Bank Loans: Three Questions on What’s Changed Since the March Madness

1. In a March blog post, you referred to loans as “stupid” cheap. How do fundamentals and valuations look now?

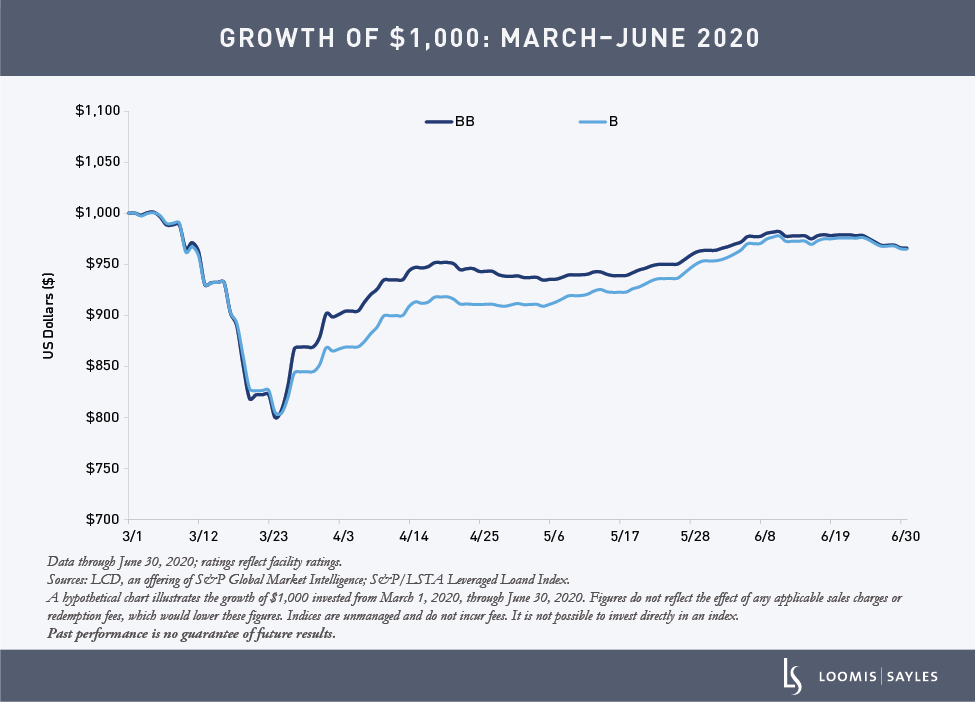

At the time, we asserted that “when people get scared, they often tend to focus less on rational investment prospects and more on feeling better at that moment.” We believe that sentiment drove loans to “stupid cheap” levels in March. Since then, we’ve seen the majority of the loan market bounce back to higher valuations based on fundamentals, not emotion, and the gap between BB and B-rated loans has nearly evaporated. We have thoroughly assessed the ability of each loan in our portfolios to withstand the liquidity squeeze created by the pandemic and have assigned each loan with an expected recovery pattern. We have been pleased with the results of this analysis and feel strongly that most of the loans we own have the liquidity to survive a significant period of pandemic-related challenges. Importantly, we expect a large proportion of our loans to have sharp V-shaped recoveries once the recession subsides, even in a U-shaped economic recovery. We maintain our longer-term view that science will win, the virus will be beaten back, and monetary and fiscal stimulus will ultimately lead to growth.

2. At the height of the crisis, you saw three different roads back to par, with market recovery in 6-12 months the most likely. Has the recent market activity changed your view?

Markets tend to recover 6 months before fundamentals justify that recovery. So when we said 6 to 12 months, we thought the fundamentals might merit enthusiasm 12 to 18 months from March and markets might anticipate that between September of 2020 and March of 2021. The sharp market recovery immediately after our comments was a surprise to us, but it does not change the rationale for our original 6-12 month comment. Loosely, we imagined fundamentals could be more encouraging between March and September of 2021 as anti-viral medications, vaccines, and behavioral changes show efficacy. So, while positive momentum among risk assets continued building in the second quarter, we also expect volatility between here and normalization.

Since the end of March, fiscal and monetary policy measures have created much of the updraft across markets, including the loan market. More recent anticipation of a potential vaccine and reopening activity has bolstered markets further. The news flow from here is likely to be much more mixed, particularly as US and global markets begin to digest data related to the gradual process of reopening. We expect sentiment in the loan market to generally correlate with that of overall risk markets as companies are tested.