A Recession Like No Other

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsCorona Recession

Choosing Not to Spend

The Wealthy Assume the Fetal Position

Inevitable and Unacceptable

Puerto Rico and Dust Bowls

We just spent the better part of a decade wondering when the next recession would strike. The last two months we stopped wondering. It’s here and a grand council of esteemed economists has confirmed it.

On June 8, the Business Cycle Dating Committee of the National Bureau of Economic Research found monthly economic activity had peaked in February 2020. On a quarterly basis, the peak was in Q4 2019, but in either case, a recession is now underway.

It’s important to recognize how they define “recession.”

A recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators. A recession begins when the economy reaches a peak of economic activity and ends when the economy reaches its trough.

If the trough isn’t here yet, when will it arrive? We don’t know. The NBER committee identifies these in hindsight. If all goes well, they may look back and say March or April was the bottom, making this one of the shortest recessions ever. But it will also be the strangest recession ever, because even if we are “recovering” we will still be further away from the previous peak than ever before, with unemployment well above 10 million.

NBER also said this time is different:

The committee recognizes that the pandemic and the public health response have resulted in a downturn with different characteristics and dynamics than prior recessions.

Considering exactly how this recession is different gives us some insight into how long it may last.

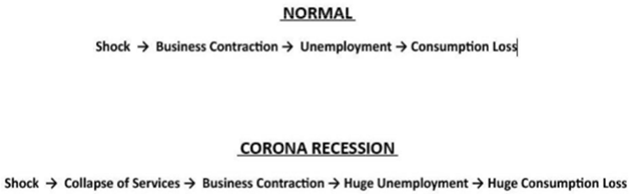

Corona Recession

Many economists thought a recession was close even before the pandemic. The expansion had run longer than any other. Cracks were forming and the main question was what would trigger a decline.

I thought we were headed for a credit crisis, centered on corporate debt rather than mortgages, as happened in 2008. The Fed’s decades-long easy money policies have many businesses leveraged to the hilt. That remains the case and could still become a bigger problem but for now, we are in something unique: a supply-and-demand-driven recession. Specifically, service supply dried up almost overnight due to virus fears and lockdown orders. Then consumer demand collapsed as people lost those service jobs and, as we will see, those with more money started to save dramatically more, further reducing demand.

My friend (and valued mentor), economist Woody Brock, draws a helpful comparison between this recession and others. I am going to rely upon his June Client Memo for some of these insights and blend them with other analysis and my own views.

Source: Woody Brock

Normally, some kind of trigger or “shock” makes business activity contract. Tighter credit or higher interest rates are often the culprit, not simply falling sales. Unable to finance continued operations, businesses close and lay off workers, who then reduce their consumption. The effects cascade through the economy and recession begins.

This time, the shock came with the coronavirus and our reaction to it. Note, it wasn’t just government-ordered shutdowns. Data now shows consumer spending started falling weeks before governors acted. Retail and service businesses saw store traffic falling and, with risks to employees and customers rising, many closed even when not required to. But the result was the same: Business activity contracted and triggered recession.

Woody observes, and I agree, this hit our economy’s weak spot like a laser-guided missile. Unlike the 1800s or the 1930s or as recently as the 1980s, manufacturing and agriculture no longer dominate. Now the service sector accounts for the vast majority of jobs and GDP. The sudden stop was catastrophic. As Woody outlines (his emphasis):

The good news over the past hundred years (as we have often documented) is that the impact of most any shock on consumption has dropped by some 90%. There are two main reasons for this remarkable decline. First, the advent of unemployment insurance and of two-income families blunted the impact of layoffs on consumption. Second and more important, the percentage of jobs in cyclical industries and farming has collapsed by some 70%, a decline offset by the increase in jobs in the service sector where some 86% of us now earn our living. What matters, of course, is that the service sector is as stable and cycle-free as the other two sectors are not. This is the main reason why the decade-by-decade volatility of GDP has fallen by 85% during the past century. In particular, post-war business cycles have thus been much less severe than they were before the war.

According to this analysis of traditional recessions, both the unemployment rate and the drop in consumption should have and did increase after the initial shock (e.g., a spike in interest rates) occurs—not concurrently. The unemployment rate also peaked after a recovery had already begun.

Note: this is why the current recession is unlike others. Most economic analysis that I read doesn’t distinguish between this service sector implosion and prior recessions of the last 200+ years. Which is why we get all this silly talk of a V-shaped recovery. They are looking at historical models when nothing in history resembles this recession.

This shock, as bad as it is, is only the beginning. More from Woody:

At a causal level, this initial shock caused the unemployment rate immediately to soar to unimaginable levels prior to any formal recession. For the face-to-face contact required to produce many goods and services in the service sector came to an abrupt end once people decided to stay home.

What the market may be missing here is that this initial service sector implosion/shock will cause a more classical recession to follow: thousands of non-service sector businesses will cut back (mining, engineering, auto production) regardless of generous fiscal and monetary assistance. Many firms will fail. As businesses suffer and cut back, they will start laying off workers in the usual manner, and we end up with a proper recession in which layoffs continue until well after an economic recovery arrives.

Thus we will have to add several million more late-stage layoffs to the 32,000,000 early-stage layoffs tabulated to date. The adverse impact of all this on consumer confidence is hard to estimate, but it will surely cause ever further reductions in consumption spending than we have seen to date. The impact on business confidence and investment spending should also be severe.

Theoretically, this new double-decker recession should cause both GDP growth and employment to drop much further and faster than in any other recession on record. And this is exactly what has happened.

If COVID-19 was only the initial trigger, then we still have to deal with the preexisting conditions even if the virus threat goes away. That doesn’t seem likely this year, at least in the US.

In short, a demand-driven recession can’t end until demand returns. It doesn’t necessarily need to be the same kind of demand. Indeed, it probably won’t be. But something must restore consumer spending. A lot of entrepreneurs are spending late nights (and days) trying to figure out how to restore consumer spending.

Choosing Not to Spend

Other problems aside, there is plenty of reason to think the virus-sparked downturn is not over. We know almost 48 million Americans lost jobs since March (the number of unemployment claims filed). Most haven’t felt a severe income loss thanks to government programs and stimulus payments. Some are even making more now.

This isn’t simply a benefit to unemployed workers. The extra payments let them keep paying their bills, which helps their landlords, lenders, and the stores where they shop. (Anecdotally, one friend relayed to me that he was told by the CEO of the company that over 95% of their 50,000 apartments are still paying their rent, but only 50% of their commercial rentals were being paid). That being said, 30% of mortgage holders failed to make payments in June. Even so, cash is still flowing through the economy. That has helped.

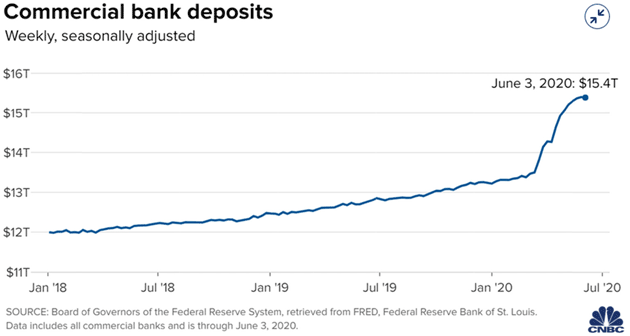

At the same time, less cash is flowing into commerce. The difference shows up in the savings rate and bank deposits. The personal savings rate reached an unprecedented 32% in April. It was still 23% after spending rose in May.

Source: CNBC

Much of this money now flowing into banks would have been spent in restaurants, hotels, and other suffering service businesses. In some cases, it is getting recycled back to those businesses as the banks buy Treasury bonds and the government pumps cash into various programs. But not all of it, and maybe not for long. Some of the CARES Act stimulus measures are set to expire in the next few months.

Mortgage and other lenders have been granting forbearance on debt payments. Courts in many places paused eviction proceedings for renters. Credit card issuers have been generously extending terms. All these help, but they aren’t sustainable indefinitely. They, too, will end at some point, perhaps soon. Then what?

