Spring Quarterly Commentary

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Let me not pray to be sheltered from dangers, but to be fearless in facing them. Let me not beg for the stilling of my pain, but for the heart to conquer it.”

- Rabindranath Tagore, 1861-1941 Polymath, poet, musician, artist

This letter is one of the more difficult ones to write because things are changing so rapidly. We caution readers that we are not epidemiologists, but it is our job to try, to the best of our ability, to figure out what is going on, and that’s what we attempt to do with this letter. Such is the nature of predictions, that much of what we say may ultimately prove wrong, and some thoughts will be out of date even by the time you read this. This letter is also longer than usual as there is more to talk about.

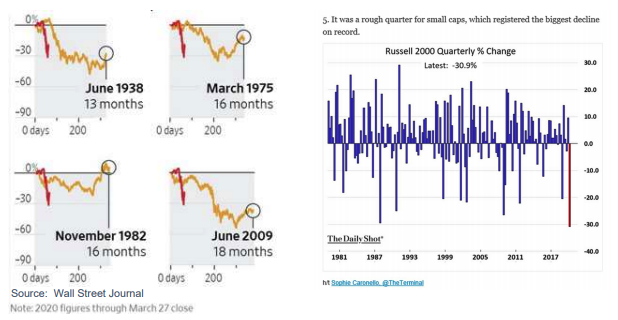

No one needs to read this letter to learn that the novel coronavirus has vastly altered the financial landscape and the way we live. The impact on financial markets has not only been profoundly deep, but also incredibly sudden. When the Tech Bubble “burst” in the year 2000, it took 18 months for the S&P 500 Index to decline 32% from its peak. In the current crisis, it took only 16 days. Even more incredibly, by some people’s definitions (not ours), the bear market was not only the fastest ever, but also the shortest ever, with stocks already having rallied more than 20% off their bottom1. The chart atop the following page is over a week old but does a good job of showing the abruptness of the current bear market (red line on the chart) versus other historic recessionary declines in the S&P 500 Index.

As always, major indices such as the Dow or S&P 500 “hide” much of the damage. For example, small cap stocks logged their worst quarter ever, with the Russell 2000 down almost 31%.

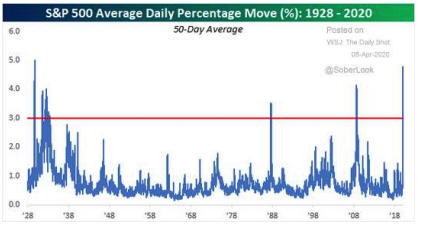

By many measures, we also just experienced the most volatile stock market of all time. While normally a 1% move would grab one’s attention, 3%+ moves have recently become the daily norm.

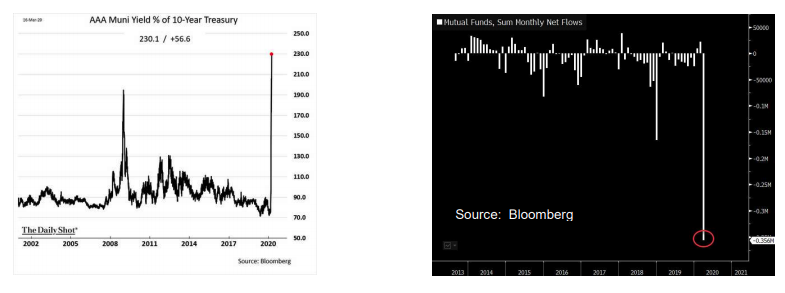

Market chaos was not just restricted to stocks. The extra yield required by investors in even the safest, most highly rated municipal bonds rocketed past the levels seen in the 2008 financial crisis. More broadly, mutual fund investors headed for the exits, as markets exuded once-in-a-century extremes... for the second time in twelve years.

These examples serve as but a small sample of this quarter’s tumbling, soaring, and wilding gyrating financial markets. No matter where you look, from currencies to spreads to CMOs to swaps, things have been really, really, crazy.

