been in secular decline, transportation, leisure, and hospitality have largely been filling that void. Given the uncertain timeline around the arrival of a vaccine, or a convincing level of herd immunity, it is hard to see those lost service-sector jobs leading the employment recovery back to its pre-Covid levels anytime soon.

Figure 3: It took nearly 7 years to recover jobs from pre-GFC peak, now losses are much greater

Myth: The technology sector is in “a bubble,” and the current period resembles the early-2000s.

Like some of the other myths we engage, the idea that technology sector valuations are perpetually in an inflated “bubble” state, and that this “bubble” is bound to burst in a manner analogous to the early-2000s, is a fiction that nevertheless has remarkable persistence to it. The fact is that the “big 5 tech” firms have transformed themselves into platform companies that are integral to broad-based commercial activity today, and there are many respects in which the current period is quite distinct from the late-1990s/early-2000s. In reality, what is still not appreciated by many is the fact that we’ve entered a profoundly important technology supercycle.

Fact: A technology supercycle that was well underway pre-virus has only gained greater momentum.

Supercycles transcend asset prices – they reshape the very orientation of the economy. Perhaps the most underappreciated financial market influence today is the dramatic continuation of a powerful technology supercycle – one that will be about digitally connecting the goods that the Industrial Revolution set about electrifying. And while the Industrial Revolution was about the consumption of tangible goods, the Tech Revolution will be defined by the consumption of intangible data. So, in order to satiate this voracious demand for data, all the old economy goods that have already reached full penetration (many from the Second Industrial Revolution) will need to re-reach full penetration – as smart devices.

Of course, some of these goods will be rendered obsolete (e.g. MP3 players), and some will become “smart” faster than others (e.g. phones versus cars), but given the global ubiquity of durable goods like cars, refrigerators and airplanes, the epic replacement rates that will be required suggest that this Tech Supercycle is looking less like the Commodity Supercycle of the previous decade and more like the Industrial Revolution in terms of its potential economic impact and longevity. Indeed, over the next decade, the number of connected devices is expected to grow at least fifteen-fold.

At the same time, the ongoing Tech Supercycle is widening the divide between market winners and losers. While the market continues to be fascinated by Growth/Value factor rotations, we are solely focused on identifying those entities that can generate sustainable cash flow growth. Traditional “value investing” is defined as an investment strategy that involves picking stocks that appear to be trading for less than their intrinsic or book value (Investopedia). While Price-to-Book continues to be one of the most common Value factors this, traditional metric fails to capture the worth of intangible assets, such as data.

Therefore, as businesses become more asset-light, the value of the enterprise is less determined by a set of tangible assets, and instead is more determined by cash flows stemming from an efficient use of intangible assets. The ability to generate cash flows expands with ever-fewer limitations if companies are not beholden to a defined capacity of physical assets and are not burdened by their associated expenses.

As a result, instead of profit recessions every four years, as we had in the past, we are witnessing a more persistent mid-single digit revenue growth paradigm from the innovative sectors, and the biggest winners within that cohort are obviously delivering even stronger growth. Thus, systemic cash flows are increasingly concentrated in the hands of a few dominant and fast-growing sectors and companies leveraging the tech supercycle, and the market performance of these entities is not necessarily tied to the health of the broader, virus-laden economy.

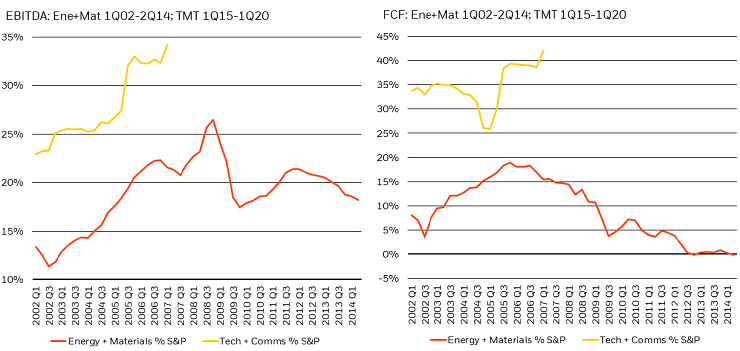

Figure 4: Current tech supercycle versus prior commodity supercycle

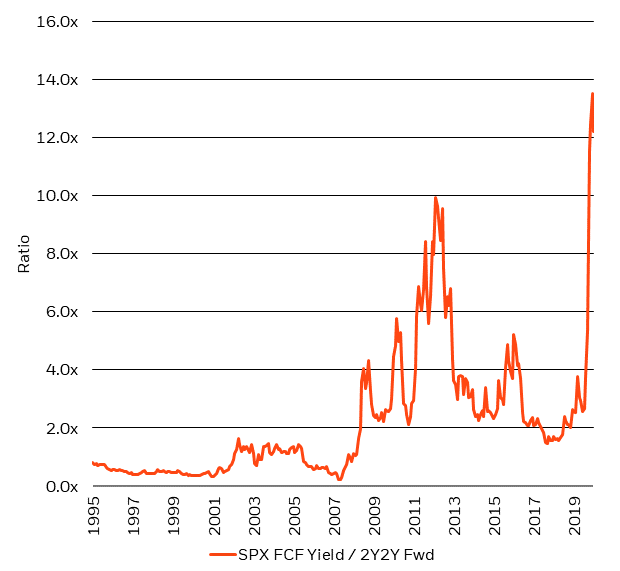

Thus, if a business has higher growth, lower revenue volatility, greater cash flow conversion, less cyclicality, is asset-light, and exists in a low discount-rate world, then its Value is derived significantly more by “tomorrow’s expected cash flows” than by “today’s asset base and current income” (see Figure 4 for a comparison of the current supercycle with the prior commodities-based supercycle). Whereas P/E multiples were useful in the past, valuation metrics that measure cash flow and its future growth are far more relevant today. And on that basis the S&P 500 has not been this cheap relative to risk-free rates since the 1960s. We believe that in the face of an indefinite period of sustained lower risk-free rates, there is room for compression in the free cash flow yield of stocks relative to risk-free rates over the long-term. In fact, it is absolutely remarkable today to see that the free-cash-flow yield on the S&P 500 is 13X the 2-year, 2-year forward Treasury yield, suggesting to us that the upside from interest-rate improvement is largely gone, but that you are still being paid for taking risk, particularly in a barbell-styled portfolio (see Figure 5).

