Almost by definition, value investing rarely performs well in the short run. This is especially true when you are in a strong bull market like we’ve been in since March 2009. Most companies as represented by the S&P 500 are currently trading at fundamental multiples that are significantly above historical norms. Below is a 20-year historical earnings and price correlated FAST Graph of the S&P 500. There are two valuation reference lines on the graph.

The dark blue valuation reference line represents a normal P/E ratio of 18.12. The orange valuation reference line represents a fair value P/E ratio of 15. As you can see, for most of that timeframe market prices traded between those valuation references. However, note the two outliers calendar year 2000 to the beginning of 2002 and calendar years 2017 to current. Clearly, current valuations are high. Not necessarily crazily high as some people believe, but undoubtedly higher than historical norms nevertheless.

S&P 500 Twenty-Year Valuation Levels

Consistent with what I have shown above, many if not most of the most recognized and popular stocks are also currently trading at extremely high valuations relative to their norms or their fundamentals. Famous Dow Jones Industrial Average stocks such as Apple, Walt Disney, Procter & Gamble, Nike, Visa, Microsoft, McDonald’s, Coca-Cola and United Technologies represent just a few good examples of great companies trading at abnormally high valuations. In addition to simply being great companies with superb historical operating results to include superior records of dividend growth, these are also some of the most popular stocks on the planet.

However, as legendary investor Warren Buffett once stated “Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what is popular and do well.” I believe that Warren is trying to tell us that popular stocks are likely to be overvalued whereas unpopular stocks will be where the best bargains can be found.

On the other hand, and what I consider the dark side of being a value investor, is that it often takes a long time before you eventually reap your rewards. Consequently, being a value investor also means being a patient investor. Or perhaps more appropriately stated, being a value investor also implies having a long-term mindset.

This speaks to why Warren Buffett also said “If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.” Stated more directly, value investing rarely produces instantaneous or short-term results, because value investing usually also implies investing in unpopular stocks. This unpopularity is often why they have become valuable (bargains).

Moreover, and from a more practical point of view, we must also acknowledge that value stocks are typically inexpensive for good reasons. This is especially true in a major bull market run like we have been experiencing since 2008. Therefore, the trick is to determine whether the related issues are temporary or more permanent in nature. Additionally, we need to ascertain whether the discounted stock price is justified or perhaps an overreaction. These judgments can help us determine the level of risk we are facing and if we are being adequately compensated for taking it by the low valuations or not.

On the other hand, in the long run value stocks often dramatically outperform and very often do so by taking on significantly less risk than other strategies such as momentum, or in many cases even growth. This is attributed to the fact that the risk is being mitigated by low valuation (price). As a result, I believe the key benefit of value investing is the valuation risk mitigation element. Experience has taught me that stocks that are properly valued, or better yet, undervalued, are more defensive in a bad market than overvalued stocks are. I will be elaborating more on this in the video later.