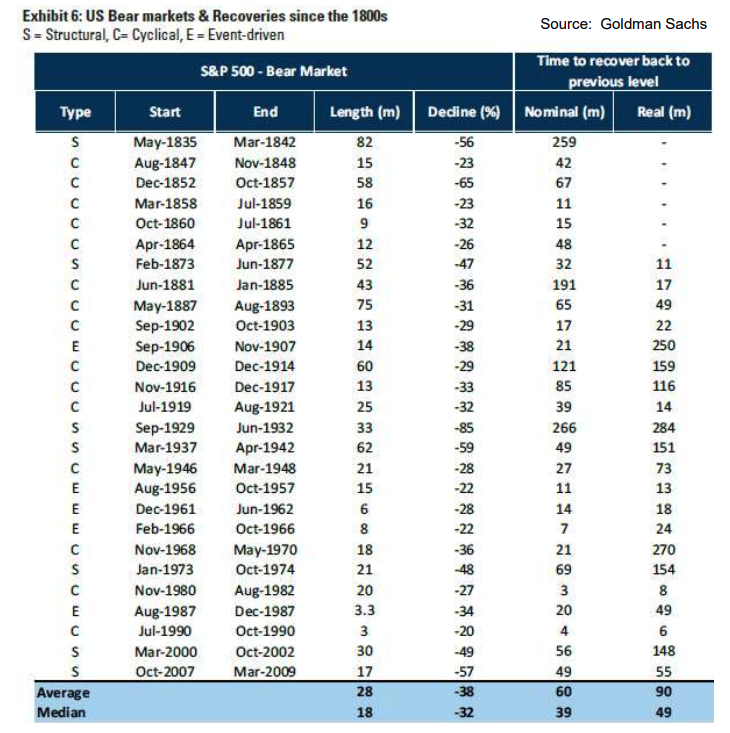

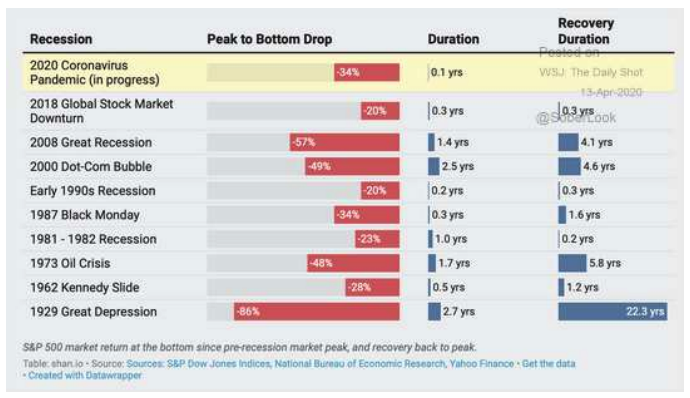

Before we start analyzing the circumstances of this specific bear market, it is worth setting a baseline by looking at some statistics on bear markets in general. The average bear market (defined as a 20% drop from its peak) since the 1800s: declined 38%, required 28 months to hit bottom, and took 60 months (yes, 5 years) to fully recover. In comparison, assuming the March 23rd low of 2,192 in the S&P 500 Index was “the” low, the 2020 bear market dropped 35% and lasted a mere month. We now sit about 17% below the mid-January high. Here is the full history of past bear markets for comparison:

Some other statistics to keep in mind:

- Of the 15 bear markets since 1950, only one did not see the initial major low tested within three months.2

- The U.S. stock market has never bottomed less than six months after falling 30% amid a recession.

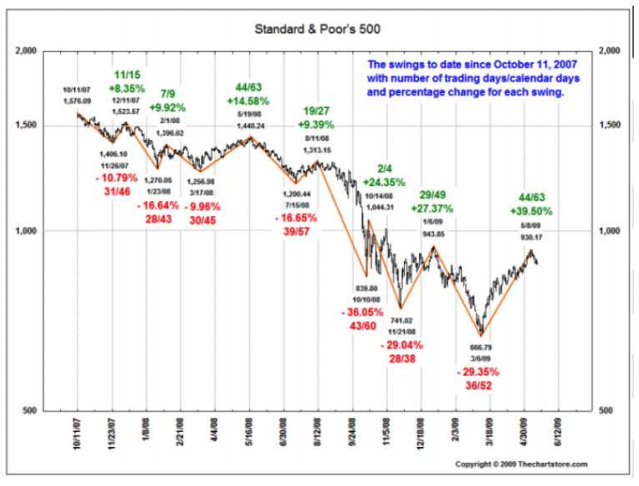

It is common to see meaningful market rallies during what turn out to be ongoing bear markets. During the 2007-09 bear market, there were several hope-filled phases which must have made it seem at the time that the market was on the mend, as you can see on the chart atop the following page. Thus, before even discussing the virus, all this taken together would seem to lend strength to an argument that, despite the recent sharp rally, the stock market isn’t out of the woods yet.

