While it is hard to predict the economic impact from the coronavirus (COVID-19) in the first quarter given little yet reported and many unknowns, most economists are anticipating a rebound later this year.

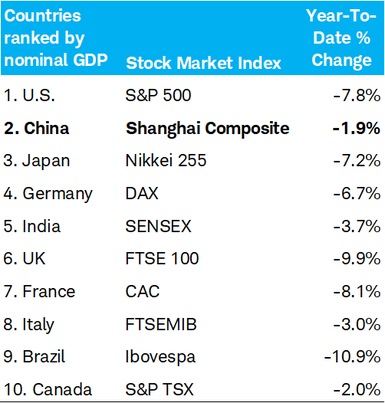

Two of the best performing stock markets in the world so far this year are China and Italy, where COVID-19 outbreaks have been focused—reminding us that headlines don’t often make for good investment advice.

Rather than trying to call the bottom, a more effective way to think about investing right now is to focus more on the duration rather than the decline. Markets may have further to fall, but they may not stay down for the rest of the year barring a severe pandemic.

Q: What’s the economic impact of COVID-19?

While it is hard to predict the economic impact in the first quarter given little data yet reported and many unknowns, most economists are anticipating a rebound later this year. They see the drag on growth early in the year resulting in only a modestly weaker pace of growth for the year as a whole. For example, on February 22, the International Monetary Fund (IMF) updated their 2020 global growth outlook, lowering the pace of growth by 0.1% due to the anticipated impact of COVID-19, putting their estimate of GDP growth at 3.2% compared with 2.9% last year.

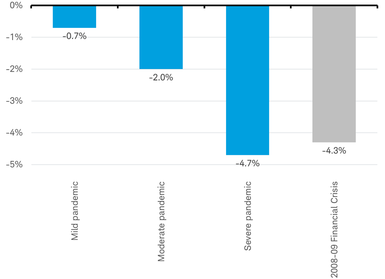

With the situation evolving rapidly, how bad could it get in the event of a pandemic? In 2008, an internal report by the World Bank estimated the impact of a “mild” flu pandemic at 0.7% of global GDP, a “moderate” pandemic at 2% and a “severe” outbreak at 4.8%. That would be the difference between a slowdown, a downturn, and a global recession as deep as the GDP decline during the financial crisis of 2008-09.

In the event of a pandemic: mild, moderate and severe potential global GDP impact

Source: Charles Schwab, Federal Reserve and World Bank data as of 2/27/2020.

Some good news is that the global economy was improving ahead of the coronavirus outbreak even as recently as mid-February. For example, echoing last week’s better-than-expected IFO business confidence report for Germany, yesterday’s Italian business confidence survey for February showed unexpected improvement. While these results are out of date since the survey period preceded the jump in coronavirus cases in Italy by a week, it offers further evidence that core European countries were seeing improving economic momentum just ahead of the rise in new cases.

Q: What economic stimulus is being applied, where, and will it work?

The seemingly daily announcements of new outbreaks and quarantines have been met lately by government announcements of new economic stimulus to combat the economic effects of the COVID-19:

Hong Kong announced stimulus equivalent to 4% of GDP in the form of giving 10,000 Hong Kong dollars to all residents 18 or older.

The German finance minister announced plans to suspend the debt brake provision in the German constitution to allow higher deficit spending.

China has unveiled a host of measures from cutting rates to boosting infrastructure financing and support for small and medium-sized businesses.

Taiwan has approved a $2 billion stimulus package that includes tax cuts for travel related businesses.

The market is expecting the world’s major central banks to cut interest rates, including the Federal Reserve as soon as next month.

While this stimulus may help to support some demand, much of it is unlikely to show up where spending has been cut the most, travel and entertainment, given the fears of contagion. And it is unlikely to have any impact on restoring supply from closed factories. As a result, economic stimulus may be less effective in addressing the drag from COVID-19 than the factors related to a typical economic downturn.

Q: What is the earnings impact?

