Regular readers of this blog and of our other commentary know that we have been been looking for some kind of cyclical rebound in economic activity starting in the first quarter of 2020. By many indications, we are getting just that, and right on time. One of the most useful indicators we use to judge cyclical turning points in economic activity is the ISM Manufacturing PMI. We like it because the manufacturing sector is among the most cyclical areas of the economy, and thus the manufacturing PMI is highly sensitive to changes in overall activity.

From the end last year through January, the ISM Manufacturing PMI has moved from a reading of below 50 (contraction) to above 50 again (expansion). This is definitely good news. What’s more, the delayed effect of the lower cost of money we’ve experienced since the end of 2018 (i.e. the lowering of long-term interest rates), suggests this cyclical recovery has more than a year left to run. The chart below demonstrates this observation. In it, I plot the changes in the 10-year Treasury yield advanced by 18 months (red line on the right, inverted scale) on top of the ISM Manufacturing PMI (blue line on the left scale). In this chart we can clearly see that manufacturing activity began to turn higher literally on the month suggested by changes in long-term bond yields.

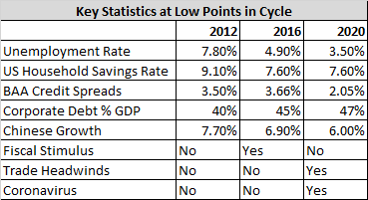

But, here’s one of the problems I have with the idea of a full-blown 2016-’18 or 2012-’15 style economic expansion that would carry stocks up another 50-70% from here. There is simply isn’t as much gas in the tank now as we had back in either 2012 or 2016. Side note, US stocks rallied 76% from the 2011 lows through the middle of 2015. They rallied 57% from the lows in 2016 through the middle of 2018.

For example, at the economic lows of 2012 and 2016 the US consumer activity had much more room to improve. Back in 2012 the unemployment rate was a whopping 7.8% and the household savings rate was a robust 9.1%. The higher the savings rate, the more “dry powder” the consumer has to make purchases by running down the savings rate. In 2016 the unemployment rate was still well above previous cycle lows at 4.9% and the savings rate had come down to 7.6%. Now, the unemployment rate is at multi-generational lows of 3.5%. The savings rate is still a healthy 7.6%, but this metric has little hope of moving higher since slack in the labor market has been reduced by such a large extent.

But it’s not just the household sector that has less room to improve from here, it’s also the corporate sector. Currently, the extra margin investment grade corporate bond issuers must pay over and above the treasury yield is at a low level of 2.05%. In 2012 these corporate credit spreads were 3.5% and in 2016 they were 3.66%. In both of those cases, credit spreads – a proxy for corporate funding costs – could come down by quite a lot before entering the historically low realm. Not so today. Of course, credit spreads could theoretically move lower than they are now, but they are currently sitting at the second lowest level since 2007. Even if they did move lower, it wouldn’t likely be by that much. Back in early 2018 investment grade credit spreads got down to 1.6%, so even a best case scenario provides only 0.45% of credit spread improvement from current levels. For what it’s worth, credit spreads narrowed by 1.5% from 2011-2014 and by 2% from 2016-2018.