We began this letter by stating that the impact of the virus on financial markets was very sudden. The plunge came as it became clear that the current economic downturn would be both devastatingly deep and broad. The breadth of industries affected by the shutdown is matched by the degree of decimation. Moody’s estimates that nearly a quarter of the economy has been shut since mid-March. Estimates of peak unemployment range up to 30%, which represents a level reminiscent of the Great Depression. During the Great Recession, the mortgage, construction and real estate industries were hardest hit. In contrast, the following is a short list of just some of the areas adversely affected by the response to the virus:

- Restaurants and bars are shuttered, staff unemployed

- Entertainment establishments (theaters, casinos, etc.) shut

- Musicians, performers unemployed

- Retail stores, malls shut, associates unemployed

- Travel industry – airlines grounded, hotels empty

- Oil and gas production halted amid plunging demand

- Medical / dental – anything elective or non-urgent (including medical tourism) canceled

- Film industry (all Hollywood production has stopped; this will be the first time ever we don’t have a Fall TV season)

- Real estate and finance under pressure – more on this later

- Advertising – only beginning to feel the major effects

- Anything else deemed “non-essential”

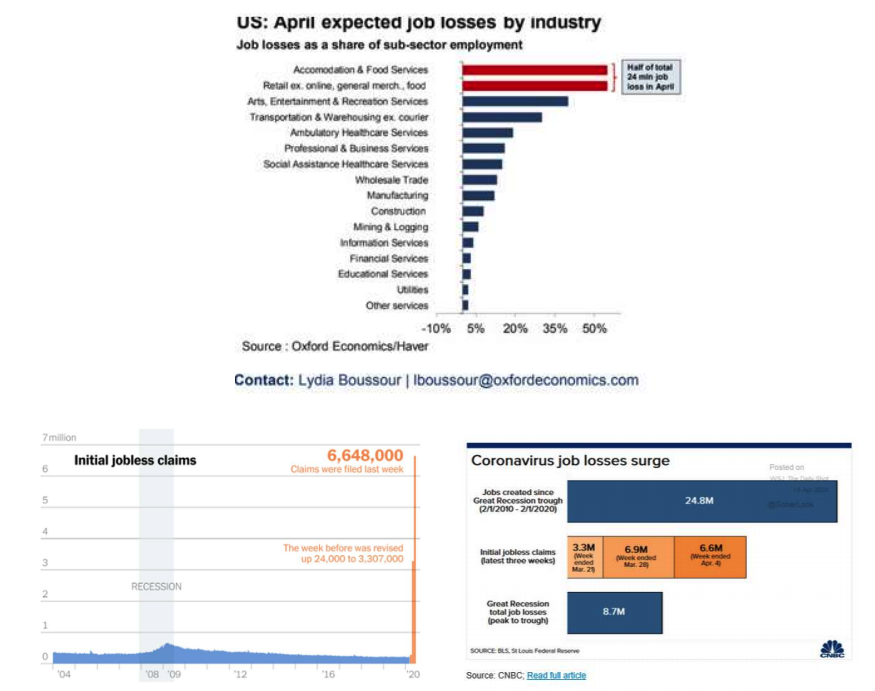

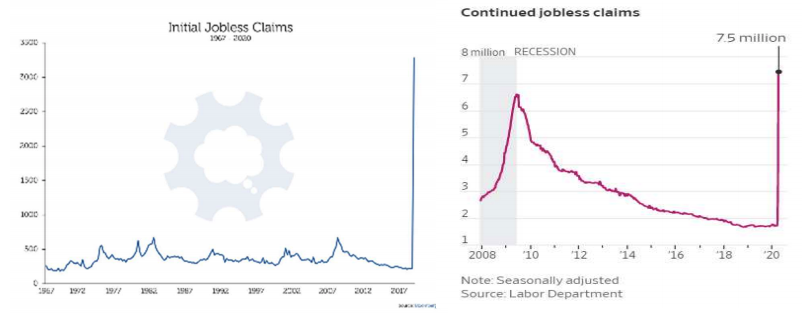

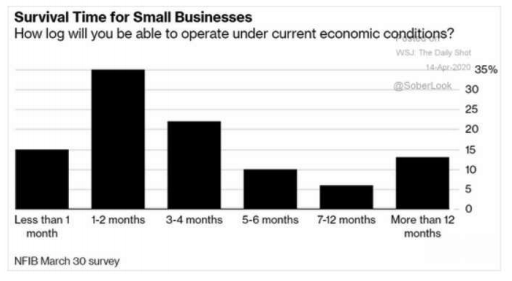

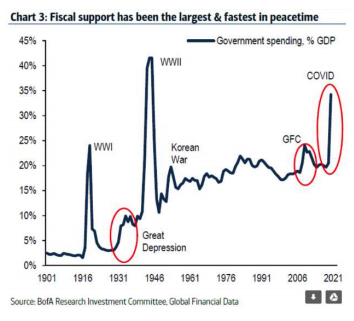

The sort of contraction our economy is facing – that we have imposed upon our economy – is completely without precedent. During the prolonged Great Recession, many workers lost their jobs... eventually. Over the last month, a much greater number of workers lost their jobs... immediately. To choose just one example, nearly every bartender in the country lost their