Wasatch Market Scout: Our Take on Emerging Markets—“Don’t Stop Believin’”

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFor most of the past decade, emerging-market stocks have generally underperformed U.S. names and other developed-market equities. Adding to this disappointment, the relatively low emerging-market returns have come with significant volatility.

Despite the fact that our emerging-market strategies have done reasonably well compared to their benchmarks, we’re quick to acknowledge that the long-term emerging-market underperformance and relative volatility were not expected. But rather than capitulating to the view that emerging markets will remain under a cloud, we think a better response is: “Don’t stop believin’.”

In this Market Scout commentary, we explain our reasons for optimism with discussions in four main areas:

- Emerging-market currencies have been weak for years, and this trend may reverse to the advantage of well-chosen stocks in developing nations. Our outlook is informed by similar currency cycles in the past.

- In the “old” emerging markets, companies largely depended on commodity production. But in the “new” emerging markets, the best companies are typically engaged in developing innovative technologies and in serving growing consumer needs. Our expertise is in the “new” emerging markets, and our emerging-market strategies are invested in companies that we believe can create their own destinies.

- The financial metrics of our emerging-market companies and the demographics of our preferred countries are some of the most attractive that we’re seeing in the investment universe.

- India, with its enormous population of young people, is our favorite emerging market of all. We believe India is on the cusp of exponential growth based on its embrace of technology, transparency and the rule of law.

ECONOMIC AND MARKET CONDITIONS OF THE PAST

For the decade that ended in 2010 (generally a period of U.S. dollar weakness and emerging-market currency strength), the MSCI Emerging Markets Index rose a robust 337.02% (15.89% on an average annual basis). But in the nine years ended in 2019 (generally a period of dollar strength and emerging-market currency weakness), the MSCI Emerging Markets Index returned only 20.72% (2.11% on an average annual basis).

After this most-recent nine-year period of disappointing performance, investors probably feel woefully undercompensated for their effort in the emerging-market space—especially compared to the much more satisfying 209.97% (13.39% average annual) return of the S&P 500® Index over the same period. To decide whether or not investors should continue the effort in emerging markets, it’s important to first understand the headwinds that arose in the nine years leading up to the present.

Subsequent to the global financial crisis (GFC) that ended in early 2009, emerging-market stocks generally rebounded for the next two years. But since early 2011, emerging-market names have made relatively little progress overall. Meanwhile, stocks in developed markets—especially in the United States—have mostly performed well.

A couple of related issues that plagued emerging markets in the past several years were 1) the highly competitive interest rates in the United States and 2) the strong value of the U.S. dollar. Compared to the negative rates and the close-to-zero rates in many other developed countries (e.g., Denmark, Germany and Japan), the positive rates in the U.S. attracted capital that might otherwise have gone to emerging markets. This lack of capital made it harder for emerging markets to sustain their earlier-stage economic progress. Similarly, the strong U.S. dollar negatively impacted emerging markets that had previously incurred dollar-denominated debt.

Beyond these issues, there were also political disruptions in emerging markets such as Brazil, Mexico, Russia, South Africa and Turkey. Moreover, declining commodity prices were problematic for many emerging markets that are large commodity producers.

As a result, some of the countries with the worst political problems and the greatest dependence on commodity production saw especially poor stock-price performance and have become smaller components of the major emerging-market indexes. Attention in emerging markets has shifted away from areas where companies extract resources from the earth and toward areas where companies are focused on knowledge-intensive functions and on serving the expanding ranks of consumers.

So while countries like Russia, South Africa and Turkey have become less prominent, countries like China and India have grown in importance. As mentioned, these shifts have been reflected in the major emerging-market indexes—and the shifts have come as the overall level of emerging-market enthusiasm has declined.

WHY AND HOW EMERGING-MARKET CONDITIONS MAY CHANGE

For the reasons described, emerging markets have faced significant challenges over much of the past several years. In a negative, self-reinforcing cycle, these challenges have been reflected in less investor demand today for exposure to the emerging-market asset class. Moreover, since lots of investors prefer passive strategies, this lack of enthusiasm has been especially pronounced for many actively managed emerging-market strategies.

