Key Points

-

Investors are often most uncomfortable when it seems that the stock market isn’t making any sense whether it’s heading up or down. In these uncertain times, it may be comforting to know that the markets are making some sense.

-

We are able to make some sense of global earnings and stock market performance in addition to the pace and success of re-openings and relative stock market performance across countries.

-

While it makes little sense that there would be such a big gap between the market and analyst estimates for the return of dividends, we expect an official announcement by the European Central Bank (ECB) to help make sense of that soon.

While no one is ever really comfortable losing money, we often hear from investors that they are most uncomfortable when it seems that the stock market isn’t making any sense whether it’s heading up or down. In order to help try to make sense of it all, let’s take a look at where the stock market makes sense right now and where it doesn’t.

Making sense of earnings and performance

Corporate earnings are the most important long-term driver of the stock market. Any changes in the outlook for earnings per share (EPS) should be aligned with stock price movements, even in the near-term. While the outlook for earnings has been clouded by the impact of COVID-19, the direction of analysts’ earnings revisions has been closely aligned with stock price movements.

Changes to analysts’ earnings estimates and stock market performance

Source: Charles Schwab, Factset data as of 7/5/2020. Past performance is no guarantee of future results.

Of course, there are many companies with downward revisions to analysts’ earnings estimates in addition to those with upward revisions. That number is a mirror image of the number of companies with upward revisions in the chart above, peaking in early April and then falling steadily.

Although the dollar amount of analysts’ estimates of the next 12 months earnings per share for MSCI World Index companies has been slowly rising over the past month, it’s hard to have a high degree of confidence in the magnitude of earnings, given all the uncertainty. Instead, it is the direction of analysts’ changes which becomes important to the direction of the stock market. A worsening outlook on the pace or sustainability of the global recovery from COVID-19 would likely affect both the outlook for earnings and the stock market.

Making sense of re-openings and performance

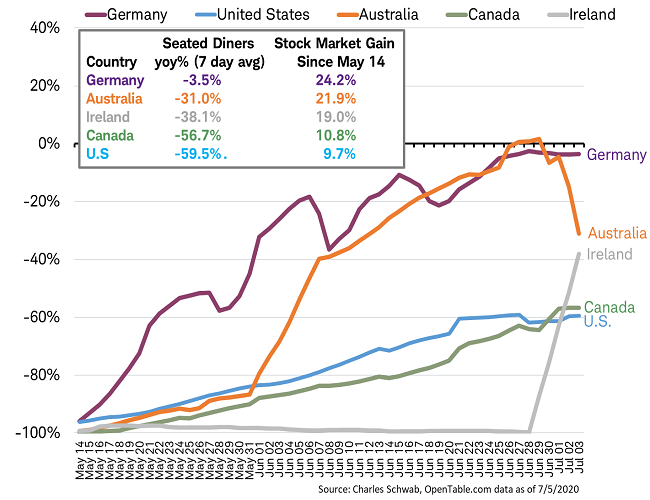

Our weekly real-time recovery heatmaps track many different aspects of the economic recovery and have been highlighting the different pace of the recoveries in different countries. Focusing in on just one important aspect of recovery may help to explain the performance of stocks across countries.

Many of the latest re-opening and re-closings tied to COVID-19 have been tied to public gathering spaces, so we look at restaurants. Although the data is limited to a relatively small number of major countries, the trend in seated diners at restaurants on the OpenTable reservation network since re-openings began in mid-May aligns with relative stock market performance, as you can see in the chart and table below.

Change in diners at restaurants and stock market performance

Source: Charles Schwab, OpenTable.com data as of 7/5/2020. Individual country performance based on its respective MSCI country indexes (MSCI Germany, MSCI Australia, MSCI Ireland, MSCI Canada, MSCI U.S.) Past performance is no guarantee of future results.

Restaurants in Ireland finally reopened to seated diners on June 29, accounting for the rise in diners in the chart above. Meanwhile in Australia, restaurants in the state of Victoria (home to the city of Melbourne) were re-closed on July 1 until July 29, after an outbreak of COVID-19. We will be watching to see if this begins to be reflected in the performance of the Irish and Australian stock markets this month.

