COVID-19 has supplied the catalyst for a secular change in the role of central banks. Providing governments with ammunition to fight the virus is now the overriding goal, and this means keeping bond yields pinned close to zero for the foreseeable future.

The Changing Role of Central Banks

Throughout history, central banks have performed three main roles: providing low and stable inflation (price stability); safeguarding financial stability; and helping governments pay their bills (monetization). The importance of these different roles varies over time, and they often conflict. In the 30 years prior to the global financial crisis (GFC), for example, most central banks focused exclusively on price stability. But that approach led to the biggest financial crisis since the Great Depression, so central banks added financial stability to the mix (nominally, at least).

Direct monetization has fallen out of fashion in recent decades—with the odd, noteworthy exception (i.e., Venezuela, Zimbabwe). But in the past, central banks have often helped governments pay their bills, particularly during wartime. So it’s not surprising that they’ve stepped in to give countries the financial firepower to confront COVID-19 without triggering a self-defeating increase in bond yields.

A Bad Time for a Crisis

Public sector balance sheets weren’t in great shape coming into the coronavirus crisis, and they’re soon going to look an awful lot worse. At the end of last year, the combined government debt of the G7* group of large industrial nations stood at almost 120% of gross domestic product (GDP), higher than at the end of either the first or second world wars. This year, with budget deficits set to move sharply higher and output likely to collapse, that number will probably rise to something like 140% of GDP.

There was a time—not that long ago—when that sort of number would have been considered unsustainable. At the beginning of Europe’s sovereign-debt crisis, Greece’s debt-to-GDP ratio was 146%. Such elevated debt ratios are no longer considered unsustainable because interest rates are so low. But just how low do interest rates need to be for the major developed economies to remain solvent?

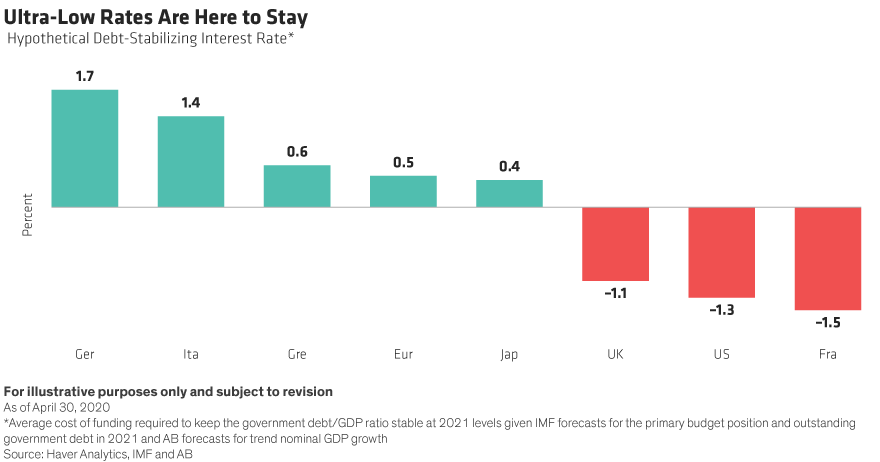

What Level of Interest Rates Keeps Debt-to-GDP Stable?

To explore this point, we calculated debt-stabilizing interest rates (DSIRs) for select developed economies. This simple calculation estimates the average cost of funding needed to keep the debt-to-GDP ratio stable. It’s based on three variables: the level of government debt, the size of the primary budget balance (excluding interest payments) and projected nominal GDP growth. For illustrative purposes, we use the International Monetary Fund’s 2021 forecasts for government debt and the primary balance, and our own projections for nominal GDP growth (Display).

According to our simulation, DSIRs range from a high of 1.7% in Germany to –1.1% in the UK, –1.3% in the US and –1.5% in France. This doesn’t mean the US will push its policy rate into negative territory—indeed, we continue to think that unlikely. But it does mean that government debt will move onto an explosive path unless the average cost of funding is kept very, very low—particularly in countries with negative DSIRs. And that’s where central banks come in.

In recent weeks, many central banks have either launched, reopened or expanded large-scale government-bond purchase programs. This is similar to the GFC policy response but there are key differences. The coronavirus crisis response has been faster and broader: the US Federal Reserve bought $1.5 trillion of Treasury debt in March and April, something that took four years to accomplish during the GFC. And we expect much more to come. The goal is different, too: central banks now talk much more openly about the link between their purchases and government financing costs.

Fiscal and Monetary Policy Joined at the Hip

Very few central bankers would be willing to admit that they are monetizing government deficits. But that’s exactly what they are doing and, more importantly, it’s precisely what they should be doing in current circumstances. Just as during wartime, central banks currently have little option but to step into the nexus that blurs the distinction between monetary and fiscal policy, with the two effectively joined at the hip.

In time, governments and voters will have to decide how best to deal with very high levels of public sector debt. Default, austerity and higher inflation are among the possible options. Alternatively, they could choose to downplay the significance of government debt, as some advocates of modern monetary theory would recommend. But those are questions for another day. And until then, what’s important is that interest rates and bond yields remain low.

In recent weeks, central banks have clearly shown that they have both the ability and the willingness to keep a lid on bond yields. So at a time when the global outlook is subject to so many uncertainties, our highest-conviction view is that interest rates and bond yields will continue to be pinned close to, and in some cases below, zero. And that’s likely to be the case long after the coronavirus crisis has passed.

*The G7 is Canada, France, Germany, Italy, Japan, the UK and the US.

Darren Williams is Director—Global Economic Research at AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein