Join us and Calamos Investments for our upcoming webinar: Adding Convertible Strategies to Your Playbook on May 7th at 2 pm ET. Register now.

In a turbulent period for the markets, Calamos has been hosting a Calamos CIO Conference Call series for investment professionals. Below are notes from a call Thursday, April 30, with Michael Grant, Co-CIO, Sr. Co-Portfolio Manager, Head of Long/Short Strategies. To listen to the call in its entirety, go to www.calamos.com/CIOlongshort-4-30

For highlights on last month's calls, see this post.

While predicting that “economic activity in March and April will be the worst of our professional careers,” Grant nonetheless says markets see light at the end of the tunnel that includes economic recovery by July.

“Financial markets are communicating a consistent message: namely, the contours of imminent economic recovery are tracking better than what anyone’s sensibilities would suggest,” he said.

A Sustainable Equity Recovery, the Result of Extraordinary Action

Grant acknowledged that many investors are confused by an apparent paradox: the rapid and uninterrupted recovery in equities since the March lows despite the most severe global recession on record. The rally is “special,” he agreed, and the result of decisive initiatives of the Federal Reserve.

“The reality is that U.S. policymakers have quashed the liquidity and solvency risks of this event. History is likely to judge them well,” said Grant.

“The resilience of the Western consumer combined with unparalleled policy support,” he continued, “will minimize financial stress with the consequence that by mid-year, the global output cycle is well on its way to regaining its pre-virus capacity.”

Further, Grant believes that April’s equity recovery is sustainable, which could disappoint those waiting for a retest. “There is a material likelihood that clients who sold at [March] lows will never see these entry points again,” he said.

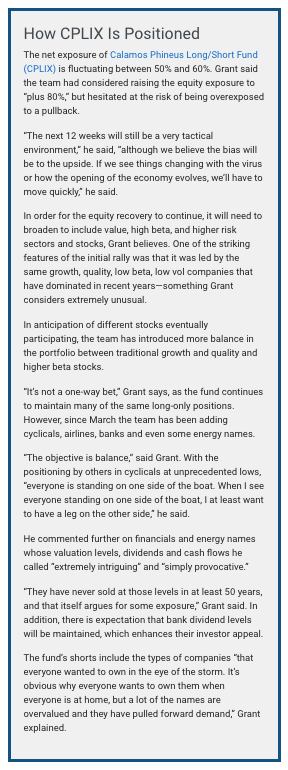

It was in March when the fund moved to a net long exposure fluctuating between 50% and 60%, which has been maintained. According to Grant, the team believed that the COVID-19 spread, incidence and fatality would “inflect positively” while understanding that the economic and corporate data would be “ugly.” They were weighing whether to add further hedges on the assumption of a retest of the March lows until the Fed’s “game-changing” actions on April 9.

“Chairman Powell noted that the economic calamity was not the result of ‘bad actors.’ He thus had no misgivings relating to moral hazard and added, ‘We will make you whole’…I want to emphasize how extraordinary these policy actions are,” said Grant.

Grant parts ways with those who are assuming less optimistic outcomes based on “typical” recessions.

“This will be the first economic crisis where policymakers have kept credit markets functioning in the midst of the downturn. This difference alone should convince you to think differently about how economic activity could evolve in coming quarters,” he said.

Today’s crisis might be compared to a natural disaster, which produces sudden stops in economic activity including spikes in unemployment and a collapse in production. Natural disasters are different from a traditional recession in that the damage is immediate and normality resumes within a year, Grant said.

The CPLIX team is expecting 0% revenue growth and a decline of 20% in corporate earnings in 2020. This assumes that U.S. GDP recovers in Q3 and improves further in Q4.

As he’s said before, the team believes that the recession this year will mark the end of the cyclical bear, not the beginning of one.

How the Economy ‘Opens’

Grant offered a timeline for how the economy starts back up again, considering both the virus and political considerations.

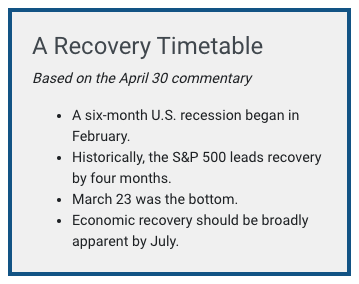

Virus: “We concluded in March that improvement was a matter of weeks, not months. That was a high conviction view (see this commentary) and it has proven correct,” said Grant. He cited two developments that have occurred this week that he believes confirm “we have entered the decline phase” of the crisis:

- New York City reported a breakthrough in its COVID-19 case count at 1,613, or the first sub-2,000 day in more than 30 days and now 78% off peak levels.

- More than 50% of U.S. counties report case levels that are 50% or more off peak. This implies more than half of the U.S. by population is further in the decline phase.