The Wealthy Assume the Fetal Position

One of my most important “reads” every day is Neil Howe and Hedgeye Demography. This morning he starts out by noting a New York Times article and then provides color.

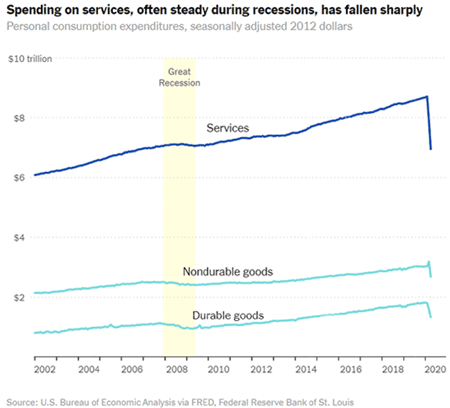

It’s the richest Americans who have cut their spending the most during the pandemic, which is limiting the economic recovery to a larger degree than in past recessions. Unlike other recessions, this one has decimated the service sector, which depends increasingly on consumption by those at the top.

He goes on to relate much of the same analysis as we discussed above.

It has been triggered, in the first instance, by a supply shock: Firms cannot produce or sell to customers. The first firms to get hit are mainly small companies (or sole proprietors) in the service sector—personal services especially. And the first workers to get hit are low-income earners in affluent, urban areas very near to where wealthy people live.

Services, driven by millions of small firms (restaurants alone comprise nearly 15% of all US employers), typically help power our economy through a recessionary patch. This time, services are getting hammered.

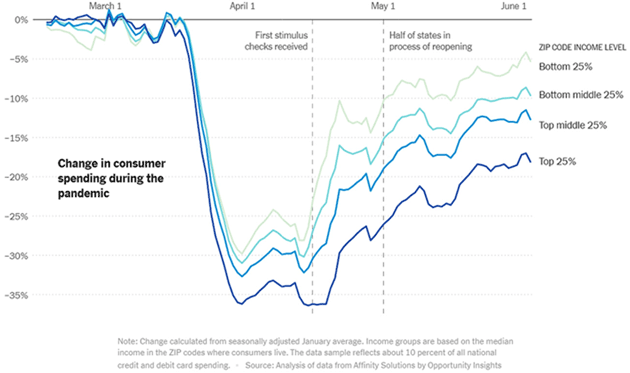

Source: Hedgeye

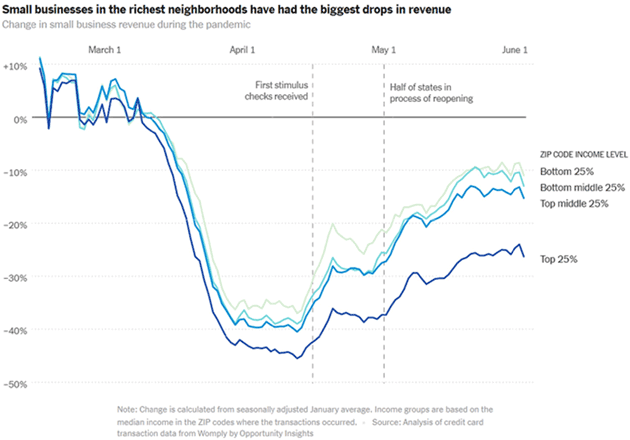

But then we get to the part that really gives us truly valuable insight. The data below is daily credit card receipts which can be tracked by ZIP Code. A Harvard think tank called Opportunity Insights breaks down the data by average household income within a particular ZIP Code. No surprise, the data tracked remarkably closely, both before and after the recognition of the pandemic and lockdowns. But notice what happens after the first stimulus checks are received. Those getting those checks, presumably not the wealthy, spend them. The top 25% of wealth-related ZIP codes spend dramatically less. And that is the problem.

A few years ago, former Dallas Fed president Richard Fisher, speaking at my conference, was asked how he had positioned his own portfolio. He quipped, “The fetal position.” That is precisely what we are seeing today: extraordinarily high savings rates and less spending from those who are uncertain about the economy.

