Russ explores what’s driving the continued strength of the consumer.

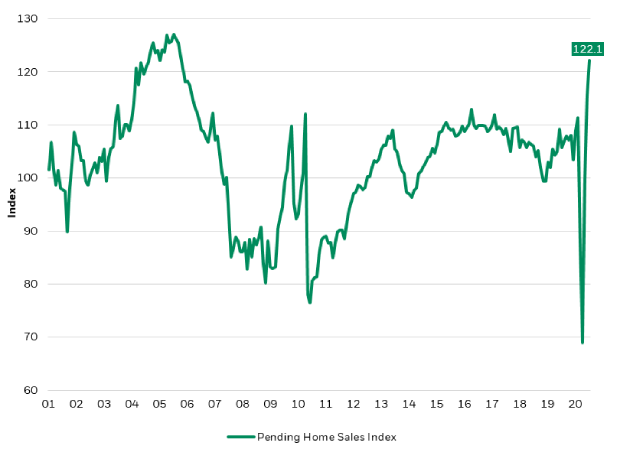

Despite the worst recession and public health crisis in generations, the U.S. consumer is (once again) defying the pessimists. Besides the rapidity and magnitude of the rebound, what is also remarkable: the breadth. While online commerce continues to surge, spending has broadened to include more traditional categories, notably autos and housing.

I last discussed the consumer in early June. At the time I suggested that a combination of record stimulus, resilient housing and an improved balance sheet would prevent a collapse. Since then both spending and consumer stocks have beat expectations. After bottoming at a 20% year-over-year decline, retail sales are rising at nearly 3%.

As spending has rebounded so have consumer stocks. During the past three months the consumer discretionary sector has gained approximately 14%, second only to the technology sector. Gains have been led by a melt-up in internet commerce names, but other industries are also rallying. Home improvement, general merchandise retailers, and home builders have all posted double-digit gains.

While the big gains may be behind us, I would expect spending to continue to firm. Yes, fading stimulus is a risk, but it is offset by steady and strong balance sheets, a rapidly healing labor market and a surge in housing.

Wealth up, debt down

Back in June I highlighted that household balance sheets have recently been a source of strength. The last three months have witnessed further improvement. Household debt as a percentage of disposable income remains at a 20-year low while debt servicing costs have never been lower. Meanwhile, net worth is supported by both a rising stock market and a housing rebound.