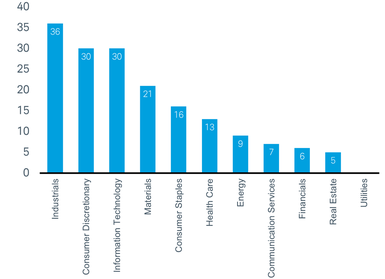

Since January 20, 530 companies have mentioned COVID-19 in their communications to investors. More specifically, nearly 200 companies revised their earnings guidance lower in response to COVID-19. Those revisions were more prevalent in the Industrials, Consumer Discretionary and Information Technology sectors, as you can see in the chart below.

Number of MSCI World Index companies lowering earnings guidance due to COVID-19 since January 20

Source: Charles Schwab, Factset data systems data as of 2/27/2020.

The long-awaited earnings recovery expected by analysts for the first quarter is now likely to be delayed. Overall, Wall Street analysts have not made much of a cut to their corporate earnings forecasts for the year, anticipating a second half double-digit rebound. Those estimates are at risk if the outbreak results in a prolonged negative impact on supply and demand for businesses.

Q: What are stock markets pricing in?

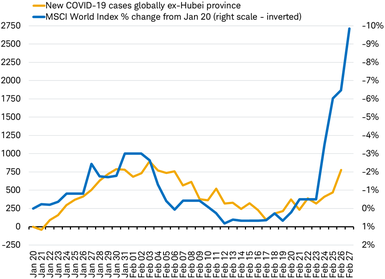

One way to look at what the stock market is anticipating is to compare it to the spread of COVID-19. Based solely on the trends in new case growth and stock market moves, the stock market may be pricing in the risk of a surge in daily new cases triple that of the late January peak, as you can see in the chart below.

Stocks: new virus cases to triple?

Source: Charles Schwab, Bloomberg data as of 2/27/2020. Past performance does not guarantee future results.

Perhaps the most surprising development in the stock market is that two of the best performing stock markets in the world so far this year are China and Italy, where COVID-19 outbreaks have been focused—reminding us that headlines don’t often make for good investment advice.

China is the best performing stock market this year

Source: Charles Schwab, Bloomberg data as of 2/27/2020. Past performance is no guarantee of future results.

Q: Will stocks fall another 10%?

No one knows for sure. The market became more vulnerable to a pullback after a strong run up last year and as investors became more optimistic in 2020 despite growth slowing and earnings stalling. And even now, stocks have retraced only a portion of last year’s gains.

Rather than trying to call the bottom, a more effective way to think about investing right now is to focus more on the duration rather than the depth of the decline. Markets may have further to fall, but they may not stay down for the rest of the year barring a severe pandemic. The last major bear market began in October 2007 and didn’t bottom for two and a half years as major imbalances had to be corrected. Today, the global economy faces fewer such imbalances. A short duration drop by nearly any amount is easier on long-term investors than one that lasts for years.

Q: What should investors do?

Over the past 12 months, markets have experienced both large gains and sharp reversals, which may have knocked portfolio allocations off course. Rebalancing back to long-term targets may be appropriate. Now would be an optimal time to develop a plan, or revisit it if it’s been a while since the last review.

To take a strong investing position, one way or another, it takes strong conviction in answers to key questions. Questions we are seeking answers to include:

What is the impact on China’s economy? The first credible data point won’t be available until we get the February purchasing managers’ index report on Feb. 29. But that is just one survey, it won’t be until March 16 that we get the industrial output, fixed asset investment and retail sales data to give us first take on the COVID-19 impact.

How quickly is the supply shock easing as production returns in China? Chinese officials have announced that at least 50% of major industrial firms are back to work and cited even higher percentages in key inputs like metals (80%). There is some evidence such as rising air pollution levels, and shipping traffic to suggest this may be the case. But the pace that China restores the remaining operations is critical to assessing the global supply chain impact. Additionally, while supply chain disruptions in China may be easing, disruptions in supply in countries outside of China could form.

What will be the response to outbreaks in other countries? China had an authoritative response to containing the spread of the virus, other countries may be less willing or able to quarantine large regions or shutdown businesses. World Bank research shows that 60% of the economic impact comes from cutbacks in travel and entertainment with much of the rest tied to other efforts to avoid infection. Rather than being made by one party as in China, those decisions may be made by thousands of businesses and millions of households around the world which are hard to predict.

We look forward to sharing the answers we gather to these questions to enable informed investment decisions.