Source: Hedgeye

Not surprisingly, that means that small businesses in those neighborhoods have had the biggest drops in revenue.

Source: Hedgeye

What kind of businesses are we talking about? Mainly small firms, contractors, and professionals who provide services to wealthy people in relatively wealthy neighborhoods: high-end restaurants, boutique and fashion shops, spas, gyms, therapists, theaters, florists, and so on. Businesses in Manhattan, especially on the upper east side, have been flattened—while businesses in Harlem and South Bronx have been relatively unscathed.

So what are the rich doing with their money? For now, at least, they're not spending it. Past recessions have usually been accompanied by some rise in the personal savings rate—with a disproportionate share of that rise coming from the affluent. This time, we're seeing a grotesquely exaggerated response. The average personal savings rate has skyrocketed to an unprecedented 33% in April. And nearly all of this gain has come from the affluent. According to the Harvard researchers, over half of the consumption decline in April and May came from the top quartile of households. Meanwhile, the lowest quartile has seen virtually no overall decline in consumption. And that is in part thanks to PPP and UI bonus dollars flowing to the very workers who work (or used to work) in Beverly Hills or Sausalito or along Chicago's Mag Mile.

Over half the spending decline in the current recession is coming from the top 20% income group. The lowest group has only seen aggregate spending drop 5%, thanks to unemployment insurance. Government programs have helped the economy stumble along.

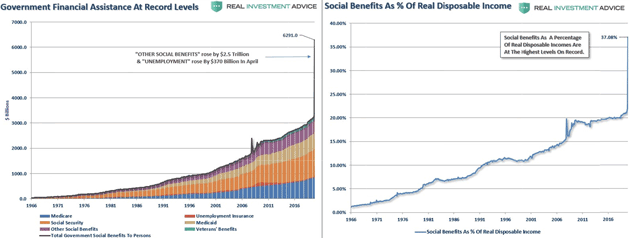

My friend Lance Roberts at Real Investment Advice posted the charts below on Twitter. Note that social benefits (government checks of one form or another) almost doubled to 37% of disposable income in the last few months. The unanswered and difficult question is what will happen if those programs are cut back?

Source: Lance Roberts

The next phase of this recession will be when demand stays low because people lack spending power. The open question is how widespread it will be, and that depends largely on health-driven behavioral decisions.

Inevitable and Unacceptable

Spending won’t recover to prior levels unless people feel safe. I emphasize “feel” because perception is what counts. Controlling the coronavirus is necessary but not sufficient.

Last week I explained how widespread mask-wearing is the best and least expensive economic stimulus program available to us. Older people, those with health conditions that make them vulnerable, and many others simply won’t go back to normal when they see large numbers of unmasked people walking around in public.

Unfortunately, that is easier said than done. Legal mandates and social shaming (you cannot imagine how I hate writing those words) may help but not enough, and can even backfire by breeding resentment. This is a real problem for businesses in which crowds and small spaces are unavoidable.

The airline industry is in turmoil. Traffic counts are coming back but are still way below breakeven rates. Hotels are even worse. Not to mention all the businesses that need airlines and hotels to bring customers. Conventions and tourism are a substantial part of the economy, representing millions of jobs. They can’t come back under these conditions. That alone is enough to keep the economy in recession for a long time. You can be optimistic about much of the economy (I certainly am) but a 90% recovery is just not enough.

But that’s really the best-case outlook. If the outbreaks that are currently intensifying in Arizona, Florida, Texas, and elsewhere get bad enough to make consumers stay home and businesses close again (whether ordered to or not), all bets are off. Texas has already paused its reopening plans, with the governor ordering bars closed again.

Efforts to control the virus, while necessary, have an economic cost. It looks like the European Union will refuse entry to American travelers, as well as others from areas where they deem the virus is insufficiently controlled. The same is happening within the US as recovering states like New York require quarantines for travelers from other states where cases are growing.

