Among the many significant developments in the world that investors should be considering as part of their long-term thinking, one of the issues that concerns me the most is China.

China is a colossus, ranking among the great nations alongside the United States. The size of its workforce and its dominant position in key sectors from semiconductors to rare earths make it a critical player in the global economy. Its position as both a continental and maritime power and home to one fifth of humankind makes China a significant geopolitical actor as well.

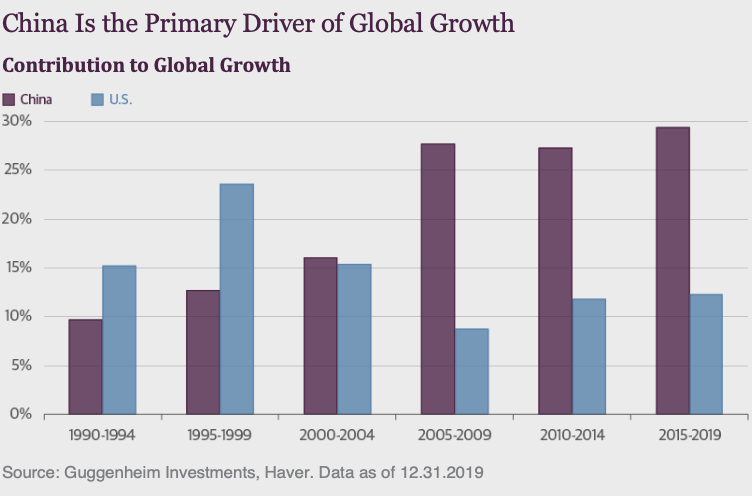

In the last fifteen years, China’s growth has contributed 27 percent to global growth, while the U.S. has accounted for an average contribution of about 10 percent over the same time period. Although some will argue this point, I believe the growth and engagement of China has been net positive for the U.S. and the world from an economic perspective.

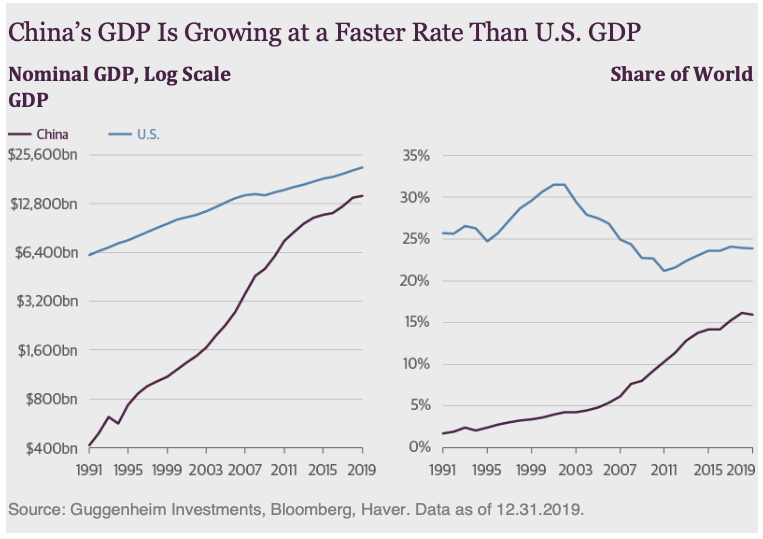

In the process, China has steadily gained on the United States to become, in many ways, its economic equal.

To fully appreciate the complexity of the Sino-American relationship the two nations must acknowledge that they have a long and mutually beneficial relationship. Since the Qing Dynasty, the U.S. has supported Chinese territorial integrity. During the 1930s and 1940s the United Sates opposed the occupation of China by colonial powers seeking to exploit Chinese resources. As part of the resolution of the War in the Pacific, the U.S. required restoration of the territorial integrity of China.

In the 1970s, leaders from both nations sought to resolve the issues of the post-war period recognizing that the long and harmonious historical relationship should be fully restored. This resulted in the People’s Republic of China becoming the fully recognized official government of China, elevating its global status and replacing Taiwan as a permanent member of the United Nations Security Council.

