“When you make a choice and say, 'Come hell or high water, I am going to be this', then you should not be surprised when you are that. It should not be something that is intoxicating or out of character because you have seen this moment for so long that ... when that moment comes, of course it is here because it has been here the whole time, because it has been [in your mind] the whole time.”

“When you make a choice and say, 'Come hell or high water, I am going to be this', then you should not be surprised when you are that. It should not be something that is intoxicating or out of character because you have seen this moment for so long that ... when that moment comes, of course it is here because it has been here the whole time, because it has been [in your mind] the whole time.”

Kobe Bryant, 1978 – 2020, 5-Time NBA Champion, 18-Time All Star, Winner of Two Gold Medals, Academy Award Winner, Author, Businessman, Father and Coach

The year 2019 was the complete opposite of 2018 across investment markets. Across the board nearly every asset class around the world, from bonds to stocks to gold to real estate, was down in 2018. 2019, on the other hand, delivered above average gains across those same asset classes. 2018 ended with a sharp 20% selloff in U.S. equities. 2019 ended with market darlings, such as Tesla (which we don’t own), and Apple (which we do), shooting seemingly straight up.

The market zeitgeist is perhaps best captured by CNN’s Fear and Greed Index. The new year’s measure was all greed at 97, the highest rating we can recall, whereas a year ago it was all fear at 12. Such an observation calls to mind Warren Buffett’s famous admonition to, “be fearful when others are greedy.”

Why was 2019 so much better than 2018 for the markets? Two main reasons come to mind. The lesser source of recent exuberance is the “Phase 1” trade deal with China. Markets seem to have hailed this deal as a major turning point in Sino-American relations. Trump has certainly trumpeted it as such, with an even better Phase 2 to follow shortly. We believe Phase 1 rather represents only a temporary truce of convenience. If you pick up an official Chinese newspaper, you will read a very different narrative that paints the current deal as “flexible” and the prospects for further negotiation dependent on how the current deal works out. The Phase 1 deal is a nice cease fire: the main American concession being the non-imposition of further tariff increases, with a small token reduction of tariffs currently in place thrown in as well.

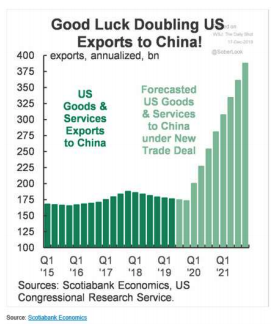

Why do we doubt progress on further deals? First it appears probable that the Chinese purchase obligation required under the pact (shown in the image below) will be nearly impossible to achieve. Is China really going to double imports from us and therefore stop buying from countries that didn’t pick a fight with it in the first place? Fortunately, any disappointing results will mostly come down the road, as Chinese 3 purchases aren’t scheduled to really ramp up until 2021, by which time the Phase 1 deal might have already served its political purpose for the American side. The Chinese side was interested in a reprieve for economic reasons, and they appear to have gotten that. However, further progress in Phase 2 of the sort that would lower American tariffs would require compromise on the issues of technology theft/transfer and state control of the economy... areas where it is very difficult for the Chinese to compromise, and even more difficult, in the case of technological good behavior, for the U.S. to verify.