job last month. The graphs on this page illustrate the magnitude of the unemployment wave. 17 million applied for unemployment benefits over the past three weeks3. This will increase much further, as some states, totally overwhelmed by the number of claims, have been unable to even process all of them.

Continuing jobless claims, i.e. the number of people currently receiving unemployment benefits, have already surpassed the total reached during the deep 2008 recession.

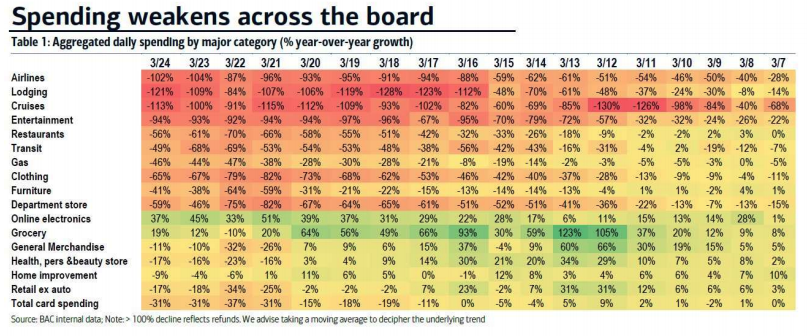

The simplest way to think about the current economic circumstance is to consider the fact that 70% of the U.S. economy is consumption-based. Who among you are out there spending money right now? The below table shows declines in consumer spending each day, across multiple categories through March 24th (before many states were shut down). Note that aggregate total credit card spending (bottom line) was down by 31% in recent days. Some category declines exceeded -100% due to cancelation refunds.

70% of the economy down 30+% equates to a 20+% drop in GDP... before even including weakness in areas beyond consumption. This compares to the 2008 Great Recession, in which real GDP dropped 4.3%, which at the time represented the largest post World War II decline on record. The Great Depression saw GDP drop 30%... over a three plus year period.

Without government intervention (more on that later), our opinion is that we would be headed toward a major financial crisis. Even though that intervention will be massive and ongoing, we may end up with a financial crisis anyway. If people aren’t out there earning money, where will they find the money to pay rent or make their mortgage payment? If homeowners and landlords are not making their mortgage payments, then we have a financial crisis. If small businesses are closed and not making money, and can’t service their loan payments, then we have a financial crisis.