During the past four decades, the main determinants of growth in China have been the economic and social reforms of Deng Xiaoping’s Four Modernizations program and normalization of relations with the United States. China’s remarkable economic growth would have been much more difficult in the absence of the rapid and mutually beneficial expansion in the U.S.-China relationship following normalization.

That normalization has been underpinned by the concept of “strategic ambiguity.” This shared determination meant that diplomatic accommodation would be part of the strategic partnership. The US and China would work together to halt Soviet assertiveness while agreeing to disagree on numerous issues that remained unresolved, such as Taiwan, maritime claims in the South China Sea, the Vietnam-Cambodia conflict, and divergent views regarding internal democratic values and practices. The effect has been to change the global balance of power, including the Soviet reassessment that precipitated the end of the Cold War.

More recently, diplomatic accommodation has allowed the U.S. and China to broker China’s entry into the World Trade Organization (WTO) in 2001 and an historic agreement on climate change in 2015, despite numerous differences on trade, human rights, and other issues.

China has been able to rapidly transition beyond the customary place of an “emerging markets economy,” by advancing up the value chain and reducing its reliance on manufacturing and exports as the primary source of general economic growth. China is moving beyond its status as the manufacturing floor to the world that drives exports through cheap labor and a managed currency, and is becoming a society that generates economic growth internally. Services now account for 54 percent of the Chinese economy, up from 39 percent in 2000. While China has not reached the level of the U.S.—services contribute 70 percent to our economy—it has come a long way.

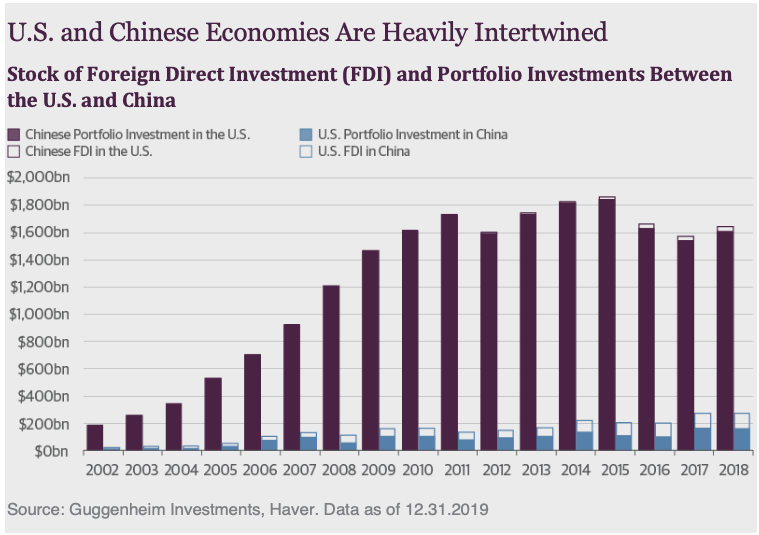

The complex interdependence of the United States and China has become one of the foundations of global political and economic stability. Talk of a “G2” a decade ago was seriously considered as a framework for guiding the global economy. Over the years, China and the U.S. have come to need each other: the U.S. consumes China’s exports, while China uses dollars to purchase natural resources such as oil and natural gas, agricultural products, and capital goods such as aircraft and construction equipment, and invest in financial assets such as U.S. Treasury securities, which reduces U.S. interest rates.

My concern over China stems from the fact that the idea of strategic ambiguity has now been replaced, formalized by President Trump’s definition of China as a “strategic rival” in his Administration’s National Security Strategy as well as the decision by the Standing Committee of the National People’s Congress to enact the “Safeguarding National Security” law permitting a more direct role in Hong Kong affairs. As a result, differences between the U.S. and China that would have been set aside and resolved over time to their mutual benefit have now become flashpoints that define the relationship. Among these flashpoints are the status of Hong Kong; maritime operations in the South and East China seas; China’s courting of Iran and other countries in the Persian Gulf to secure energy sources and other trade relationships; 5G competition between Chinese and US companies; and, of course, the most symbolic and potentially dangerous flashpoint of all, the status of Taiwan. Tariffs are the weapons in the current round of tension, and the rhetoric from both sides is increasingly inflammatory.