International and interstate travel is pretty low anyway, but these measures will reduce it further. Now even some urgent, no-other-way trips can’t happen. This will have unpredictable but potentially severe impact on some businesses. If your factory is closed because you need a machine repaired, and the only person who can repair it can’t enter your state, you are in deep trouble. So are your employees, suppliers, customers, and shareholders.

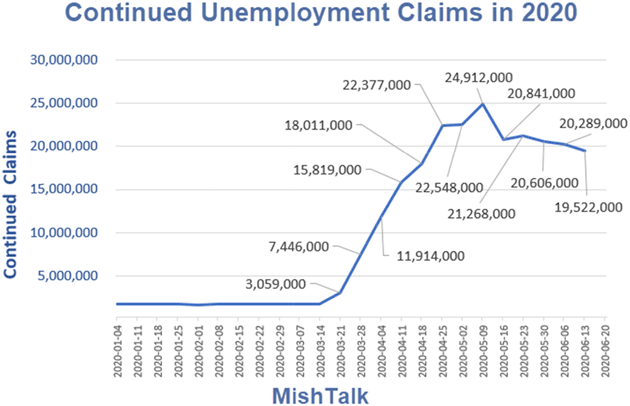

When NBER said this recession would have “different characteristics and dynamics” than others, the committee wasn’t kidding. This is unlike anything we have seen before. At least 20 million people have been out of work for eight weeks. (H/T Mike Shedlock) Initial claims are still about 1.5 million per week, though down from almost 7 million. Again, 47 million of our neighbors have lost a job. Some are now slowly going back to work. But by all accounts, that work looks significantly different.

Source: MishTalk

I think governments everywhere, but especially in the US prior to the election, will continue their stimulus programs. But at some point, we cannot maintain the current level of spending. I think it is likely we taper off rather than simply cut them wholesale, but no one really knows.

And remember, TANSTAAFL (There ain’t no such thing as a free lunch) is still an economic law. We may pay for it via lower growth and thus fewer opportunities for everyone, or inflation, other ways, or combinations thereof. That being said, doing nothing would mean an economy worse than the Great Depression. We have no good choices. We’re simply picking the best of some pretty bad choices. Ugh.

When economists talk about the shape of a recovery, relying upon the past data, my best advice is to ignore them. We are in the Stumble-Through Economy. Everything is going to be different in the future. The old playbook won’t get us out of trouble this time. Every business, every family, every investor will have to create a brand-new playbook.

Think of it this way. From time to time the gods of football change the rules. Coaches and players adapt. Now imagine every rule change of the past 40 years was enacted in one month, in the middle of the season, and the referees instructed to rigorously enforce them.

It is time to throw out the old playbook and create a whole new game plan. Nearly everything in the world is going to be repriced. Some of those changes will be minor but some will be significant. In the middle of all this, governments and central banks will to continue to change rules just to make the challenge a little more difficult.

In future letters, I will begin to explore options. I can’t promise they will all be pretty, as I know they won’t be, but they will be as real as I can make them. I can also say that some are going to be pretty fantastic. And for what it’s worth, I am in the same boat with you. Stay tuned…

Puerto Rico and Dust Bowls

I grew up on the edge of West Texas where dust storms were a regular feature. It turns out that the storms are also an annual feature in Puerto Rico, and indeed the southeast US.

For whatever meteorological reason, about this time of the year a massive amount of sand from the Sahara Desert is sucked up into the high atmosphere and gets blown across the Atlantic, over Puerto Rico, and then onto the southeast and even into Texas. The locals explained the phenomenon to me, pointing out this was a particularly bad year.

The good news is that theoretically the sand reduces the ocean temperature which may reduce the hurricane season’s severity. It was weird to have the sun look like a bright moon at 3:00 in the afternoon in the tropics. It lasted for a few days and now is apparently reaching the mainland.sucked up into the

Source: WRAL Weather

My daughter Tiffani sent me this tweet:

Source: Twitter

One person replied, “In West Texas, we call this Tuesday.” You have to love gallows humor. And you should be following me on Twitter, and if you like this letter, go back to the top and tweet out your own comment with this link. Thanks. You have a great week!

Your making a new personal playbook analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All