Want to read more by Ashmore Group? Visit their Featured Firm page here

Global stock markets have been struck by a triple shock; global pandemic, energy price war and market rout from full valuation levels in developed markets. Each of these types of shocks has been seen, and recovered from, previously. The simultaneous nature of the events though is unprecedented and so too have been the speed and magnitude of market reactions. For those investors able to rationalise, identify fundamental ‘winners’ and manage their exposure actively, this market chapter may also prove to offer unprecedented investment opportunities.

Markets behaving badly

It should not come as a surprise that Emerging Markets were first-in to the 2020 market sell off. After all, they are still burdened with the tag of ‘risk assets’ despite fundamentals, in the vast majority of countries’ cases, pointing to the contrary. So, while YTD global emerging and developed market indices have been sold off uniformly, a good degree of Emerging Markets perceived risk premium had already been priced.

From the peak of this Emerging Markets ‘cycle’ from 26 January 2018 to 31 March 2020, the MSCI Emerging Markets index has returned -29.7% while the S&P has fallen by a fraction of that amount at -6.0%. Historically, such market distortion has created opportunity as Emerging Markets have also proved to be the first-out and to lead the market recovery. This paper provides context to recent market behaviour; assesses the trajectory of macroeconomic data; reviews current policy stance; and finishes with market implications. In brief, while Emerging Markets were the first to bear the pain of the triple shock, they also look well placed to be among the first to recover.

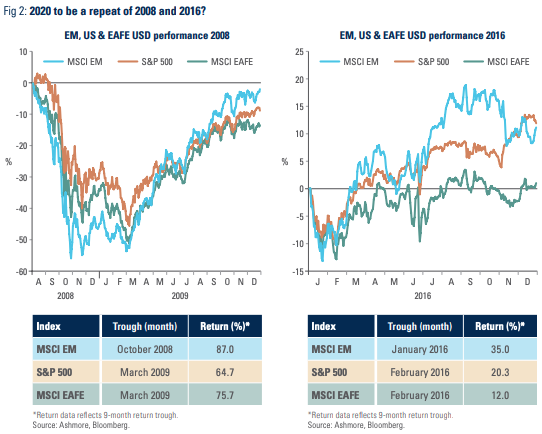

Fig 1: Emerging Markets were first to fall

This was evident in the previous two severe market dislocations. Emerging Markets troughed first in October 2008 and subsequently returned 87.0% over the following nine months. Meanwhile, US and EAFE markets bottomed five months later and rebounded by less. It was a similar, albeit less dramatic, story in 2016’s sell off and recovery.

Market liquidity has also seen distortion. Liquidity for equity markets has been largely ‘normal’, albeit the magnitude of intraday market gyrations has led to reduced visibility of potential realised prices. However, the perception of a potential shortage of liquidity has led investors to value cash above all else. The typical safe haven, gold, has fallen double digits before recovering and money market funds have seen record inflows.

Highly liquid stocks have seen disproportionate selling pressure as investors have sold what they can rather than perhaps what they want. The historical premium that stocks’ depository receipts trade at compared to the equivalent local line has also evaporated, in some cases. These factors are temporary and will reverse, just as they did it 2008 and 2016.

Macroeconomic trajectory leaders

Emerging Markets are heterogeneous comprising a myriad of economies each at a different stage of development, maturity and with a different balance of growth drivers, not to mention currencies and stock market compositions. Evidently, they will consequently all cope, tackle and recover from the triple shock differently. Hence, selectivity as an active investor is key. The good news is the Emerging Markets universe is so large and dynamic there are invariably winners, as well as losers, in every macroeconomic backdrop.

