On My Radar: The Stockdale Paradox

Learn more about this firmMembership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Retain faith that you will prevail in the end regardless of the difficulties,

and at the same time confront the most brutal facts of your current

reality, whatever they may be.”

– Jim Collins

Management Researcher, Consultant, and

Author of Good to Great: Why Some Companies Make the Leap and Others Don’t

Admiral James Bond Stockdale was the highest-ranking United States military officer in the “Hanoi Hilton” POW camp during the Vietnam War. His jet was shot down in 1965, and after parachuting into a small village, he was taken as a prisoner of war. He was tortured over 20 times during his nearly eight-year confinement. Despite the uncertainty as to whether he would survive to ever see his family again, he endured.

Not only did he survive, but Admiral Stockdale was resolute in opposing his captors to the fullest extent (at one point, he even beat himself with a stool and cut himself with a razor so that he could not be taped for propaganda purposes). He also led the other POWs in resisting torture and set up an elaborate communications system amongst the camp prisoners. What is amazing and applicable to our current crisis is the stoic resoluteness of Stockdale (influenced by his study of Epictetus, a Greek stoic philosopher, and Meditations by Marcus Aurelius, which details the stoic precepts used by the Roman emperor to manage his various responsibilities) that was essential to his survival and leadership.

In the process of writing Good to Great, management researcher and consultant Jim Collins interviewed Admiral Stockdale and adapted his insights for business. Collins’s focus was not just on extracting leadership lessons, but more specifically on understanding how Stockdale was able to remain steadfast in the face of such an ordeal with no certainty that he would survive. Stockdale’s response (quoted from Good to Great) was:

“I never lost faith in the end of the story. I never doubted not only that I would get out, but also that I would prevail in the end and turn the experience into the defining event of my life, which, in retrospect, I would not trade.”

When asked, “Who didn’t make it out?” Stockdale responded with the following:

“The optimists. Oh, they were the ones who said, ‘We’re going to be out by Christmas.’ And Christmas would come, and Christmas would go. Then they’d say, ‘We’re going to be out by Easter.’ And Easter would come, and Easter would go. And then Thanksgiving, and then it would be Christmas again. And they died of a broken heart. This is a very important lesson. You must never confuse faith that you will prevail in the end—which you can never afford to lose—with the discipline to confront the most brutal facts of your current reality, whatever they might be.”

Herein lies the Stockdale Paradox, as distilled by Collins:

“Retain faith that you will prevail in the end regardless of the difficulties

and at the same time confront the most brutal facts of your current reality,

whatever they may be.”

As we face uncertainty about the future—the pandemic’s and our own—this lesson cannot be timelier. While we must retain hope that we will prevail as business leaders and investors, we must remain grounded and disciplined—prepared for the possibility that the economy may not be open as quickly as we hope it will.

Stockdale’s story is truly amazing. At the time of his release, he became the first three-star officer in the history of the Navy to wear both aviator wings and the Congressional Medal of Honor. Admiral Stockdale taught Jim Collins that what separates people is not the presence or absence of difficulty, but how they deal with the inevitable challenges of life.

To help inspire and keep resolute his fellow Americans, Jim Collins recently posted the following video on the Stockdale Paradox. I find the story powerful and recommend sharing it with your colleagues, your clients, your friends, and family.

I made a few minor edits to the above, which was written by CMG’s president, PJ Grzywacz. If you are a client, you may have noticed the piece in our strategy updates. A grateful hat tip to PJ. An important story—especially for the times.

V, U, or L

Back in late February and early March, in the early stages of the coronavirus pandemic, there was speculation about what a market recovery would look like. Would it be a V-shaped market recovery, rocketing back up as quickly as it came crashing down? Did social distancing and the shutdown mean we would have a U-shaped recovery, denoting a longer period of subdued economic activity (one or two quarters of decline) before that strong recovery came about? Or would the economy take an L-shaped path, in which unemployment remains high, growth is sluggish, and progress is slow, as my friend and market sage Art Cashin recently suggested.

We believe that the recovery will be slow. Maybe two Easters; maybe two Christmases. But keep Stockdale’s resoluteness in mind: never lose faith in the possibility of a happier ending.

We are seeing a new wave of outbreaks, and it is affecting different regions of the country, creating a rolling shock to the economy in such a way that we are unlikely to reach full capacity for some time. In my notes on Jim Bianco’s SIC 2020 presentation last week, I highlighted his belief that the economy will recover back to just 90% of its former self and noted that, on the surface that may sound OK, but it is actually a disaster. For now, the Fed is controlling the narrative of the market. At some point, fundamentals will.

In a recent interview, Art Cashin offered the following: “The question is, will the public be eager to rush back? Even people like you and me, who love to go out and socialize, it might be difficult to get that back any time soon,” he said. “Will they come back? Yes. Will they come flooding back the day after they say you can relax social distancing? No. So the chances of a bounce-back are there, [but] the chances of a rapid bounce-back are low.”