The ramifications of this change are becoming clear. Replacing strategic ambiguity with pugnacious clarity when China was a small player on the world stage is one thing, but quite another when it has become a global economic power. Continued escalation of tensions could have disastrous effects on an already weak global economy. Uncertainty about the path of the U.S.-China relationship hangs over the financial markets and could lead to increasing episodes of market volatility. A major Chinese growth shock could expose vulnerabilities associated with the massive rise in leverage since 2008, in turn spreading pain across a global economy that has become very dependent on China as a growth engine.

Certain aggressive policies against China could erode America’s competitive advantage. For example, limiting student visas and tightening immigration policy could push talented foreign individuals, including hardworking Chinese, to other countries. Unilateral financial sanctions by the U.S. create incentives for China and its trading partners to move away from the U.S. dollar. Establishing technology export bans may end up reducing our trade surplus in tech products and incentivize other countries to develop alternatives to American technologies (e.g., Samsung will supply chips to Huawei in return for market share in China). Tariffs on China could force China to lower trade barriers with the rest of the world, stimulating free trade agreements that do not include the U.S., like the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP).

Next, if forced to choose sides, many states may hedge their bets, concerned by a United States turning inward. Unlike the USSR, which did not have many economic linkages with the West, China has become the largest trading partner of many countries, including major U.S. allies.

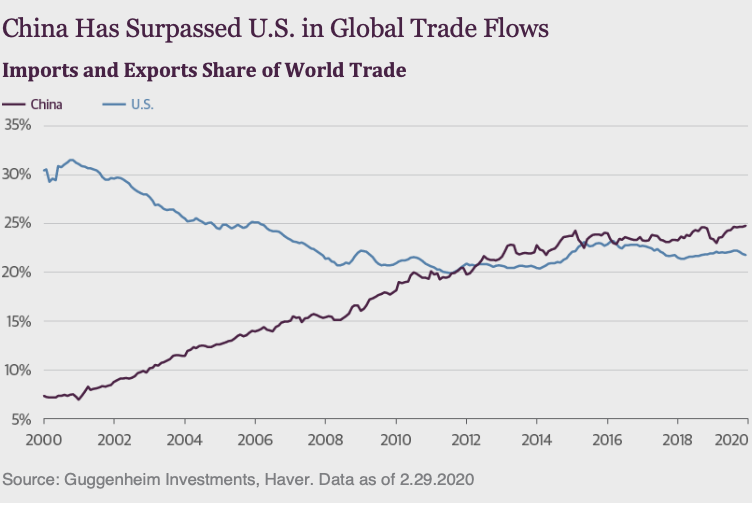

China has also become a central counterparty for global trade flows, having recently surpassed the United States, and its financial interconnectedness is also on the rise.

While China’s direct investment is still less than the United States, it is increasingly buying influence by spreading its wealth around the world. For these countries, China has become a crucial partner.