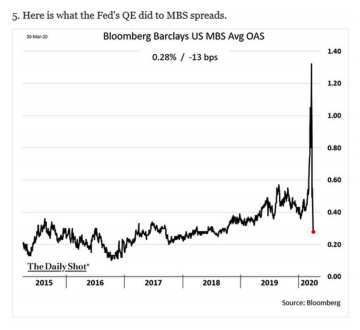

In late March, every financial indicator looked about as bad as it possibly could. Credit, equity, volatility, fund flows, you name it. Then, once the Fed came out with its trillion-dollar-bazooka to restore liquidity, many of those measures rapidly normalized. One example of this is the below chart, which captures the “riskiness” of mortgage backed securities, hugely up and then hugely down. The financial crisis was unfolding, and the Federal Reserve stepped in to quell the flames.

We saw charts similar to the above during the 2008 financial crisis. But, unlike the last downturn, when the crisis happened on Wall Street and slowly made its way out to Main Street, the current crisis is happening across Main Streets and will soon be bubbling back to Wall Street. We know property managers who are collecting half to two thirds of April rent. The numbers are surely far worse for retail properties. How many small business owners planned for a 100% decline in sales? Real estate is often levered because it is such a “safe” asset, but when the rent isn’t paid, can the landlord then make their mortgage payment to their bank? Will the bank then be ok? Not wanting to find out the answers to these questions partially explains the massive government interventions.

In calculating the economic damage equation, the most important variable is the duration of the shutdown. The virus is driving everything right now, so figuring out its progress is the first step in deciphering the economic puzzle. But unfortunately, the question isn’t simply “When will we open back up?” It is instead, “When and how will we open back up? And what will it look like?” Once case counts have receded due to the strict social distancing measures, the virus will still be waiting for us if we simply return to our normal lives.

Trump’s decision on when to open up has often been framed as a choice between the economy and public health, between dollars and lives. Certainly, the economy is important, and the President is right to value it, but we view this either/or characterization as probably a false choice. We, as individuals and collectively as a society, face these dollars/lives trade-offs every day when deciding which safety projects to fund, which charities to endow, and whether and how to sell our own time for money. However, in this case, re-opening without the virus under control would both re-ignite the pestilence and endanger the economy. Without the mitigation measures, deaths could reach into the millions under currently estimated fatality rates, to say nothing of the even higher fatality rates that could hold if the hospital system was overwhelmed. In such a state, people aren’t travelling or going to restaurants; workers aren’t coming to work because they are sick or scared; supply chains are disrupted. We don’t believe there is an option that delivers uninterrupted economic growth, even at a high cost of human lives. We are reminded of what Winston Churchill said about the preWWII British leaders, “You were given the choice between war and dishonor. You chose dishonor, and you shall have war.” Adapted for today, “You were given the choice between plague and recession, you choose plague and you shall face recession.”

In the absence of a breakthrough miracle viral treatment (which is a possibility) the world will not return to normal until we get a vaccine, by all accounts not for 12-18 months4. When we do “open up”, we believe we will largely be in one of three states:

- Effective Suppression: When we reopen, we have strict procedures in place to make sure that there are no uncontrolled outbreaks. This can take the form of continued social distancing, constant temperature checks (with quick isolation for those that fail), contact tracing for those who do get sick, and most importantly, testing, testing, testing, so we know who is safe to return to work and who must be isolated immediately. In this scenario, most of us don’t actually get the virus, and we eventually achieve immunity through a vaccine. Asian countries such as China, and more importantly democratic South Korea, have effectively implemented this strategy, the latter without draconian violations of civil liberties. In South Korea, life is not normal, but the schools are open, the restaurants are open. They serve as an example to be emulated. But this strategy does not offer surefire success. Singapore was attempting to keep the virus suppressed while keeping their economy open but they had a flare up and recently had to close schools and workplaces for a month. Japan might be losing the same battle. Any sign that these Asian countries were unable to maintain their suppression of the virus would be a very worrying sign that this desirable result is untenable.

- Ineffective Suppression: Simply put, when we re-open, the steps we take are not enough to prevent widespread spreading of the virus again. Be it insufficient testing, insufficient adherence to the rules, insufficient organization, manpower, or willpower, the result is subsequent partial or complete shutdowns. The possibility of this scenario illustrates the potential false choice between the economy and public health. An overly hasty re-opening risks a re-shutting. This process could repeat itself until we finally achieve effective suppression or end up in the third scenario below.

- Extended Curve Flattening: In this scenario, we either decided not to pursue effective suppression or we’ve given up on it. Social distancing is recommended but the schools are open and workplaces are open, and people continue to get the virus and suffer consequences. Some shutdowns may be necessary to prevent the hospital system from being overwhelmed, but in general we are resolved to go on with our lives to the extent possible and suffer the consequences. In this scenario, half of us get the virus and then it fades away “naturally”. We fear many poorer countries who don’t have the resources to achieve effective suppression have no choice but to pursue this plan by default. Intentionally pursing this strategy would be to actually choose plague to save the economy (though, as mentioned above, the economy would not be untouched, not by a long shot). The cost in human lives to achieve this goal is unknown at this point. This is because we don’t know how deadly the virus actually is. We don’t know how many people have caught it, because many who do so have mild or no symptoms. It is actually possible that this strategy could prove in retrospect to be desirable if it turns out the virus is much more infectious than we currently believe5. This would actually be great news, because it would mean that many more people have had the virus than we think, the case fatality rate is much lower than we estimate, and the population is much closer to “herd immunity6” than we think. Sweden is actually bucking the trend and choosing to pursue something like this strategy, banking on the virus not being as deadly as many estimate, and that a long shutdown is not sustainable (and ostensibly, that effective suppression post-shutdown would be unattainable). They are leaving much of their society open, attempting to isolate only their older and at-risk populations, leaving the younger and healthier to catch the virus and develop herd immunity. It is a risky strategy and we hope it works, because that would be great news for the world.

Thus, when we can open back up depends on which strategy we decide to pursue. Effective suppression would seem the best outcome but will also need a lot of pieces in place before it can be achieved. And frankly, it doesn’t seem realistic right now. We don’t have the testing capacity. We don’t have the organizational capability to track and trace the inevitable outbreaks, to prevent the brushfires from becoming infernos. The government also seems either to lack the manpower (states) or the willpower (feds). Nevertheless, effective suppression is our base case of what the U.S. will ultimately pursue. We don’t seem to be heading there yet, and we’re not ready yet, but a lot can change in a month.

Our base case expectation is a gradual reopening of the U.S. economy, beginning in mid-May, with an aim toward effective suppression. China’s aggressive shutdown lasted about six weeks (in areas outside of Wuhan). California’s began March 19th. Six weeks from then would be the start of May. Our lockdown was not as extreme and thus we expect it to require a bit longer. Italy, for example, began its shutdown March 9th and has extended it to May 3rd despite its receding virus count. Unfortunately, getting to a low virus count via the current shutdown will be the easy part. Getting the testing capacity and techniques in place for effective suppression will be the hard part. And, we will remind readers one final time, even if we do reopen in this fashion, we still will not be shaking hands or going to concerts. We are unlikely to see a complete return to normalcy in 2020.

Testing is a key component to solving the virus. We have seen it ramp in the U.S, from almost nothing in the early days, to 75,000 per day, but some estimates put the needed capacity at 700,000 a day, a tall order when the rest of the world is trying to ramp up their testing capacity as well. Both antigen (not sick) and antibody (already had the virus) tests are important in allowing the healthy to go back to work. Expect to see “immunity passport” wristbands on the wrists of those already proven to be immune. This is a huge step towards getting life back to normal, because we can trust individuals with “immunity passports” to care for our at-risk loved ones and safely work in other face-to-face situations.

How can we expect that California will begin reopening mid-May even though there appears to be no plan to make that happen? Our forecast relies on developments we cannot see but believe are taking place nonetheless. For the first time in the history of the human experience, the entire world is focused on a single problem. Hundreds of millions of people are laboring in obscurity, working harder than they ever have before, to create something, anything, that will help with this health crisis. We don’t know where the most important breakthroughs will occur, but think it would be unreasonable to expect no progress. Here are some of the most important areas of work:

- Vaccines

- Treatments (medications)

- Treatments (techniques and procedures)

- Virus testing

- Antibody testing

- At-home testing

- Personal Protective Equipment (PPE)- more, better faster

- Better, cheaper ventilators

- Newly built hospital bed and ICU capacity

- Social distancing tools (Zoom) and techniques (curbside take out)

- Contact tracing applications

It would be surprising if there were no major breakthroughs in these important areas. Additionally, millions of people are likely working on projects that we haven’t even thought of, and one of these could prove to be a difference maker.