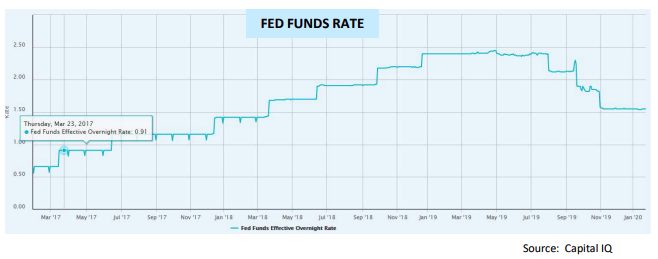

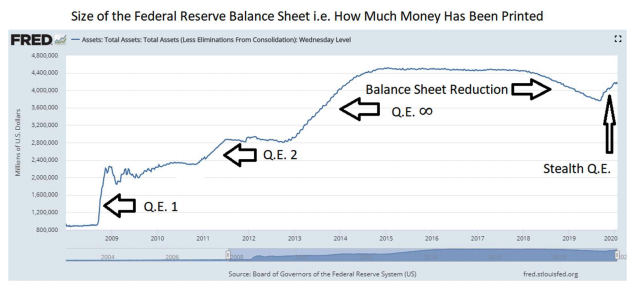

The more important reason that global assets surged in 2019 was the dramatic 180 degree turn in Federal Reserve monetary policy. In January of last year, the Fed was talking about raising rates. In reality, it ended up cutting rates three times last year. The Fed also went from saying its balance sheet reduction1 was on “autopilot”, to turning around and instead expanding its balance sheet in what many have termed “Stealth Q.E.”2. This is the largest change in monetary policy ever seen during an economic expansion.

The Fed will swear up and down that it lowered rates to head off potentially deteriorating economic conditions, and not because the President was browbeating them into doing so3. Likewise, when it comes to its new money-printing operation, the Fed will say that it is nothing like the Q.E. done during the financial crisis and recovery. The financial crisis-era Quantitative Easings (again another euphemism for money printing) were done with the explicit goal of lowering interest rates, raising asset prices, and getting people to spend again. The 2019 operation (aka Stealth Q.E.) is printing and pumping $60 billion dollars a month into the economy for (supposedly) completely different reasons, and therefore shouldn’t be considered Q.E. at all. True or not and regardless of intent4, it has had the same effect: setting risk asset prices on fire. What started out as an extreme measure during the financial crisis is now being deployed on an economy with sub four percent unemployment in its 11th year of expansion.

It seems likely that when money is created and injected into the financial markets, it would naturally flow to the recently highest returning assets: U.S. stocks in general and U.S. tech stocks in particular. Over the past decade, U.S. stocks have continued to steamroll both international developed and emerging market stocks, but even this is largely a technology story. This is because the technology sector represents nearly 30% of U.S. market value, versus ~6% in Europe and ~13% in Japan. That makes a huge difference when U.S. Tech stocks are up a whopping 50%, as they were in 2019.

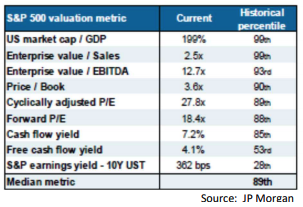

In any case, the monetary actions have driven rates down and asset prices up, stocks included. The table of stock market valuation measures to the right illustrates much of what has transpired with regard to interest rates and valuation. Study it and see if you can spot the outlier.

Most measures are in the top quintile of expensiveness. These measures generally show that stocks are historically expensive, that is, stocks today are expensive compared to stocks five, ten, or fifteen years ago. Interesting to know, but only useful if we expect things to revert back to how they were. Will this happen? Let us defer the question for a moment.

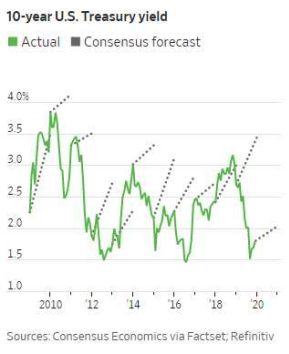

The outlier in the above table is the earnings yield of the S&P 500 (earnings / price) compared to the current 10-year Treasury yield, which is only in the 28th percentile. This means that stocks are historically cheap compared to bond yields available today. Might you say this is a temporary condition? Do you believe, or even know, that rates will rise? The below chart should give you pause.

If one feels uncomfortable predicting with certainty that rates will rise towards the territory they occupied prior to 2008, then why would one feel confident that valuation regimes would return to their previous levels? This is where the Fed has led us: stocks are ever more expensive than their history, but still appear superior to other financial options. One must accept the new reality or sit in cash as asset prices rise and rise. Sitting in cash would indeed be the prudent course of action, if an accurate forecast of a return to previous conditions could be made. We cannot make that forecast at the present time, though we remain vigilant for warning signs.

