When markets get as volatile as they’ve been lately, it’s extremely difficult for investors to avoid our innate “fight or flight” response. In our states of heightened emotion (fear) our logical minds try to tell us that we are witnessing an incredible buying opportunity for long-term oriented investors. However, our emotions make it very difficult to pull the trigger. Moreover, with markets as uncertain as they’ve been lately, there is no way for us to know whether the worst is over or not.

On the other hand, it behooves us to remember that picking the exact top or bottom is only possible by chance. Therefore, to me at least, it’s always been easier to recognize attractive values when they manifest and accept that as more than good enough. As a result, my basic strategy is that when I can identify attractive value, especially in extremely high-quality companies, I am willing to invest regardless of whether they fall a little further, or even a lot, or not.

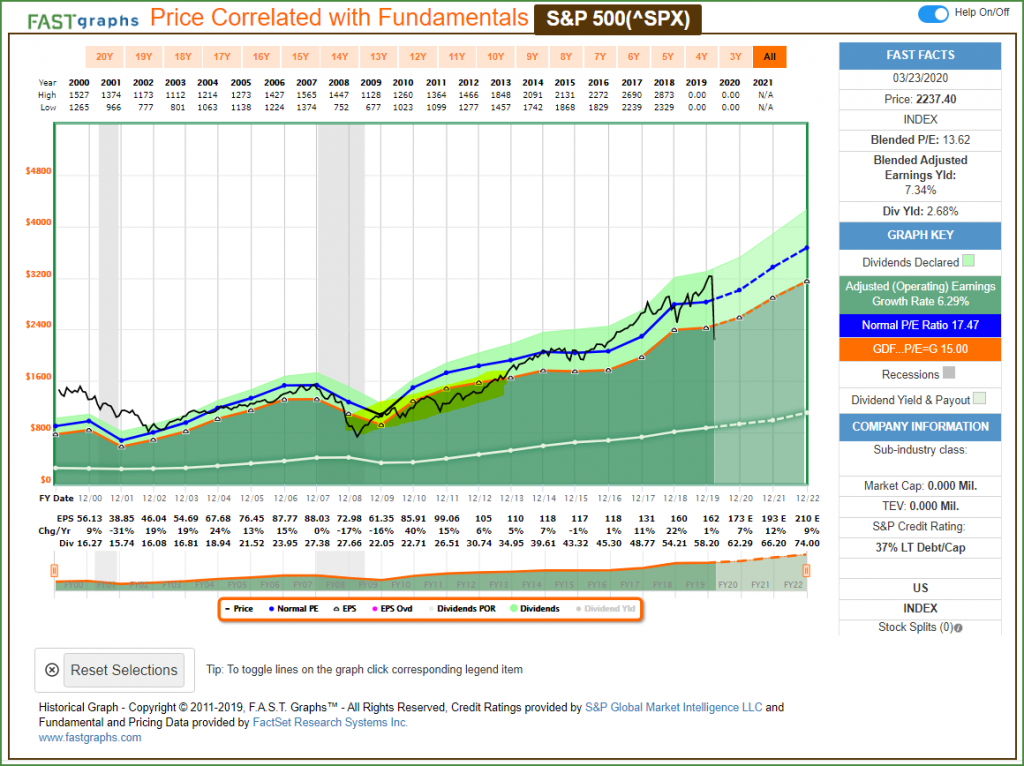

Moreover, I also find it easier to be courageous when I can identify extremely high-quality companies at attractive valuations. This is important, and a strong contrast to what we experience when the markets brought us a similar opportunity during the great recession of 2008 and 2009. I would like to remind investors that there was a 4 ½ year period starting in March 2009 which ended in October 2013 when stocks making up the S&P 500 were very attractive. I have highlighted in yellow that timeframe on the earnings and price correlated FAST Graph of the S&P 500 below:

On the other hand, I want to also point out that the years 2014 until just recently in 2020 the S&P 500 was trading at a high valuation relative to fundamentals and historical norms. As a card-carrying diehard value investor, I for one found it very difficult to find attractively valued stocks over that period. On the other hand, it was not impossible because, as I’ve often stated, it is a market of stocks.

Moreover, I was even more frustrated because the highest quality bluest of blue chips were the stocks that the market was valuing the highest. As a result, it became much more difficult to find attractive investments of impeccable quality because the crème de la crème stocks were mostly overvalued. In short, as a value investor, I find bull markets troubling albeit very profitable. In contrast, I tend to be very comfortable in bear markets simply because I see value everywhere I look.

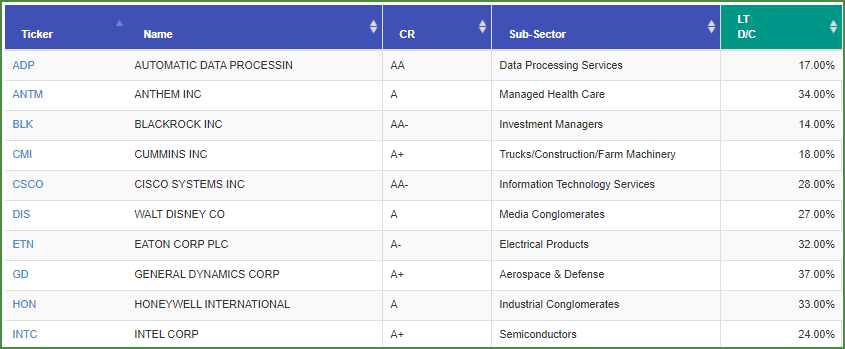

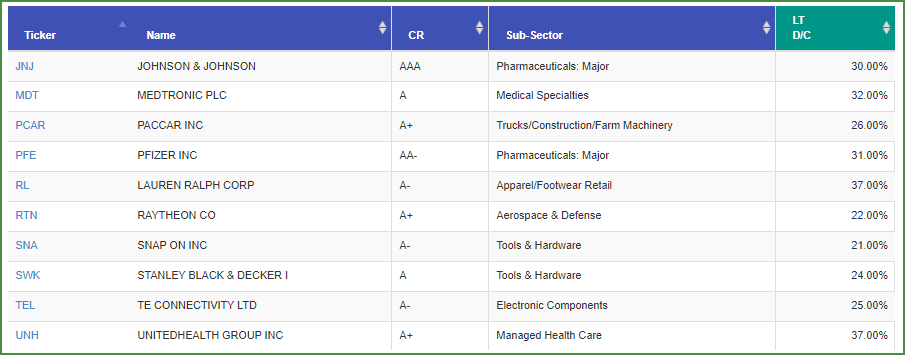

20 A Rated Low Debt Blue Chips to Consider

The following 20 companies I would rate amongst the highest quality blue-chip dividend growth stocks in the market. Thanks to the recent market crash, most high-quality dividend growth stocks once overvalued, have now become attractive. As a result, the criteria for my selection process was simple and straightforward. Since I now had value, I turned my focus to high-quality. Therefore, I searched for companies with consistent long-term records of increasing their dividends with credit ratings A rated or better and long-term debt to capital ratios below 40%.

The following 20 companies are high-quality blue-chip dividend growth stocks with well protected dividends that have currently gone on sale. No one can predict whether the market has yet bottomed, but as it relates to these 20 blue chips, I suggest it really doesn’t matter. These companies are of impeccable quality and I would argue that at their current valuations each represents a very attractive long-term opportunity. In other words, when I can identify this kind of quality at these kinds of values, I don’t try to second-guess. Instead, I would be willing to confidently invest in any of the following 20 based on quality and value. Of course, that assumes a long-term view.

Top 20 Review Credit Ratings and Long-Term Debt to Capital

The following review is presented in alphabetical order and focuses on the credit rating, the subsector and each company’s long-term debt to capital. When screening to come up with this list, I was looking at credit ratings and debt levels.

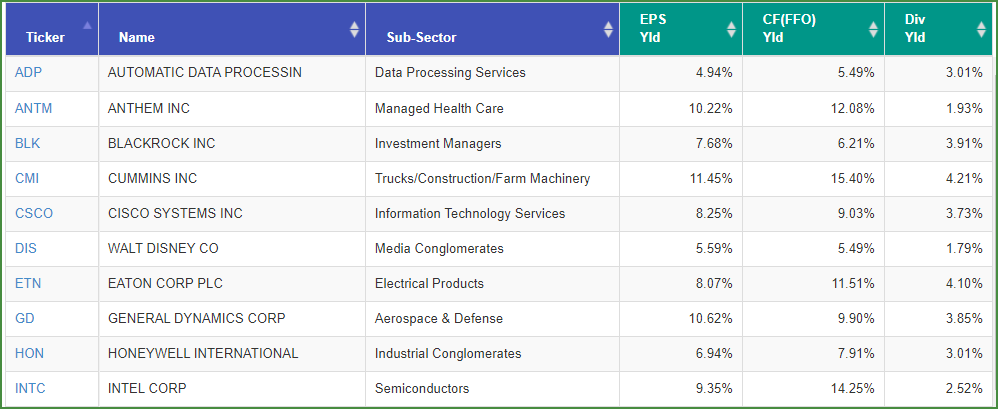

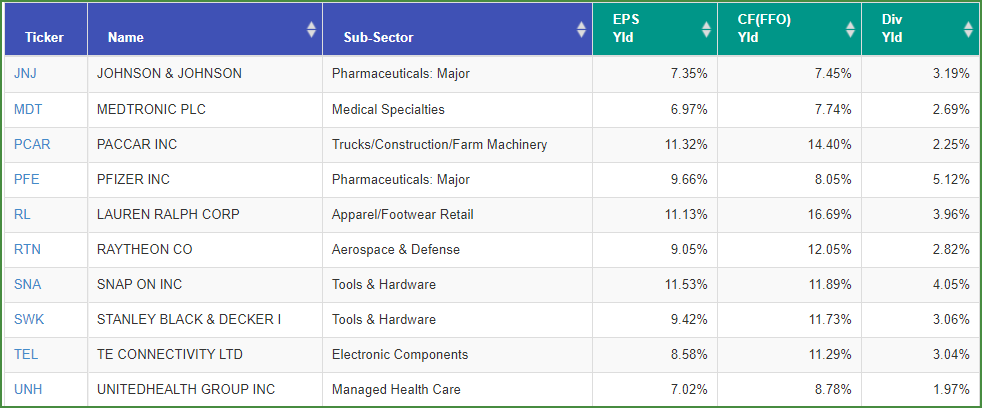

Top 20 Review Earnings Yield, Cash Flow Yield and Dividend Yield

With my quality standards met and established, I then turned my attention to valuation. As regular readers of mine know, I prefer earnings yields of at least 6 ½% or better. Although I held this group to those standards, I did give a pass to Automatic Data Processing and Walt Disney Company because of their quality and popularity. However, from a risk-adjusted long-term rate of return investment point of view, these would be my least favorites.

FAST Graphs Analyze out Loud Video: Quality, Value but Different

I believe all the companies on the above research list are high-quality dividend growth stocks currently available at very attractive valuations. They are all A rated or better and they all have debt to capital levels below 40%. However, even though they share these same characteristics, each company is different and should be judged on its own merit and potential. Therefore, with the video I offer 5 stocks from the above list in order to more clearly illustrate the differences.

FAST Graphs Analyze Out Loud Reviewing Automatic Data Processing (ADP), Walt Disney (DIS), PACCAR Inc (PCAR), Raytheon (RTN) and Snap On (SNA):

Summary and Conclusions

The volatility we are experiencing in the market is both unnerving and exciting. In just the last few weeks, we have seen record days of stocks plummeting and we have also seen record-setting up days. One of my objectives with this article was to put the recent volatility into a clear perspective. As I indicated with my earnings and price correlated graph of the S&P 500, the overall market had become fully valued to overvalued. As a result of the recent correction, the valuation of the overall market now appears much saner.

On the other hand, it is a market of stocks and there still are stocks that are significantly overvalued despite what has recently occurred. Of course, the recent market has also brought us terrific bargains. For the first time in years, I do believe that we are now in a buyer’s market. That doesn’t necessarily mean we should be buying today, but I do believe it means that many stocks have become inexpensive. In the long run, being able to invest in high-quality companies at attractive valuations is a dream market for prudent value-oriented investors. Living the dream.

Disclosure: No position

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.