We, on the other hand, have been finding some of our most promising companies in emerging markets. From our perspective, less interest from investors overall means stock prices, in general, haven’t been driven up irrationally. And a lower level of due diligence from active managers means there’s a greater likelihood of inefficient pricing in emerging-market investments.

At an individual level, we think most of the companies held by our various emerging-market strategies have delivered attractive performance from an operational perspective over the past several years. But we believe their stock prices, in general, haven’t kept pace with their operational success—leading us to think the gap will narrow and we’ll “get paid” for our patience.

This brings us to another point regarding high-quality, long-duration growth companies in emerging-markets. At times, we’re willing to pay what seems like elevated prices for such companies because the potential size of the market is so large. In addition, it’s usually justifiable to pay somewhat of a premium for industry leaders because they often have easier and less-expensive access to capital than weak players.

CURRENCIES HAVE TENDED TO MOVE IN CYCLES

At a broader level, our optimism regarding emerging markets in the coming years is partly due to what we believe will be at least a semi-reversal of what happened in the years leading up to the present. As stated, for a good portion of the past several years, the U.S. dollar was in a strengthening cycle that negatively impacted emerging-market company earnings due to effects on borrowing costs, commodities and overall economic tightness. This dynamic has been consistent in past dollar-strengthening cycles.

Moreover, particularly for U.S.-based investors, the stronger dollar hurt emerging-market stock prices due to currency-conversion effects. But prior to that strengthening cycle, the dollar was in a weakening cycle for several years. At some time in the years ahead, we believe there will be a return to a dollar-weakening cycle. And while our investment approach by no means depends on such a cycle, we think dollar weakness would give an added boost to emerging-market stocks. The primary reasons for our longer-term view on the dollar are the likelihood of cyclical slowing in U.S. economic growth, continued dovish U.S. monetary policies and improved fiscal conditions in many emerging markets.

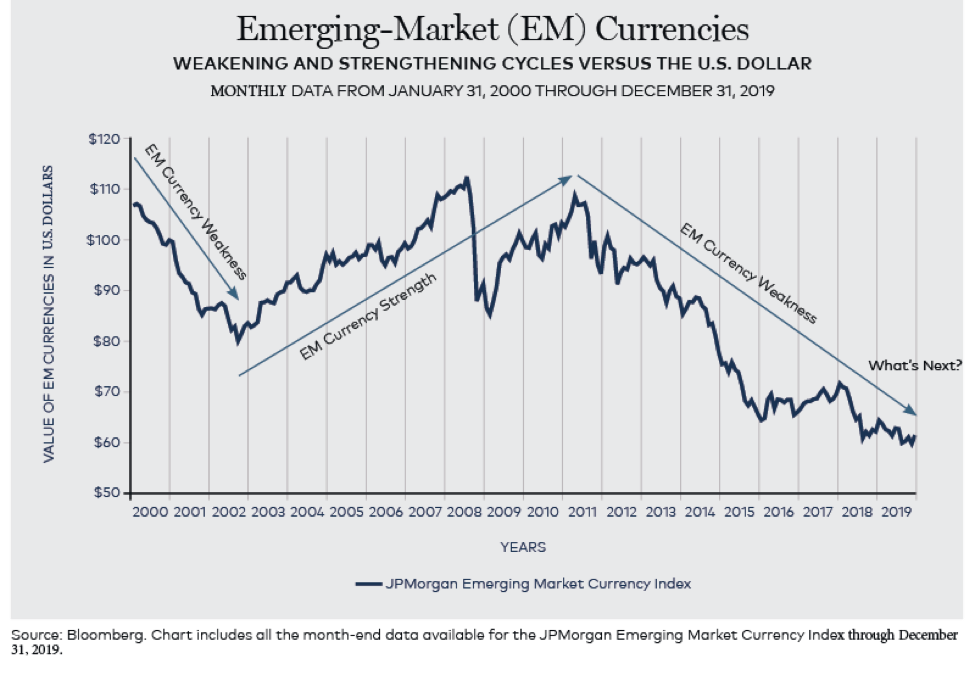

To illustrate the historical strength in the dollar and weakness in emerging-market currencies for the past several years, we note that the JPMorgan Emerging Market Currency Index is down more than -40% from a high in 2011 and is now close to its lowest level since then. So while we cannot predict when this general relationship will shift, we think emerging-market currencies will eventually work in our favor—or at least stop working to our detriment. This should benefit certain countries, industries and high-quality companies in particular.