Figure 5: With equity FCF at 13X the 2y2y forward TSY yield, you’re still being paid to take risk

Myth: U.S. Treasury (or other developed market) rate levels are what regulate lending dynamics

While the absolute levels of interest rates were once critical for understanding lending dynamics within an economy, we think the aggregate supply/demand of capital is a more vital factor today, with the price of money now changing based on a multitude of factors. That’s largely because merely having lower, or even negative, interest rates doesn’t catalyze capacity growth if there’s no aggregate demand growth, or no pricing power. Likewise, relatively higher rate levels in the 1970s and 1980s didn’t stifle the capacity growth rate. Furthermore, it’s clear to us today that the risk-free rate is no longer driving borrowing costs and that credit risk factors are much more important in setting the corporate cost of capital.

So, just as we’re witnessing a growing demand for income-producing assets from pension funds, insurance companies and individuals, all desperately seeking ways to meet their future liabilities, the massive central banks asset purchase programs end up crowding out capital from high-quality investments. And while these rescue measures were vital earlier in the year to support proper market functioning, and have supported asset valuations, they also end up driving capital/lending into alternative yielding assets, potentially including equity markets. These market dynamics are likely to result in greater sector and regional return dispersion, as investors seek to meet return targets, and we think European asset markets could potentially be affected by it.

Fact: The European Covid policy response is game changing.

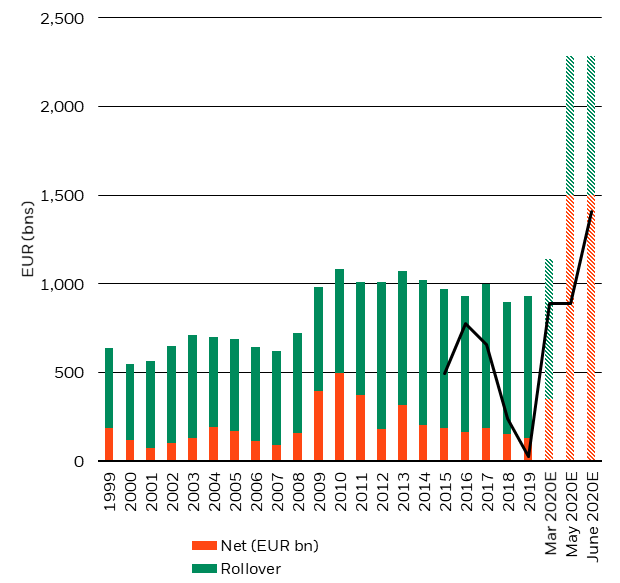

A dramatic policy pivot is underway in Europe, where bold monetary policy is being combined with the massive European Recovery Fund (see Figure 6). We are becoming increasingly optimistic that these changes can finally break a stubborn cycle of diminished real economy velocity and catalyze the dawn of a virtuous, and much needed, investment cycle that may well attract significant global capital flows. Indeed, the combination of supportive fiscal policy and easy financing conditions facilitate a durable and much improved Continental investment climate. Europe’s asset valuations are cheaper than much of the rest of the developed world, allowing for substantial appreciation if there were to be a “catch-up” trade.

Figure 6: The European PEPP’s flexibility means that QE now covers all Net-2020 sovereign issuance

Investment implications

Despite the somewhat positive bias of our outlook for the quarters ahead, one might feel conflicted about staying the course and holding a risk asset portfolio in the face of relentless, and stubbornly negative, news flow. But while the media’s ongoing objective is to generate its own cash flow growth through higher readership, more virtual “hits,” and greater numbers of followers, our focus as investors should be on finding investment destinations where cash flow growth is robust and durable. In other words, we shouldn’t confuse the path of the news, which today is largely driven either by antagonist politics, or the virus, for the destination of asset prices, which are ultimately driven by cash flows in the years to come.

At the heart of our portfolio allocations is the growing conviction that “the need for income” deserves to join “death” and “taxes” on the list of exceptions to this world of unending uncertainty. It is this need for income that has been and will continue to provide the insatiable bid behind yielding assets, and income has never been scarcer than it is today. Further, we have long believed that markets underestimate the benefits of coupon/carry and that income seems to become ever more valuable when it is more difficult to attain.

In 1995, a 100% bond portfolio could meet a manager’s 7.5% yield target. In 2020 and beyond, it is likely that at least 90% of portfolios reaching for the same 7.5% return will need to be comprised of several alternative sources of income, preferably allocated in a barbell-styled structure. Some critical components to that portfolio barbell include mid-quality yielding spread assets in the U.S. and Europe, global equities, Treasury Inflation Protected Securities (TIPS), gold and other alternative assets, such as private equity, infrastructure, or natural resources-backed assets. Additionally, holding some meaningful levels of cash today makes sense, both as dry powder to take advantage of unforeseen opportunities, and as a left-tail risk hedge. Investors would do well to start formulating an alternative(s) asset allocation plan today.

© 2020 BlackRock, Inc. All rights reserved.

© BlackRock

Read more commentaries by BlackRock