Divided dividend outlook makes no sense

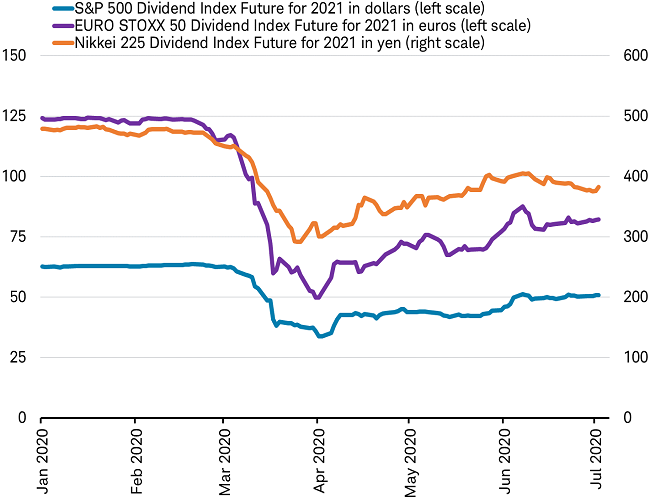

Stock prices in the major indicies have recovered most of their losses so far this year, but dividends have not. On this issue, market and analysts are seeing things very differently.

The market’s expectation for dividends per share has rebounded about halfway back to where they were at the start of the year for stocks in the United States, Europe and Japan. The dividend futures prices for the S&P 500, Euro STOXX 50 and Nikkei 225 Indexes in their local currencies are shown in the chart below.

Dividend futures recovery near halfway point

Source: Charles Schwab, Factset data as of 7/5/2020. Past performance is no guarantee of future results.

While not expecting a complete recovery for dividends per share next year, the analysts’ consensus forecast for dividends per share in 2021 for these indexes are even higher than the current market forecast, as you can see in the table below.

Expected dividends per share in 2021

Source: Charles Schwab, Factset data as of 7/5/2020. Past performance is no guarantee of future results.

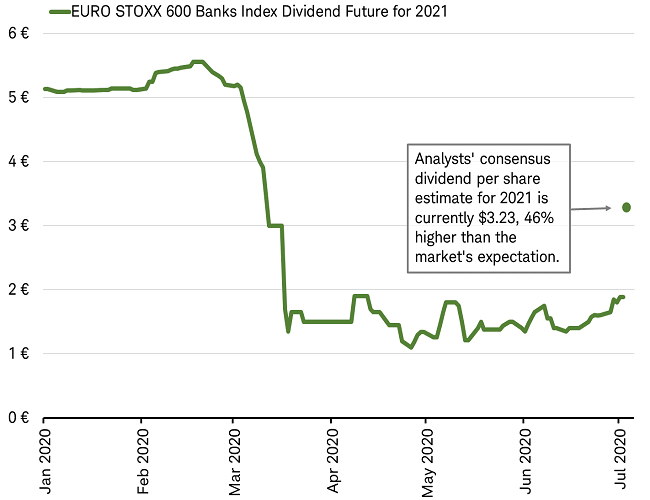

It makes little sense to see such a big gap between the market and analyst estimates for the return of dividends. The biggest difference in expectations is due to the financial sector (especially in Europe). Banks in many parts of the world have cut their dividend payments to preserve capital in the aftermath of COVID-19. In late March, the European Systemic Risk Board (ESRB) recommended that banks suspend dividends for 2020 at least until October, leading to a plunge in the market’s expectation for European bank dividends, as you can see in the chart below. Those expectations have not recovered, the market is pricing in only €1.89 in dividends per share for the bank sector of the Euro STOXX 600. In contrast, analysts’ expect a recovery to €3.23 per share next year, nearly 50% higher than the market.

Big gap: expected dividends for Europe’s banks in 2021

Source: Charles Schwab, Factset data as of 7/5/2020. Past performance is no guarantee of future results.

Analysts expect banks to have the capital and regulators to ease the ban, allowing a recovery in bank dividends. The market is betting the opposite. So who is right? We may find out soon. The European Central Bank’s Single Supervisory Mechanism has said it may provide clarity on its dividend ban in July, which could offer more visibility on the outlook for dividends.

Markets making some sense

We’ve been able to make some sense of global earnings and stock market performance, re-openings and relative stock market performance across countries, and we expect to be able to make sense of the dividend divide fairly soon. While these are uncertain times and there can be no guarantees, it may be comforting to know that the markets are making some sense.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Futures trading involves substantial risk and is not suitable for all investors. Please read the Risk Disclosure Statement for Futures and Options before considering any futures transactions.

All names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

The Nikkei 225 tracks the 225 top blue-chip companies listed on the Tokyo Stock Exchange from a range of industries.

The EURO STOXX 50 Index is a blue-chip index for the Eurozone, which covers 50 stocks from 12 Eurozone countries: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain.

The STOXX Europe 600 Index has a fixed number of 600 components and represents large, mid and small capitalization companies across 18 countries of the European region: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom.

Euro STOXX 600 Banks Index tracks the Banks supersector constituents of the Euro STOXX 600 Index. Companies are categorized according to their primary source of revenue.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(0620-07T7)

© Charles Schwab

Read more commentaries by Charles Schwab