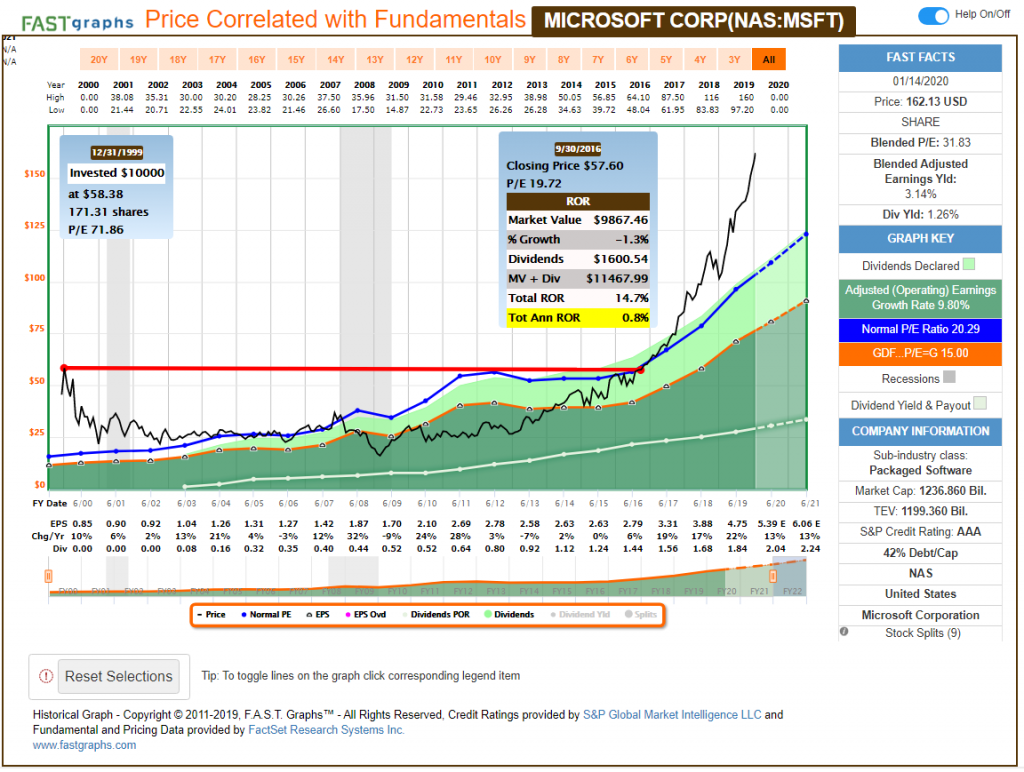

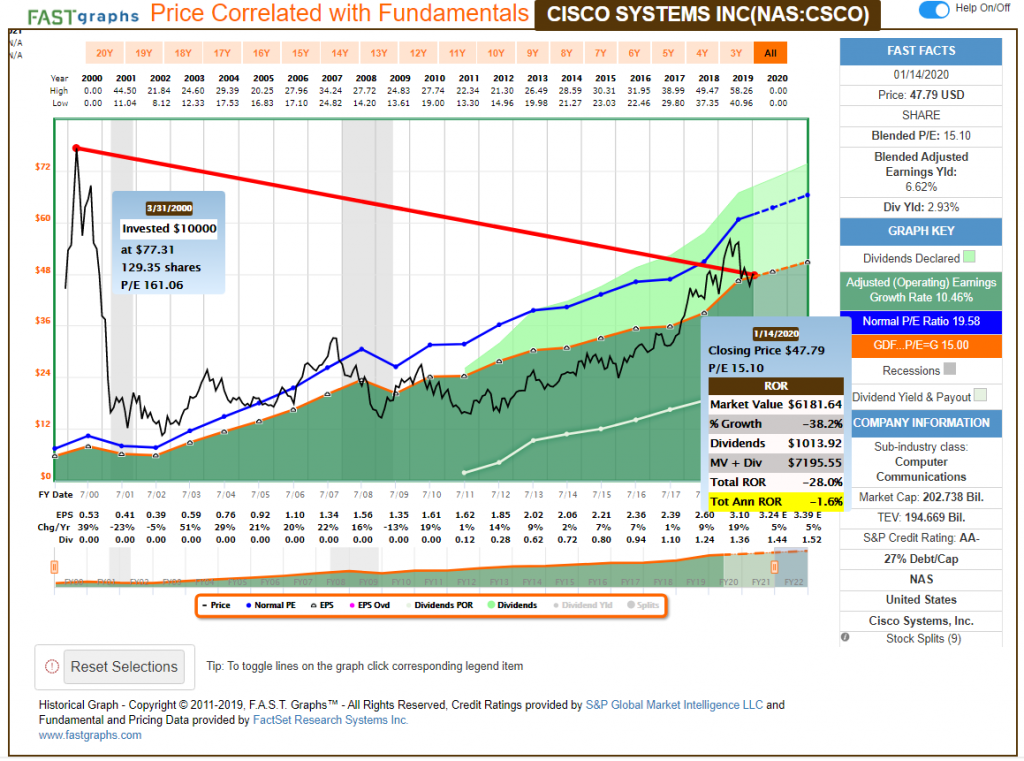

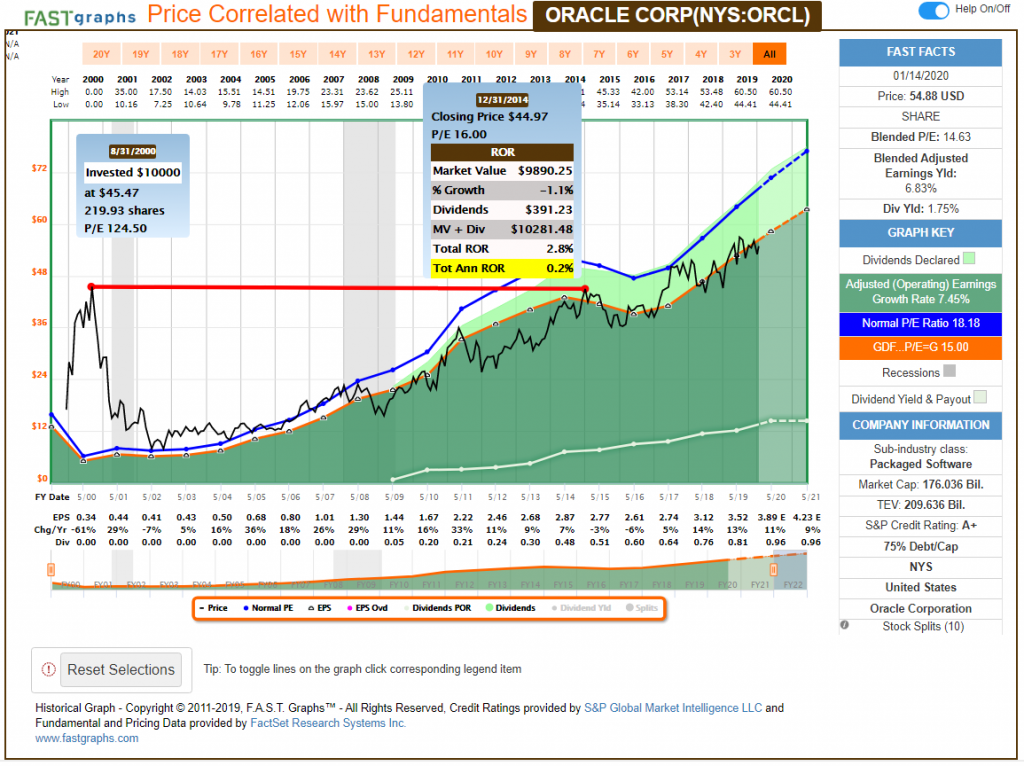

Even though all stocks will fall in a bad market, attractively valued stocks tend to recover much quicker. In fact, if a stock is dangerously overvalued (bubble territory) it may take decades instead of years or months before it recovers. Premier technology stocks such as Microsoft, Cisco and Oracle are three extreme examples that took many years and even decades to return to their peak valuations reached during the tech bubble of 1999 through 2000. In fact, Cisco has yet to get even close to those peak valuations. As I stated many times before, not all price drops are the same.

As illustrated by the three graphs below, being patient is not a very profitable attribute when you are investing in popular stocks that are simultaneously dangerously overvalued. In fact, being a long-term holder of stocks that were purchased when they were at the peak of popularity can result in very long-term periods of dead money. You invested in the very best stocks, but if you paid too much to buy them, therefore, you negate all their potential. Warren Buffett also spoke about this when he said: “For the investor, a too-high purchase price for the stock of an excellent company can undo the effects of a subsequent decade of favorable business developments.” Valuation matters, and it matters a lot.

Microsoft Corp (MSFT)

Cisco Systems (CSCO)

Oracle Corporation (ORCL)

Value Investing Success Takes Time

One of the great dangers of investing in overvalued stocks is that time becomes your great adversary instead of your ally. In contrast, a great benefit of being a value investor is that it puts time on your side. However, at the same time, it often takes time before success manifests for value investors. When you are investing in unpopular stocks, which is where value often comes from it often requires waiting until they become popular again before you can reap your rewards through rising prices.