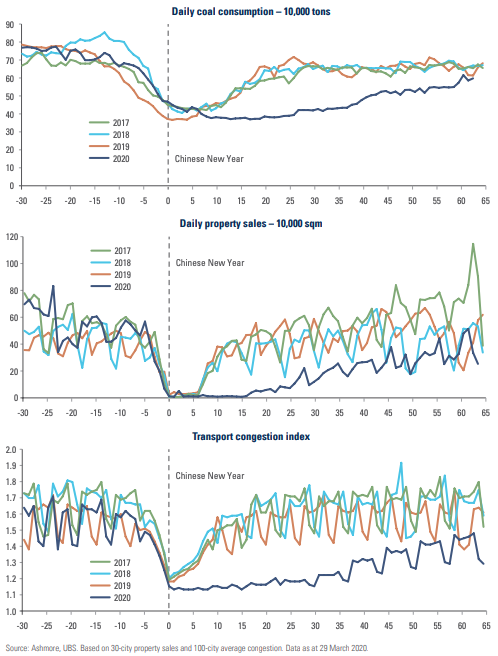

In the case of COVID19, China was the first to see it, first to supress it, first to see related slowdown and is now the first to show sequential normalisation. South Korea and Taiwan are notably not far behind. These three countries comprise approximately 60% of the MSCI EM index.

By referencing the trajectory of China and North Asia, investors are increasingly able to quantify better the potential impact, as well as judge the potential speed of recovery for different economies. For example, over the month of February on a year-on-year basis, Chinese electricity consumption fell -10.1%, retail sales -20.5% while auto sales fell -81.2%.

However, since then activity levels have generally been improving on a sequential basis. The vast majority of Chinese provinces have lowered their emergency level and low risk regions (where most of manufacturing hubs are located) have been ordered proactively to resume full operations. The mosaic of hard and soft data implies industrial activity levels around 80% of ‘normal’ levels.

Meanwhile, March South Korean export data, based on 20 day indicative basis, pointed to a 10% year-on-year improvement buoyed by technology demand. On-line services and virtual technologies have, unsurprisingly, seen positive trajectory, although investors should be wary of changes in product mix demand. Fashion may take a back seat in confinement. By using North Asia as a template, investors can judge trajectories elsewhere better and also identify potential ‘winners’.

The above stands in stark contrast to developed markets, where macroeconomic trajectories are still deteriorating. Over the week ending 21 March, US initial jobless claims increased by 3.3 million, a record number that is ahead of total current existing claims.

Corporate guidance has been quiet and investors need to be mindful of the impact of deterioration in developed markets demand on those more open emerging economies and export orientated corporates. Likewise, the risk of ‘second wave’ effects of COVID-19 should not be understated. In such a situation, the ability for China and North Asia to respond looks comparably strong, given a combination of strong equipment supplies, the ability to implement selective confinement measures and enforce them effectively. Clearly, as per the opening remark in this section, the impact of COVID-19 on each country will be different and should different scenarios unfold an active approach to investing will only prove more crucial.

Fig 3: Improving trajectories in China

Policy response goes from accommodative to highly stimulatory

The proliferation of central bank and fiscal support globally has been unprecedented. The reaction has also been swifter and more synchronised than during the Global Financial Crisis. On the monetary side, developed markets central banks have already depleted their limited resources. To support price stability and liquidity, interest rates have been cut to zero; Quantitative Easing programmes have been enacted/expanded; and reserve and capital requirements cut. This has been combined with significant fiscal stimulus and support programmes. Monetary stimulus has ‘no boundaries’ and globally easier USD financing conditions are a positive for Emerging Markets domestic economies. While the US Dollar benefitted from an initial flight to safety, all else equal, this may prove temporary given the sharp increase in its supply.

China was the first to respond with policy support and is expected to be the first to benefit assisted by its command economy. As the largest consumer and producer of Emerging Markets goods, this is important for Emerging Markets as a whole. It did so pro-actively with liquidity provision and targeted fiscal measures to support sections of the economy most vulnerable. Further fiscal support is anticipated, notably in the form of healthcare and fixed asset investment projects. Most recently, the authorities have initiated consumer coupon programmes to encourage domestic consumption. Such a measured response, coupled with a rich tool kit at its disposal, places China well to sustain, or expand, policy support.

Emerging economies are in a much better shape than developed markets and also compared to the Global Financial Crisis. This includes typically better-balanced current accounts, floating (and competitive) currencies and liabilities funded in local currency. This strong fundamental footing has enabled central banks to respond to the triple shock with counter-cyclical monetary easing. This is a positive from a domestic economic growth perspective, although equity investors should be wary of potential reduced FX visibility and its impact on locally generated earnings reported in US dollars.

The earnings cycle

It takes time for stock analysts to assess, model and extrapolate the positon of a corporate in its current operating environment, especially when the latter is in a state of flux. Consequently, headline earnings estimates have limited value at such times of dislocation.