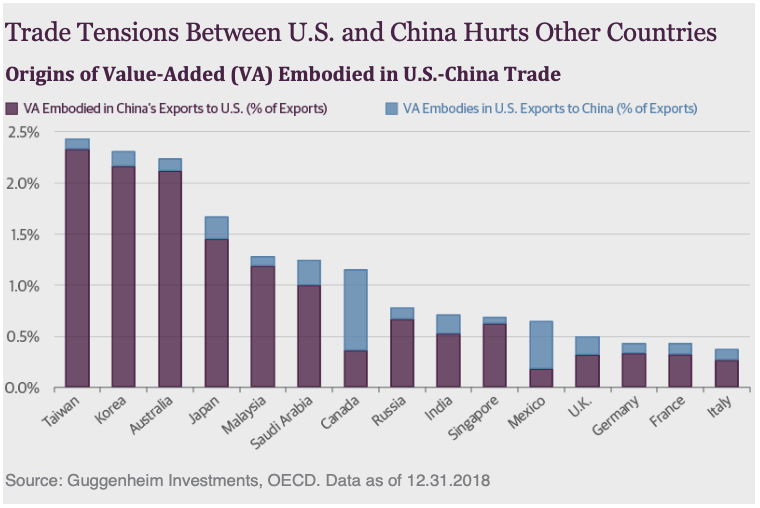

Finally, the trade frictions between the U.S. and China are not happening in a vacuum. Global supply chains for trade between the two countries typically include value-added contributions from other countries. These trade flow contributions by other countries to flows between the U.S. and China are sizable components of their domestic economies. Any reduction in trade between China and the U.S. will result in significant global economic collateral damage.

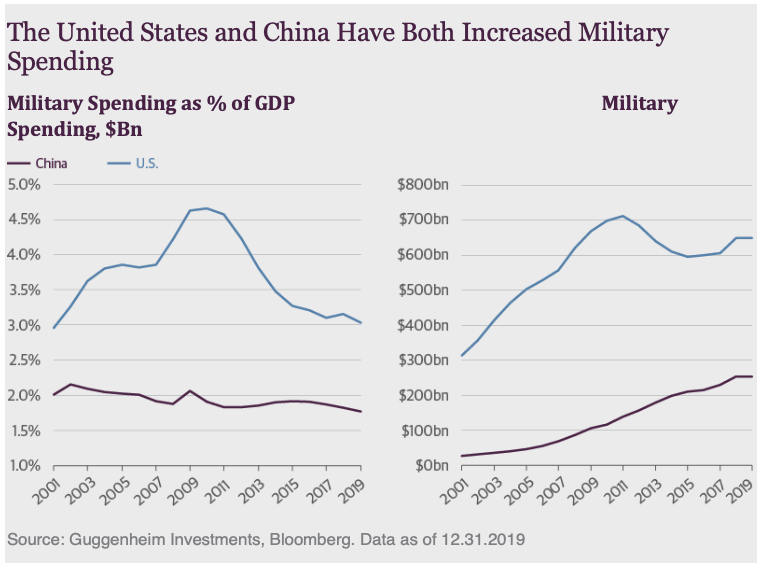

President Trump and President Xi both have incentives to de-escalate the trade war through a Phase 1 trade deal, but the most pressing U.S. concerns have not actually been resolved. It is not lost on any student of history that if diplomacy fails, other options are less desirable. Trade tensions seem to have spawned bellicosity over North Korea, Hong Kong, Taiwan, and the South China Sea. President Xi has made shipbuilding and military spending a top priority, pushing China’s claims further west into a Pacific Ocean defined for seven decades by the United States’ mutual defense treaties.

I expect tensions between the U.S. and China will be exacerbated by campaign rhetoric leading up to the next U.S. presidential election. Pre-virus tensions have not disappeared due to the pandemic, they have escalated as blame is being cast on China for both causing and trying to cover up the virus. Anti-China sentiment in the U.S. is bipartisan and as fervent as it has been since about the 1950s. Both President Trump and former Vice President Biden are talking tough on China, and this is likely to lead to a more muscular approach to China that will characterize whichever administration is in power in 2021.

As a prudent investor who assesses the probability of outcomes to manage risk, my view is that the likelihood of a worsening situation is rising. Preparing for this means preparing for rising volatility as the global economy and world markets adjust to this battle of the titans.

As a practical matter, I believe that leaders of both countries need to be mindful of the centrality of their interdependence. We need to take every opportunity to widen and deepen our geostrategic and financial collaboration, particularly in coping with the global health and financial crisis, as well as global challenges like climate change. In an era in which the risks of massively destructive global challenges are rising, a genuine reconciliation would be far better than a decoupling.

Important Notices and Disclosures

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Investing involves risk, including the possible loss of principal.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

©2020, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.