On the other hand, the above statements are only true if the underlying fundamentals remain solid. To me, the primary difference between a great value investment and a value trap is the strength of the underlying fundamentals. Hence, I have often stated that it makes more sense to focus on the fundamentals than it does to worry about short-term stock price action. Fundamentals are durable, stock prices are ephemeral. Therefore, I have taught myself to trust fundamentals more than I do stock prices.

This is precisely why I have often stated that measuring performance without simultaneously measuring valuation is a job half done. Ironically, I can’t remember even one comment acknowledging this critical element of calculating performance in any article where I have made this statement. Perhaps, that is my fault for not explaining it clearly enough. Therefore, I will be demonstrating how this is done and why it’s so important several times in the video portion of this article.

Furthermore, what I am presenting here only applies if you are a prudent long-term investor. In other words, if you’re looking for short-term profits, value investing is not a strategy for you. To keep this clear in my own mind rather than calling it value investing, I like to think of it as business perspective investing. In other words, I am not seeing myself speculating in a stock, instead, I see myself partnering as a shareholder in a wonderful business that I purchased at an attractive value. Therefore, I am thinking like a business owner not a day trader.

FAST Graphs Analyze Out Loud Video: How Long It Often Takes for Patience to Pay Off Utilizing the S&P 500, Cisco Systems (CSCO), Microsoft (MSFT), Lockheed Martin (LMT) and CVS Health (CVS)

There are numerous ways on how value investing can pay off. You can simply buy a great company that is growing at a sound valuation and then let the growth generate strong future returns. Or, you can buy a slower growing company at a significant bargain and make your money through P/E expansion as the undervalued stock moves back into alignment with fair value. There are other ways that value investing produces good returns, these are just a few examples.

In the following video I’m going to show examples of different ways that value investing can pay off. I am also going to briefly reveal several of today’s overvalued stocks that I mentioned in the introduction. All in all, the video is intended to be a series of lessons on the nuances of valuation – up, down or sideways.

Summary and Conclusions

Value investing works for all categories of stocks. When it is applied to growth stocks it is often referred to as GARP, which is an acronym for growth at a reasonable price. For growth stocks valuation measurements such as P/E ratios and price to cash flow ratios, etc., can be justifiably higher due to the dynamic of compounding at high rates. Nevertheless, the core principles still apply. Value investing implies investing your capital in businesses where their fundamentals represent both soundness and opportunity. Therefore, you are positioned to benefit from the success of the business invested in.

Nevertheless, with the above said, value investing might make the most sense for dividend growth investors. This is especially true for those prudent dividend growth investors that have accumulated enough capital where they can live off their dividend income without sacrificing or harvesting principle. This investor class will prudently focus on the level of dividend income they are receiving with less concern on capital appreciation, especially in the short run. Dividend growth investors that are applying valuation principles will usually expect capital appreciation over time because they understand their value stocks will inevitably move into alignment with fundamental value.

However, the smart dividend growth investors recognize that capital appreciation may not be an immediate benefit. Therefore, the steady dividend payments – especially if they are increasing each year – provide the valuation-oriented dividend growth investor the fortitude to stay the course. For these investors, they are being paid through dividends to wait patiently for capital appreciation to manifest. Since they are primarily investing for the dividend income, they can wait for the prices to rise without undue stress. In other words, their priorities are in the right place. Dividends are much more predictable than stock prices.

In summary and conclusion, value investing of all kinds implies taking the long-term view. To me this also suggests a minimum holding period of at least a business cycle, which is typically 3 to 5 years. However, this is a minimum holding period because sometimes it can take longer. But perhaps most importantly, when we are in a bull market that has been as strong as our current one, investors need to consider the risk they are taking if they are holding overvalued stocks. Frankly, I am seeing a lot of overconfidence in a lot of people that have been spoiled by our current bull market. This is precisely why I have emphasized this so strongly in the video. If you haven’t watched it, please do because I believe the real value and the most important messages of this article are found in the video portion.

Disclosure: Long CSCO,CVS,ORCL

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.