So, what will it take to do an effective suppression re-opening? The following are the primary pre-requisites to reopen, as outlined by the American Enterprise Institute.

1. Reaching a sustained reduction in cases for at least 14 days

2. Hospitals in the state are safely able to treat all patients without resorting to crisis standards of care

. The state being able to test all people with symptoms

4. The state being able to conduct active monitoring of confirmed cases and their contacts

Cases should peak in California over the next two weeks, meaning a sustained reduction would be seen at the end of April or early May. Hospitals should be increasingly less burdened given expansion of capacity. It is #3 and #4 which will need the push in the weeks to come, with much organization and manpower required.

Re-opening will likely occur in phases. Austria was the first in Europe to begin re-opening this week. The country’s timetable is as follows:

- Small shops, DIY stores and garden centers open April 14

- Businesses deemed slightly higher risk, including hair salons, open May 1

- Restaurants possibly mid-May

- Public events in July

We began this letter discussing all the people out of work, i.e. the first order effects of this crisis. But what about second order effects? When Macy’s furloughed 125,000 employees, Kohl’s 85,000 and Gap 80,000 all on the same day a few weeks ago, those were primary effects. When those employees cancel their cable subscription, it will be a secondary effect. Other second order examples include not wanting to spend nowreduced funds on remodeling the house, banks being scared to make new loans because they have loans in default, states firing workers and delaying projects because their budgets are busted, underfunded pensions exploding because of falling markets and lower interest rates, and retail construction coming to a halt given all the vacancies. Will the government checks and expanded unemployment insurance completely offset all this? Not likely.

We wonder what weaknesses will be exposed that we had no idea even existed. Only when the tide goes out do you discover who is swimming naked. The Financial Crisis exposed General Electric. Who knew they were engaging in all the crazy financial activities that made the entire organization effectively insolvent and required a bailout? Will we find out that say... giant oil companies are much less robust than we thought? Will municipal governments blow up in the ensuing pension crisis?

Some have talked about the economy snapping back because there is nothing “fundamentally wrong” with it and we just need to get past this exogenous shock. We disagree. Consider 9/11, which was an economic shock. Did people get back to work immediately? No, these things take time. Air traffic is down significantly more today than after 9/11. After 9/11, the restaurants and shops didn’t close.

Significant unemployment has never “snapped back” in the past, why should it now? A normal recession has people out of work because they are not in the right jobs. Nothing really prevented unemployed construction workers from becoming coders during the last recession... right? People are unable to work for additional reasons such as being sick or on lockdown right now... but many people will also be in the “wrong” jobs when we emerge. For example, we now have too many restaurant servers and bartenders and not enough, say, ventilator technicians. These problems are not solved overnight. And once we open back up, there will still be too many restaurant servers, because not all the restaurants will reopen. There will be lower demand for restaurant service both due to the depleted finances of customers and lingering fear of public spaces.

We believe the economic disruption from the coronavirus is much greater than that from the 2008 Global Financial Crisis. Fortunately, it is totally possible we could come out of the currently severe downturn more quickly than in 2008 (though not immediately). What is different this time? This time, the government’s response has been much more decisive; it has already been both bigger and faster. The government has been much more willing to act for a few reasons:

- The example of 2008 is fresh in memory and if anything, people think policy makers should have acted more forcefully

- Policy makers are less squeamish about acting, since no one is really “to blame” for the virus. There is not as much hand-wringing about rewarding bad actors this time

- Republicans are less scared about allowing Democrats to go crazy on spending because the Republicans are in charge. Only Nixon could go to China

The massive, rapid stimulus measures currently unfolding take us to where we began this letter: the stock market. Will stocks go up or down? The terrible, unprecedented, economic consequences of the virus and associated shutdown clearly exert a strong downward force on stocks. Announced fiscal stimulus actions ameliorate this downward force somewhat but don’t eliminate it. However, there is a giant, opposing, upward force on stocks: The Fed’s monetary policy in general and money printing specifically.

A thought experiment elucidates the conflict between these forces: imagine a very tight shutdown lasting twelve months. There would be major economic devastation. Now imagine that the Federal Reserve literally prints 320 trillion dollars and gives a million dollars to every man, woman and child in America.7 What happens to stock prices under our thought experiment? We submit they go up, at least in nominal terms. How could they not with all that money sloshing around? When money is given to people, they use it to buy goods and services, and, eventually when that money finds its way into the hands of someone who doesn’t want to buy more goods and services, they buy assets instead. Asset prices increase as a result8,9. The government’s actions do not even need to offset the economic damage from the virus to cause stock prices to go up. They simply need to print enough money10.

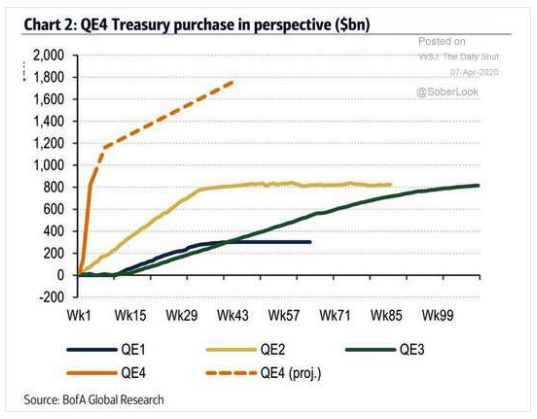

This chart below was created before the Fed last week announced another $2.3 trillion program, now lending directly to cities, states and businesses... which takes the QE4 projection literally off the chart... to $4.1 trillion... and counting. Which force, economic contraction or money printing, will ultimately prove stronger? That is the 64 trillion dollar question.

Sometimes we get feedback that our letters read too much, “on the one hand... and on the other hand...” and need more of a conclusion. While indeed the range of potential investment outcomes has never seemed so wide, we reward readers who have remained with us, by offering our concluding thoughts:

- We estimate the U.S. will begin to re-open May 11th

- The U.S. will not re-open all at once, and will not be the same once it does

- The world is currently experiencing the biggest recession since the Great Depression or perhaps ever

- It seems too soon to say the stock market decline is over

- One should not be too pessimistic about the stock market because the Fed is printing trillions of dollars to buy assets and make loans

- The stock market will bottom well in advance of the economy.11

We thank you for indulging our attempt to make sense of the investment landscape.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 We think it too hasty to call this bear market “over” just because we had a 20% rally. Significant rallies occur in bear markets.

2 That said, the single exception was the 1980-82 bear market, fueled by the Fed dialing back its monetarist policies, which could perhaps be viewed as “the market rallied once the reason for the plunge was removed”. Could the current upward trajectory continue in the same way this time, as the virus is removed? We think this unlikely, but it is a possibility.

3 It is fair to say that for businesses like bars, which had to close, it was natural for them to fire all their workers to enable those workers to at least collect unemployment. If, and it’s a big if, these businesses can reopen quickly, then one might imagine that at least some of these workers could be immediately hired back.

4 This 12-18 month timeline itself is vastly accelerated from the normal five years plus timeline and is not guaranteed.

5 We will know a lot more about this in coming weeks once anti-body testing becomes more widespread. This type of testing will let researchers know what percentage of the population has had the virus, and let individuals know if they have already contracted it and thus presumably have immunity.

6 Herd immunity is the idea that once enough people in a community are immune it becomes very difficult for the virus to spread and thus the entire herd (i.e. community) effectively becomes immune.

7 We don’t think this is realistic or a good idea. In our job as financial analysts it is not our job to think about what the government should do. In fact, thinking about that question can be dangerous, because one can start to confuse the answer to that question with the answer to a much more important question: what will the government do? Like it or not, the government (actually, the Federal Reserve, which is quasi-government) is printing money and will continue to do so.

8 We believe it also matters what is done with the money once it is printed. The effect on asset prices will be much greater if the newly printed money is mostly used to purchase assets as opposed to being handed out to people as in our thought experiment. In the real-world-experiment, now, as in 2008, the money is largely being used to purchase financial assets.

9 In this thought experiment, you might also expect a decent bit of inflation.

10 The downside to this path is the risk of inflation and prolonged financial repression, with interest rates below that rate of inflation.

11 This is always the case. Markets look forward.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All