As funding strains appeared in March, the USD surged. Then the Fed stepped in with massive foreign exchange swaps as a way to lend USD to foreign central banks, intended to ultimately be lent to borrowers in need of USD. As F/X swaps reached almost $500 billion, allocated heavily to Japan and Europe, the USD experienced a 7% correction, from 1,300 on the BBDXY to 1,200.

Now, as liquidity strains have been addressed, the F/X swaps are rolling off, leading to an outright decline in the Fed’s balance sheet last week. As the swaps roll off, the USD is rising again, up about 2% in the last couple weeks.

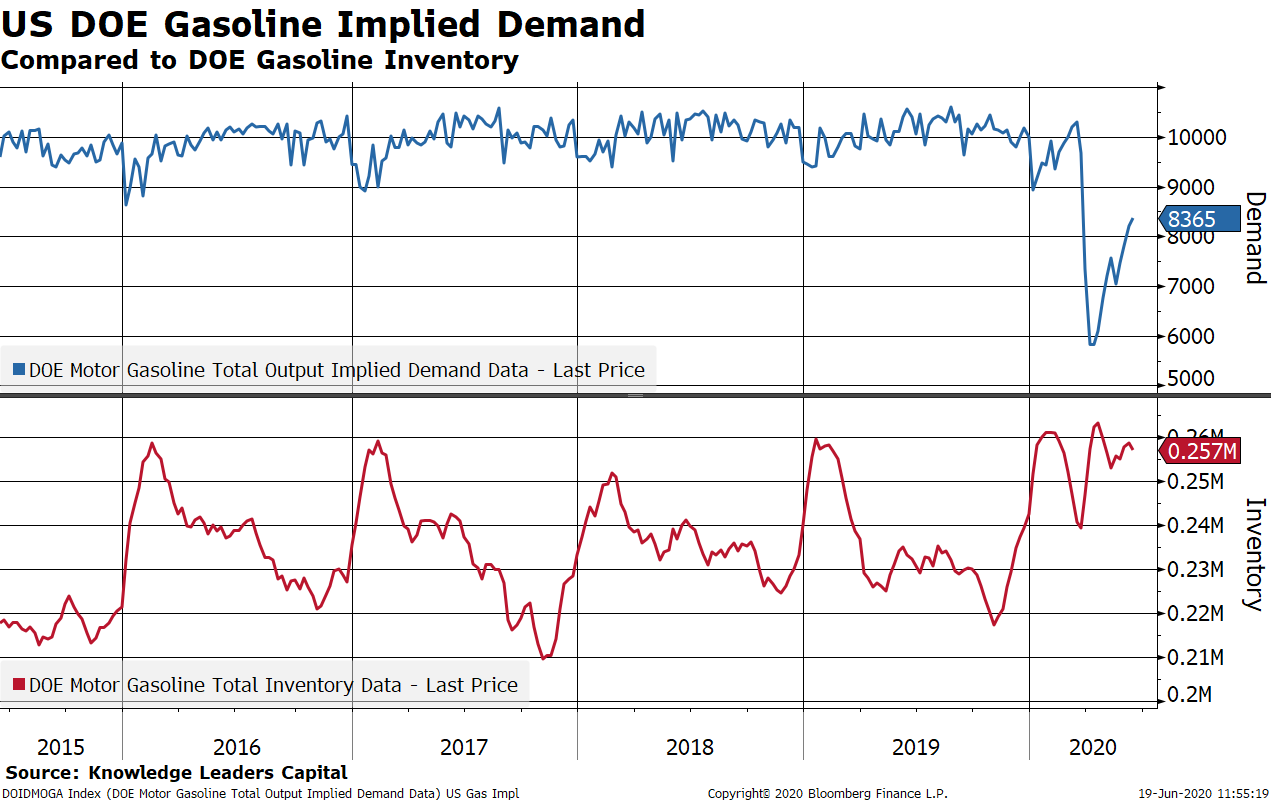

In our opinion, had the F/X swaps not occurred the USD was naturally on a glide path higher as petroleum inventories went through the roof. The BBDXY has a pretty good historic fit with the inventory of petroleum products—both crude and refined—not including the Strategic Petroleum Reserve (SPR).