This is reflected by referencing Ashmore’s proprietary aggregation of USD unweighted net income growth market expectations. At the beginning of the year, 2020 market expectations were 14%, by end February 12%, mid-March 9% and by end March 3%. This also highlights the importance of assessing top down as well as bottom up factors as a means of highlighting improving/deteriorating trajectories. This is particularly relevant in Emerging Markets given their dynamism and heterogeneity.

Emerging Markets are likely to fare differently in the current triple shock than would have been the case a decade ago. Two reasons are stock market breadth and composition. Market breadth offers investors greater selectivity while the composition changes the earnings outlook.

The importance of commodities (energy plus materials) has approximately halved in the MSCI Emerging Markets index while technology/communications has doubled. For MSCI China, in 2008, telecoms and industrials were around 35%, financials 29% and energy 18% of the market capitalisation. In 2020, they are 6%, 19% and 3% respectively. Communication Services, Consumer Discretionary and IT now account for 55%. This all bodes well in an increasingly virtual world. In China’s case, corporate revenues are also biased towards the domestic economy (7% of sales from overseas) in comparison to the S&P 500 with over 40%. However, investors should also be wary of policy and fundamental ‘losers’ in the current backdrop, not least the risk of misalignment of interests between authorities under social pressure and minority shareholders.

Market implications point to extremes

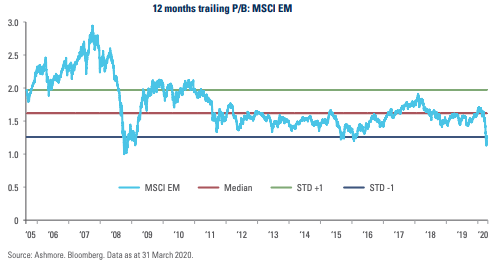

Aggregate market and country valuations typically have limited value in Emerging Markets. After all, these economies and their markets are dynamic, subject to meaningful evolution and consequently unlikely to mean revert. So, while assessment of stock valuations are crucial to investment, the same cannot be said top down. The exception to this rule is at times of extremes, where we are today.

The MSCI Emerging Markets has been trading around 1.1x trailing Price-to-Book. To put this in some context, the P/B lows during the Global Financial Crisis were also 1.1x. The 2016 meltdown saw valuations around 1.2x. By way of reference, the S&P 500 trades around 2.7x P/B compared to 1.8x in the GFC. Investor positioning was already light in Emerging Markets heading into the triple shock and this has only been exacerbated.

Fig 4: Valuations are at extremes

What will it take for markets to normalise and to allow investors’ heads to be turned by the fundamental drivers highlighted in the sections above? It is likely a combination of greater visibility of the effects of COVID-19 on economies, which is improving day by day; the virus active rate trajectory as well as progress towards therapeutic treatment; and policy response.

No one is any the wiser whether to invest today or tomorrow. Yet there are enough signals to suggest, selectively, that there are extraordinarily attractive opportunities for active investors in those areas first-in and likely first-out of the triple shock.

No part of this article may be reproduced in any form, or referred to in any other publication, without the written permission of Ashmore Investment Management Limited © 2020.

Important information: This document is issued by Ashmore Investment Management Limited (‘Ashmore’) which is authorised and regulated by the UK Financial Conduct Authority and which is also, registered under the U.S. Investment Advisors Act. The information and any opinions contained in this document have been compiled in good faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Save to the extent (if any) that exclusion of liability is prohibited by any applicable law or regulation, Ashmore and its respective officers, employees, representatives and agents expressly advise that they shall not be liable in any respect whatsoever for any loss or damage, whether direct, indirect, consequential or otherwise however arising (whether in negligence or otherwise) out of or in connection with the contents of or any omissions from this document. This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any Fund referred to in this document. The value of any investment in any such Fund may fall as well as rise and investors may not get back the amount originally invested. Past performance is not a reliable indicator of future results. All prospective investors must obtain a copy of the final Scheme Particulars or (if applicable) other offering document relating to the relevant Fund prior to making any decision to invest in any such Fund. This document does not constitute and may not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment in any such Fund. Funds are distributed in the United States by Ashmore Investment Management (US) Corporation, a registered broker-dealer and member of FINRA and SIPC.