Figure 1

FINANCIAL METRICS, MACROECONOMIC TRENDS AND DEMOGRAPHICS

In addition to the potential for weakness in the dollar and corresponding strength in emerging-market currencies—the timing of which is impossible to predict—there are other reasons for optimism. For example, median sales growth and EBIT (earnings before interest and taxes) margins are generally higher in emerging markets than in international developed markets. Also, returns on equity (ROEs) and returns on assets (ROAs) in emerging markets roughly match the high quality of international developed markets. These positive financial metrics exist despite the fact that emerging-market stock performance has trailed developed–market stock performance by a wide margin over the past several years. So we think there’s some catching up that’s due on the part of emerging-market stocks.

At a macroeconomic level, we see very large headroom for growth in emerging markets. Just consider the mismatch between global gross domestic product (GDP) and global consumption: Emerging markets account for approximately 43% of the former and only about 27% of the latter. An even more stark contrast is seen in the fact that emerging markets account for only around 12% of the MSCI All Country World Index. Another important point is that although emerging-market GDP is already sizable, GDP growth per capita in emerging markets looks ready to explode much higher in the years ahead.

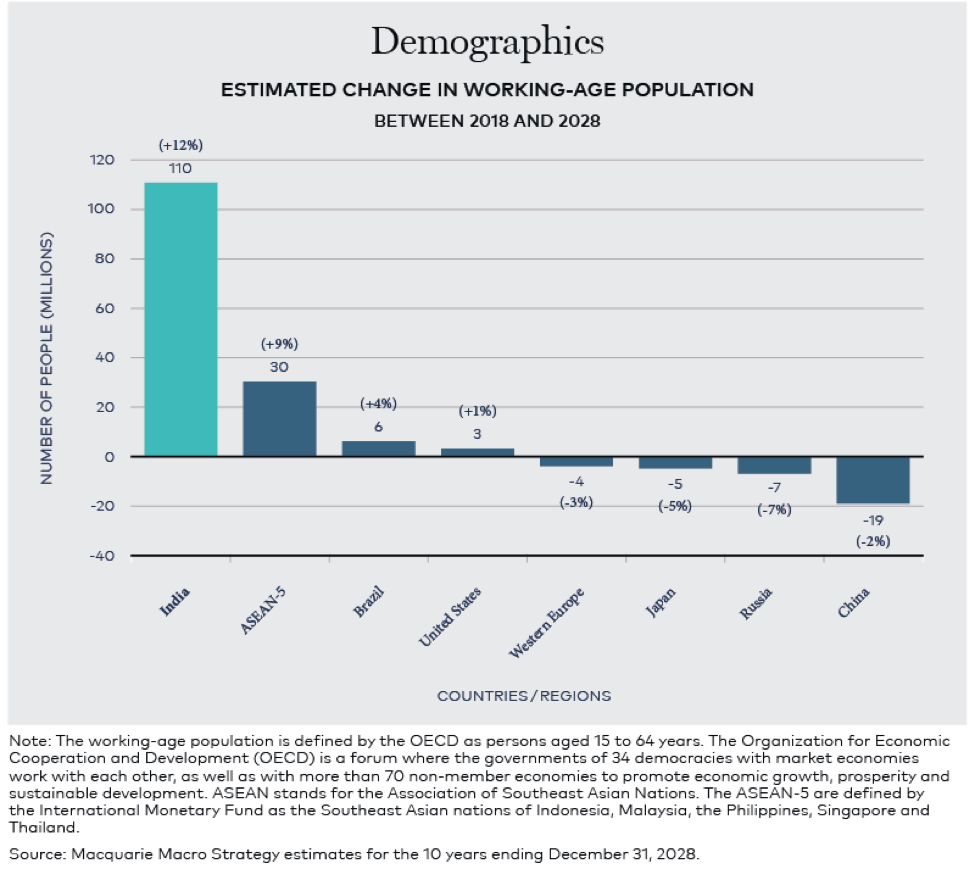

Demographic changes are also occurring in emerging markets. For instance, the change in the working–age population from 2018 to 2028 is expected to be up 12% in India, up 9% in the ASEAN–5 (Indonesia, Malaysia, the Philippines, Singapore and Thailand) and up 4% in Brazil. Unfortunately, China’s working–age population is expected to decline—largely due to the country’s decades-long one-child policy, which has now been reversed. In spite of this expected decline, however, we believe China is an economic powerhouse that’s too big to ignore.

Figure 2

The working-age population is important because it’s some indication of a country’s ability to produce and consume at higher levels and therefore drive long-duration economic and corporate growth. Members of the older segment of the population, on the other hand, tend to show declining productivity and consumption—except perhaps in the consumption of health-care services.

Another boost to productivity comes from the incredibly quick expansion and adoption of internet connectivity. Just consider the level of improvement that the internet makes in the proliferation of financial services, for example, and in the reduction of bureaucracy, waste and fraud. Even the delivery of health care is improved by the internet because patient data and clinical research are more reliable and accessible.

In terms of our ability to pick from a large selection of companies, it’s interesting to note that the number of names in the emerging-market universe has increased by about 7,000 since 1995. And in the past 10 years alone, there have been over 5,000 initial public offerings in emerging markets.