The trend toward lower fatality rates is visible everywhere, added Grant, including New York.

Politics: “It is inconceivable that [President Donald] Trump will lock down the U.S. economy into a Great Depression and, seemingly, certain electoral defeat. This argues for economic activity to return to normal by summer—with a material resumption in June,” said Grant.

The team expects the end of the lockdowns to trigger “immense pent-up demand,” notably in the developed world where many have been paid a high percentage of normal income on furlough.

“When do we worry about some of the other issues?” Grant asked. “Our view right now is that the markets just want to see recovery. There will be a stage when we’ll have to decide how much of the demand problem is just delayed, and we come back easily, and how much has been destroyed. I just don’t think we have to worry about that right now.”

Grant closed his prepared remarks with this analogy:

“Every night, we go to bed with the knowledge that sometime around 2 a.m., U.S. economic activity goes to zero. And yet, the overnight futures do not decline by 50%. There is no liquidity or solvency crisis. Instead, financial markets are entirely comfortable looking forward to normality and that is exactly where they pick up the narrative.

“That is the logic that underpins equities today. It has been only eight weeks since COVID-19 washed onto U.S. shores. Cycle times for economic activity, employment and, of course, financial markets have been stunningly compressed. It is probably this rapidity of events that allows markets to look forward to the light of morning.”

Before investing carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-800-582-6959. Read it carefully before investing.

Opinions are subject to change due to changes in the market, economic conditions or changes in the legal and/or regulatory environment and may not necessarily come to pass. This information is provided for informational purposes only and should not be considered tax, legal, or investment advice. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund's prospectus.

Past performance is no guarantee of future results. As with other investments, market price will fluctuate with the market and upon sale, your shares may have a market price that is above or below net asset value and may be worth more or less than your original investment. Returns at NAV reflect the deduction of the Fund’s management fee, debt leverage costs and other expenses. You can purchase or sell common shares daily. Like any other stock, market price will fluctuate with the market. Upon sale, your shares may have a market price that is above or below net asset value and may be worth more or less than your original investment. Shares of closed-end funds frequently trade at a discount which is a market price that is below their net asset value. You can purchase or sell common shares daily. Like any other stock, market price will fluctuate with the market. Upon sale, your shares may have a market price that is above or below net asset value and may be worth more or less than your original investment. Shares of closed-end funds frequently trade at a market price that is below their net asset value.

The principal risks of investing in the Calamos Phineus Long/Short Fund include: equity securities risk consisting of market prices declining in general, short sale risk consisting of potential for unlimited losses, foreign securities risk, currency risk, geographic concentration risk, other investment companies (including ETFs) risk, derivatives risk, options risk, and leverage risk. As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present additional risk due to potential for greater economic and political instability in less developed countries.

Equity Securities Risk. Equity investments are subject to greater fluctuations in market value than other asset classes as a result of such factors as the issuer's business performance, investor perceptions, stock market trends and general economic conditions. Equity securities are subordinated to bonds and other debt instruments in a company's capital structure in terms of priority to corporate income and liquidation payments. The Fund may invest in preferred stocks and convertible securities of any rating, including below investment grade.

Short Selling Risk. The Fund will engage in short sales for investment and risk management purposes, including when the Adviser believes an investment will underperform due to a greater sensitivity to earnings growth of the issuer, default risk or interest rates. In times of unusual or adverse market, economic, regulatory or political conditions, the Fund may not be able, fully or partially, to implement its short selling strategy. Periods of unusual or adverse market, economic, regulatory or political conditions may exist for extended periods of time. Short sales are transactions in which the Fund sells a security or other instrument that it does not own but can borrow in the market. Short selling allows the Fund to profit from a decline in market price to the extent such decline exceeds the transaction costs and the costs of borrowing the securities and to obtain a low cost means of financing long investments that the Adviser believes are attractive. If a security sold short increases in price, the Fund may have to cover its short position at a higher price than the short sale price, resulting in a loss. The Fund will have substantial short positions and must borrow those securities to make delivery to the buyer under the short sale transaction. The Fund may not be able to borrow a security that it needs to deliver or it may not be able to close out a short position at an acceptable price and may have to sell related long positions earlier than it had expected. Thus, the Fund may not be able to successfully implement its short sale strategy due to limited availability of desired securities or for other reasons.

Each fund has specific risks, which are outlined in the respective funds' prospectuses. The general risks involved in investing in a closed end fund include market volatility risk, dividend and income risk, and loss of investment risk. Please refer to each fund's prospectus, annual and semi-annual reports at www.calamos.com for complete information on the fund's performance, investments and risks.

Beta is a measure of the volatility, or systematic risk, of a security or a portfolio in comparison to the market as a whole.

802010 0520

© Calamos Investments

© Calamos Investments

More Alternative Investments Topics >