We are farther down the road from when Art made that comment. Flooding back? No. Not yet.

Leadership

Serendipitously, I ran into Michael Gale, an old friend, while playing golf at my happy place, Stonewall. Michael joined my wife Susan and me as we walked a few holes, and he told us about his firm’s work. I was blown away.

Michael began to tell us about his boss, Randall K. Stutman, Ph.D. Randall has studied more than 12,000 exceptional leaders, and found out what that the very best leaders do all the time. He has taken what he learned and uses those insights to advise many of the world’s top CEOs, coaches, athletes, and other important leaders. His passion is to help people understand leadership from a very different point of view.

What does that entail? Randall believes leaders tend to overcomplicate things. So, he simplifies them for his clients. It all boils down to what he learned from those 12,000 exceptional leaders. Irrespective of age, generation, experience, the type of business or organizational culture, the best leaders all do the same thing to motivate and inspire their teams, their families, and their friends. And he believes you and I can do it too…

After golf, Michael began to send me material on what they call “Admired Leadership.” With inbox full and my to-do list loaded, I put the links he sent on the back burner. Then, a second knock on the head came. I always know I need to take and close look at something when the same information comes to me in a seemingly different way—a friendly but firm reminder that it’s time to pay attention.

Years ago, I had a business relationship with James Altucher. James is an American hedge fund manager, author, podcaster, and entrepreneur who has founded or cofounded more than 20 companies. He has published 20 books and he is a contributor to publications including the Financial Times, The Wall Street Journal, TechCrunch, and the Huffington Post. Impressive, but even more so is the fact that he is a really good guy.

James interviewed Randall. It was the first time Randall agreed to do such an interview. The discussion is eye-opening. Randall shares some key insights on how to become the kind of leader people love and admire, and you can listen to it via the link below.

Click on the image above for the podcast.

Put your sneakers on, put in your headphones, and get out for a long walk. I guarantee you’ll love the discussion. And share it with your family and friends.

The Trade Signals post is below and I share a simple leadership idea from Randal Stutman in the personal section.

Trade Signals – Profits, Earnings and Trend (and Look at Gold Go)

June 24, 2020

S&P 500 Index — 3,131

Notable this week:

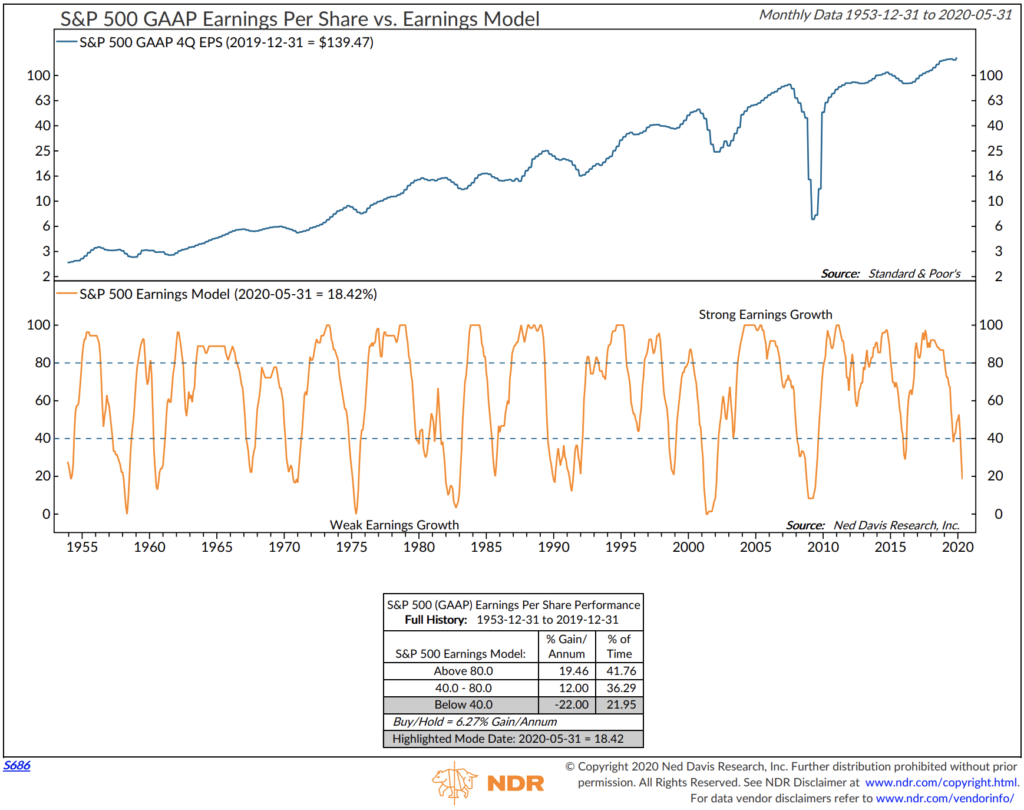

The WSJ’s Lev Borodovsky sends an email that hits my inbox every morning. The piece he writes is called “The Daily Shot” and the charts and his research reach are excellent. If you are a WSJ subscriber, you can sign up to receive Lev’s daily note. A few weeks ago, we looked at the earnings outlook. It’s hard to imagine how profits won’t be significantly impacted over the coming 12-24 months (businesses cut expenses, staff and individuals save more and spend less). Which leads me to the following chart. It may take some time but eventually the stock market will catch up with profits. Here the black line tracks profits — note how profits peaked in 2015 and were already in decline before Coronavirus emerged. The red line tracks the market. Alligator jaws always close. Either profits will nearly double in order to catch up the stock market or the market will decline to catch up to profits or both. I don’t see a profit silver lining in 2020 or 2021. We can thank the Federal Reserve for now, like we did in 1999 and 2007 (bubble peaks) but keep your stop-loss, risk management processes in place.

Let’s put the overvaluation into perspective. First, earnings are weak and in decline. Weak earnings lead to weak profits.

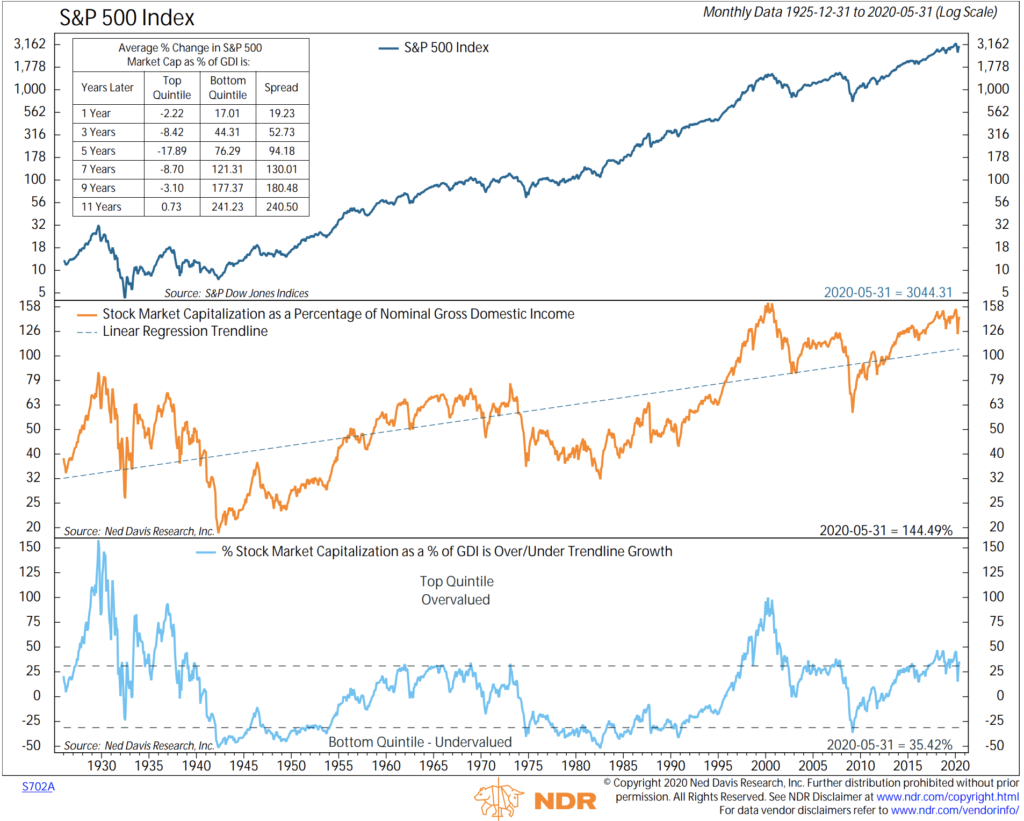

Next, markets always mean revert back to the long-term growth trend line (light blue dotted line in the middle of the next chart). Given the current level of valuation, what does this mean in terms of probable coming S&P 500 Index returns? Take a look at the box in the upper left of the chart: 1-, 3-, 5-, 7-, 9- and 11-years. What this is saying is that from our current overvalued starting point (5-31-2020 lasted data post), $1,000,000 will be worth $82,110 in five years. $1 million will be worth less in all except 11 years from now. Then it will be worth $1,000,730. The optimistic note in all of this is playing more defense today will mean you are in a position to take advantage of a much better return opportunity. That’s where price-based trend following processes can help.

No major changes in the Trade Signals. Don’t Fight the Tape or the Fed is back to a neutral reading. Investor optimism has waned and is now in the neutral zone for both the daily and weekly data. The trend for equities is still up. Bonds are also in a bullish up-trend and take a look at gold. Gold is strong!

Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Have a fun weekend!

Warm regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

Follow Steve on Twitter @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is a general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purpose.

In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

© CMG Captial Management Group

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits