Want to read more by Ashmore Group? Visit their Featured Firm page here

The VIX index has spiked. Over more than twenty years, VIX spikes have been excellent guides to when to put money to work in EM fixed income and equities. Investors have, on average, generated 262bps of excess return in EM fixed income and 234bps of excess return in EM equities by putting money to work during VIX spikes relative to a ‘timing agnostic’ investment strategy.

This time the trigger of the VIX spike was coronavirus. We discuss how we see the outbreak impacting global growth as well as EM economies compared to developed countries.

VIX spikes

The Chicago Board Options Exchange Volatility Index, or the ‘VIX index’ as it is affectionately known in investment circles, just spiked to 42 from 19 in January. Spikes in the VIX index of this magnitude have historically been excellent guides for when to put money to work in EM. We strongly suspect that the same will be the case now. VIX spikes tend to be good entry points for EM because they tend to trigger wholesale and indiscriminate liquidations of EM assets for the sole reason that they are, in the minds of many investors, “risky” assets. Fundamentals almost never deteriorate commensurately, so value is created.

This latest VIX spike has been triggered by coronavirus. The outbreak originated in China, but is now spreading beyond China. This is happening against the backdrop of a US business cycle, which is very long in the tooth and extremely rich valuations in the US stock market. Past triggers of VIX spikes have included anything from the sub-prime crisis through Lehman and the Japanese tsunami. Figure 1 lists the VIX spikes dating back to 1994. Note that the last time EM specific events caused major VIX spikes were in 1997 and 1998. Since then, every single VIX spikes has either been an ‘act of god’ or caused by incidents in developed economies.

VIX spikes have proven to be an extremely useful guide for when to put money to work in EM. Investing in months with VIX spikes has typically made money relative to a ‘timing agnostic’ investment approach. Figure 2 quantifies the excess return associated with timing entries to the EM asset classes to coincide with VIX spikes. ‘Active’ return refers to the average 12 month return after VIX spikes, while ‘passive’ return refers to the average annualised return since index inception. ‘Alpha’ is the difference between the two. The average alpha from putting money to work during VIX spikes is 262bps for fixed income and 234bps for equities. The table also shows how long the indices have existed (‘years’).

Coronavirus

Truth is said to be the first casualty of war. Similarly, a sense of proportion can be said to be the first casualty of pandemics.1 The coronavirus is currently being priced into markets, but rather spectacularly so and possibly excessively so, too. Hyperbole is not uncommon in financial markets, particularly in EM. Investors tend to create fuel for their own panics, invariably pushing prices far beyond what is reasonable in relation to fundamentals. Since prices can be an extremely bad guides to reality during bouts of risk aversion, it is useful as such times to look at some facts to inject a bit of reason.

To the extent that coronavirus is anything like flu, the spread of the illness is likely to be highly sensitive to temperature and humidity. Specifically, higher temperatures and higher humidity – and particularly the combination of both – slow influenza’s spread. At very high humidity levels the virus even stops spreading completely.2 The reason is that warmer air tends to hold more moisture. Moist air prevents airborne viruses from traveling as far as they would in dry air. Similarly, the small droplets expelled in coughs or sneezes gather more moisture in humid conditions to the point, where they become too heavy to stay airborne.

Suppose, for argument’s sake, that coronavirus spreads to all countries and that the final penetration rate in each country in the final equation boils down to temperature and humidity. In that case, the patterns of past flu outbreaks may turn out to be a good guide to the impact of the current outbreak. So far in this year’s northern hemisphere winter, the percentage of specimens testing positive for flu (as of 14 February 2020) is in excess of 30% for Europe and North America and Middle East, 20%-30% for Northern Asia and North Africa, but below 20% for Latin America and Africa, according to the World Health Organisation (WHO).3 Longer-term data from 2011/12 through 2018/219, shows that the average percentage of positive flu specimens have been 50-60% for North America and Europe, 35-40% for Asia and 15% to 35% in Latin America.4 There is no long-term data available for all countries, but the percentages mentioned here are consistent with the hypothesis that penetration rates are lower in EM countries, mainly due to temperature and humidity.

Suppose, again for argument’s sake, that the damage to economic growth in each region of the world is somehow proportional to the percentage of positive specimens as recorded by WHO. Based on this hypothesis, it is possible to form an estimate of how global growth will be impacted. Figure 3 shows how a simple simulation using infection-adjusted growth rates impacts global growth rates. Global growth could slow by a just over one third from 3.4% to 2.2% in 2020 on this basis. While the impact in 2020 is considerable by 2021 the impact is significantly diluted. Note that this does not take into account any policy reaction, which could result in an even sharper rebound. By 2024 the impact is practically imperceptible.