But the vibrant opportunity set of potential investments isn’t just related to the number of companies. Key structural reasons for venturing into emerging markets also include the world–class quality of the businesses surrounded by significant talent pools and tremendous growth in housing, mortgages, banking, insurance, travel, retail, health care, and mobile phone and data services. Moreover, because these businesses are so varied and because they operate in multiple countries, there’s ample opportunity to create well–diversified emerging-market strategies.

TAILORING OUR INVESTMENT APPROACH FOR THE COMING YEARS

In addition to the strong overall case for emerging markets in the years ahead, we believe some of the structural changes that began around the time of the GFC in 2008 will continue. First, emerging markets have become increasingly different from one another regarding their stages of political and economic development. Second, dispersions of investment returns by country have grown larger across the world’s many emerging markets. Third, because the emerging-market universe has become a progressively diverse asset class for stocks, conditions have rewarded more active risk-taking at the country level.

Beyond these general conditions, differences have been exacerbated among “hard-currency” and “soft-currency” countries. The Taiwanese dollar, which has been very stable, is an example of a hard currency. On the other hand, the Turkish lira, which has been extremely weak, is an example of a soft currency. As a result, investors need to be aware that country and currency risks can be significant and can overwhelm company-, industry-, sector- and style-specific influences.

In fact, of the overall risk in emerging-market investing, almost 65% can be explained by country risk. As a result, it’s important to make good decisions regarding country selections. At Wasatch, we seek to optimize the risk/reward tradeoff by employing various proprietary and non-proprietary investment models. We also tend to concentrate our emerging-market strategies in fewer stocks and in fewer countries than many other portfolio managers. This way, we stay properly diversified—but not overdiversified—and our best decisions have the most potential to yield meaningful results.

Our proprietary investment models generally help us uncover high-quality, long-duration–growth companies that we want to research further—even in places that are experiencing challenging environments. The non-proprietary investment models that we use tend to alert us to positive and negative conditions at the country level (e.g., politics, fiscal conditions, inflation and interest rates). And when we venture into countries with higher risks, we typically want to see the potential for especially strong results.

WHAT WE LOOK FOR IN EMERGING-MARKET COMPANIES

Apart from these overall guidelines for our investment approach, we’re more committed than ever to finding innovative companies serving home-country consumers in areas benefiting from digitalization, financialization and the formalization of emerging-market economies. We’re generally much less interested in companies that primarily export goods and services to the developed world. And we largely avoid commodity-oriented companies, as we believe emerging markets are moving past their reliance on extracting resources from the earth.

