Want to read more by Guggenheim Investments? Visit their Featured Firm page here

If I had written a commentary on how 4,000 people dying from the flu would topple global financial markets, I think I would have been deemed insane. Yet today that is exactly the story.

After all, the World Health Organization estimates that influenza kills 290,000 to 650,000 people per year. How does this statistically small number of 4,000 versus a global population of 7 billion bring the market to its knees? I don't think I have to explain that right now, but if anyone thinks I need to, feel free to reach out to me in a socially distant fashion once you have washed your hands for 20 seconds and then rinsed them in Purell.

Amazingly, the market is finally waking up to the prospects of not just viral contagion but also to financial contagion. The phenomenon of a relatively insignificant event cascading through an unpredictable series of circumstances resulting in a severe outcome has been referred to as the "butterfly effect."

The concept is derived from how a seemingly insignificant phenomenon like a butterfly flapping its wings in Brazil leads to a hurricane on the other side of the globe.

Who could predict the exact chain of events set off by the coronavirus that leads us to the circumstances that we face today? Besides the public health and economic crisis, would anyone have considered that this would also turn into a geopolitical crisis? Russia is attempting to use this critical moment to its own advantage, and the collapse of the Russian-OPEC alliance—precipitated by Russia’s goal of killing off the U.S. shale industry—has turned into an all-out price war that is causing chaos in the energy markets.

Now the financial contagion is spreading rapidly into the credit markets where not only energy bonds are plunging but other sectors like airlines, lodging, and retail are sure to follow suit.

Then there is the knock-on effect to corporate earnings and cash flows across a broad swath of industries once the world enters a global recession which now appears to be inevitable.

We arrive at this moment with the overleveraged corporate sector about to face the prospect that new-issue bond markets may seize up, as they did last week, and that even seemingly sound companies will find credit expensive or difficult to obtain.

The prospect of a crisis at maturity—that a borrower with maturing debt finds it impossible to roll the debt over to pay it off—is a very real prospect even for companies that are solvent. It has happened before, and it will happen again.

All of this points to the fact that it is virtually impossible to identify the next domino to fall but one thing seems certain: They will continue to fall.

How did we get into such a precarious position? After a decade of profligate borrowing by corporations, it would seem that any reasonable investor would have realized the fragility of the financial system.

Rumors are circulating in the market hoping for a return of crisis era programs like TAF, TARP, TALF, TLGP, and TSLF. (Can anyone remember what all these alphabet programs stand for?) But resurrection of these programs may arrive in time for Easter.

For now, stocks are limit down, the entire yield curve for Treasury securities yields under 1 percent and credit spreads are exploding, especially in energy bonds.

What next? I hate to admit this, but our proprietary models indicate that fair value on the 10-year Treasury note will reach -50 basis points before year end and the possibility that rates could overshoot to -2 percent.

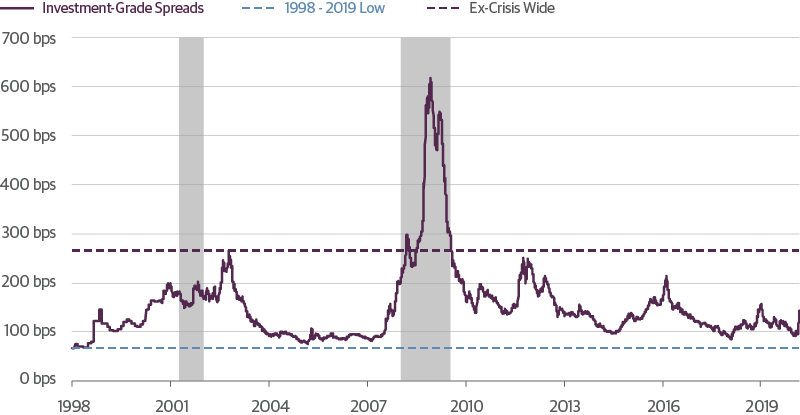

Credit spreads have a long way to expand. BBB bonds could easily reach a spread of 400 basis points over Treasurys while high yield would follow suit with BB bonds at 750 basis points over and single B bonds at 1100 basis points over. The risk is that it could be worse.

High-Yield Bond Spreads Have a Long Way to Expand

Source: Guggenheim Investments, Bloomberg. Data as of 03.06.2020.

And don't forget that a large number of investment grade bonds already have leverage ratios equivalent to high yield. As the market learned in the case of Kraft Heinz (KHC) last month, rating agency forbearance may soon dissipate, especially as earnings and free cash flow declines. KHC, a well-known household brand with a market cap of over $30 billion, saw its corporate bond rating slashed from BBB- to BB+ by both S&P and Fitch in one day. The downgrade made 19 KHC bonds totaling $22 billion in total outstanding ineligible for the most broadly-followed investment-grade corporate bond index benchmarks.

Investment-Grade Bond Spreads Are Poised to Widen

Source: Guggenheim Investments, Bloomberg. Data as of 03.06.2020.

And don't forget that a large number of investment grade bonds already have leverage ratios equivalent to high yield. As the market learned in the case of Kraft Heinz (KHC) last month, rating agency forbearance may soon dissipate, especially as earnings and free cash flow declines. KHC, a well-known household brand with a market cap of over $30 billion, saw its corporate bond rating slashed from BBB- to BB+ by both S&P and Fitch in one day. The downgrade made 19 KHC bonds totaling $22 billion in total outstanding ineligible for the most broadly-followed investment-grade corporate bond index benchmarks.

Our estimate is that there is potentially as much as a trillion dollars of high-grade bonds heading to junk. That supply would swamp the high yield market as it would double the size of the below investment grade bond market. That alone would widen spreads even without the effect of increasing defaults.

As for stocks, technical analysis suggests that there should be support around 2600 on the S&P 500, but in a recession scenario a level closer to 2000 could be the ultimate outcome.

Many skeptics have challenged this idea, saying that the panic is close to an end. In this circumstance I recall the quote from Winston Churchill: "This is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning."

Important Notices and Disclosures

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

One basis point is equal to 0.01 percent.

Investing involves risk, including the possible loss of principal. Investments in fixed-income instruments are subject to the possibility that interest rates could rise, causing their values to decline. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

©2020, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.