Within this overall growth picture, there are important changes to the contribution to growth from EM countries and developed countries. These are illustrated in Figure 4. The first column of numbers summarises the contributions of different regions of the world to global GDP growth using data from the October 2019 World Economic Outlook from the International Monetary Fund (IMF), that is, before the coronavirus outbreak. This data shows that EM countries would have contributed some 80% of global growth prior to the onset of coronavirus, while developed countries would have contributed the balance of 20%.5 The second column of numbers shows how these growth contributions change if growth rates are adjusted according to the infection rates from WHO (shown in the far right column of Figure 4). The main finding is that the contribution of EM economies to global growth increases to 85% from 80%, while developed economies will contribute 5% less to global growth, bringing their contribution from 20% to just 15%. Within EM, the only region to contribute less to global growth is Eastern Europe on account of higher infection rates. All other EM regions contribute marginally more to global growth overall.

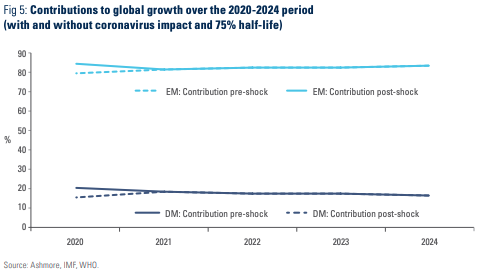

Clearly, the duration of the outbreak is important. China is probably a good guide, assuming that other countries handle the outbreak as efficiently as China, but remains to be seen. Still, we strongly believe that coronavirus is a temporary dislocation. As such, the outbreak will fade and ultimately disappear completely. Moreover, we believe that coronavirus is likely to have a relatively high half-life, consistent with past flu-like infections. The exact half-life of the outbreak is still in the realm of ‘guesstimates’, but the gradual subsidence of infection rates in China supports the view that the half-life is high. Based on this observation, Figure 5 shows how the outbreak may impact global growth rates over a five year period with a half-life of 75%. In this scenario, three quarters of the distortions to global growth contributions from EM and developed countries have dissipated within just a year and thereafter there will be almost no discernible impact on global growth contributions. By 2024, developed economies will contribute 16% of global growth and EM economies will contribute 84%, which is virtually identical to a no-coronavirus scenario.

Discussion

Global markets reacted violently to coronavirus outbreak in China, but the reaction has been more violent in response to signs that the coronavirus is spreading outside of China. The number of cases in China appears to be stabilising. The lesson from China is that the illness is transitory. A sharp slowdown in GDP growth is rapidly being priced into gold, US treasuries and oil and increasingly in credit spreads and developed markets equities, although, in the case of US equities, the extreme valuations could usher in a greater correction. This is particularly the case if the coronavirus triggers the long-overdue recession in the US.

The thing to watch now is the policy response. China moved fast to contain the disease and reacted pro-actively to the yet to be seen economic downturn with decisive monetary and fiscal stimulus, thus backstopping both the A-share market and credit spreads within China.

The US has room to cut rates, but not enough room to pull the US economy out of recession. The Fed has so far shown little willingness to cut, but that may soon change. Europe and Japan may be pushed into fiscal stimulus, since they have little room left to ease monetary policy. The risks posed by the lack of stimulus options in developed countries have been obvious for some time, albeit broadly ignored.6

The analysis of the coronavirus as presented here is based on a number of assumptions, which may or may not prove correct. Perhaps the most important assumption is that GDP growth rates are somehow going to be impacted in proportion to infection rates. Still, if coronavirus is anything like flu then EM should end up considerably less impacted than developed countries due to environmental conditions. Moreover, the impact on global growth, although sharp, should prove transitory due to the typical high half-life for flu outbreaks. Granted, even transitory growth shocks create negative economic shocks, particularly for commodity exporters, but since the shocks are temporary the optimal policy response for such economies is to borrow to smooth economic activity during the downturn. As for non-net commodity exporting EM countries – which now make up two thirds of EM countries – they will experience a de facto transitory real income windfall in the form of lower import prices, which should be supportive for bonds.

Conclusion

Our view is that investors should take a ‘chill pill’ as they consider their response to coronavirus.

Hot headed investors will undoubtedly feel inclined to liquidate, but this would be a mistake, because they will crystalise losses that are bound to be reversed in relatively short order. This is the main conclusion to the VIX spike analysis presented at the start of this paper.

More rational investors are waiting for signs that the panic is subsiding. This is a far more sensible strategy, but it runs the risk that the market suddenly rallies before they have had an opportunity to buy. The most experienced and far-sighted investors are already nibbling with the intention of continuing to do so during the duration of the pandemic. This strategy has the merit of extracting the maximum benefit from the current dislocations. It locks in a high yield and the potential to reap juicy capital gains as the pandemic subsides and prices normalise.

As always, the first casualty of pandemics may well be EM, but EM is also likely to be the greatest winner for those who buy.