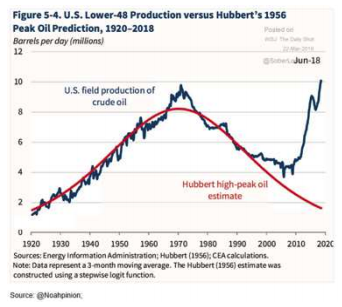

The end of the decade is a good time to reflect back on another technology story that has played out... in the energy sector. There used to be a theory called “Peak Oil” that explained the path of crude oil production in the U.S. The theory was simple: there is only so much oil in the ground and as we get the easy stuff it will become harder and harder to find new sources and production will decline. The theory was looking pretty good until the last decade when it was blown apart by the commercial arrival of hydraulic fracturing and horizontal drilling technologies, i.e. “fracking”.

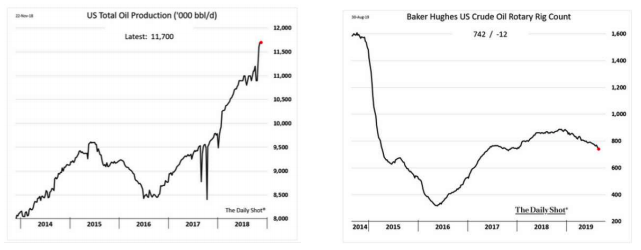

These fracking technologies, developed by private industry but initially funded by the U.S. Government in the 1970’s, allow commercial extraction of tiny pools of oil trapped in shale rocks that were previously thought inaccessible. Upon their introduction, U.S. production exploded upward. This eventually caused the price of oil to fall precipitously after 2014 and many U.S. oil rigs were pulled out of service. But amazingly, U.S. production has continued to climb in recent years despite fewer rigs in service. The continued efficiency gains even after the initial introduction of fracking have been astonishing.

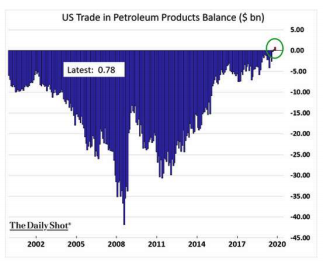

U.S. oil production has expanded to the point where we are now the largest crude oil producer in the world, surpassing powerhouses such as Russia and Saudi Arabia. As production has increased, imports have declined. And while the U.S. does continue to import some blends in certain locations, the U.S. just last year became a net exporter of energy (a definition which adds natural gas to oil). This would have been unthinkable a decade ago.

While this doesn’t mean the U.S. economy (much less the world economy) is immune to oil price shocks, it certainly means it is much less vulnerable than before. Today, in the event of rising oil prices, we would have both winners and losers, instead of just losers. This has geopolitical implications. We can’t help but wonder whether this development played into President Trump’s decision to risk conflict with Iran by assassinating top general Qasem Soleimani via cruise missile. Even the prospect of Middle Eastern conflict used to send worldwide energy markets spiking. Today, the price of oil is significantly lower than it was before the strike.

What was the reward to energy investors for enabling these incredible efficiency gains and expansions in production? Not much. Over the past decade the energy sector returned a cumulative ten percent versus two hundred percent by the broader S&P 500. Energy stocks as a percentage 8 of the index have shrunk from fifteen percent to just five5. This represents a good example of how the capitalistic system works: the main benefits of progress tend to flow to the consumers, not necessarily the pioneers. The low energy prices are probably another reason the economy has been as strong as it has for as long as it has, which has undoubtedly helped the stock market notch gains year after year, in spite of above average valuations.

We appreciate your support and wish all of our readers a happy new year and prosperous new decade.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 When you hear about the Fed’s “balance sheet expansion”, think “money printing”. Therefore a “balance sheet reduction” is the opposite of money printing, taking money out of the economy or “money destruction”.

2 Q.E. is short for quantitative easing, which is when the central bank creates new money and buys longer term government bonds (or other long-term assets) in a bid to strengthen economic growth. Again, just think “money printing”.

3 Either way, we would agree that this was probably the right monetary move.

4 The stated reason for what we have called Stealth Q.E. was to calm an obscure but extremely important corner of the financial markets known as the Repo Market. We agree that at least some intervention was justified.

© Knightsbridge Asset Management, LLC