So far in this Market Scout commentary, we’ve laid out the case for emerging-market investing based on positive macro conditions—especially in certain countries—and the vast opportunity set of stocks listed on the various exchanges. But it’s also important to note that macro conditions only take us so far and that all emerging-market companies are by no means created equal.

What we look for in companies can be generalized as strong financial quality and long-duration growth. Strong financial quality is usually defined as having high returns on capital, significant cash flows and reasonable financial risk. In terms of long-duration growth, we like to see healthy sales and earnings increases—ideally in double-digit percentages—both in the past and projected for the future.

More specifically, we search for companies able to grow in different economic environments. In many cases, these companies are beneficiaries of new technologies and have hard-to–overcome competitive advantages. For example, Silergy Corp. is a Taiwanese powerhouse in innovative mixed-signal and analog integrated circuits primarily used to measure energy use and to improve efficiency and conservation. Similarly, Argentina-based MercadoLibre operates dominant, large-scale online marketplaces and payment services in Latin America.

What Silergy and MercadoLibre have in common is that they’re both examples of our focus—above most other considerations—on identifying world–class companies. But Silergy is headquartered in a hard–currency country while MercadoLibre is headquartered in a soft-currency country with political and economic turmoil. Although our preference is for great companies in great environments, we’re willing to accept some environmental challenges if the company is truly special and if we believe it can more than overcome macro headwinds.

INDIA IS PARTICULARLY WELL POSITIONED

At Wasatch Global Investors, the core elements of our approach include an attempt to ensure that we’re mindful of where the wind is at our backs. And more than in any other emerging market, we believe the wind is at our backs in India—especially among small companies.

Consider that India is home to more than 1.3 billion citizens—over a sixth of all the people in the world—and is one of the fastest–growing major economies on the planet. India also benefits from a relatively young population’s willingness to embrace technology, transparency and the rule of law. Extremely rapid progress has ensued from there.

A young population is important because radical change is more likely to be accepted by people who haven’t lived long lives under an obsolete paradigm. In fact, with over 65% of its total population under age 35, India has the largest group of young people on the globe. In the next decade, the estimated change in India’s working–age population (ages 15 to 64) will be 110 million—making India’s workforce the world’s biggest at about one billion people, many of whom speak English.

Technology has allowed India to bypass outmoded stages of development in the ways people communicate, the ways they live and the ways they work. As an example, just imagine struggling in poverty and then—almost overnight—using a cell phone to access a bank account, receive mobile payments and buy modern consumer products. It’s not surprising, then, that India’s labor–productivity growth has been rising, while productivity growth has been slowing in most major economies.

Transparency—protected, of course, by world-class security—has allowed technology to function properly. Without transparency, technology would be limited in its ability to improve peoples’ lives. For instance, the Indian government wouldn’t be able to help the poor as effectively if people weren’t willing and able to disclose their identity, their circumstances and their needs.

Moreover, transparency is a vital aspect of the rule of law, which is a basic element of a thriving economy. People need to know that corruption will be exposed and that what they earn and save won’t be stolen through malicious schemes. The rule of law encourages people to engage in productive work and pay their taxes.

A person from a developed region visiting India might be surprised by our enthusiasm for the country’s potential. After all, India is still plagued by poverty, pollution and poor infrastructure. But as we like to say, these things only represent the country’s “hardware,” or what can be seen on the surface. We believe the country’s “software,” what can only be seen by looking deeper, is in much better shape.

India’s software is mostly responsible for the country’s technological innovation and first-world conveniences, which are developing at breakneck speed. This is why we think a country’s software is much more important than its hardware for winning in the 21st century.

A final point about India is that it’s been a “soft-currency” country for the past several years. Yet in spite of this headwind, our Indian stock selections and overall performance—even after currency effects—have been especially strong. You can read more about “India’s Virtuous Circle of Amazing Progress” in the News & Insights section of our website. This section also contains other recent articles and white papers.

REASONS WE BELIEVE NOW MAY BE THE TIME TO BE CONSTRUCTIVE

Many popular aphorisms make the point that if you want to know where you’re going, you need to know where you’ve been. To a large extent, this is how we feel about emerging markets. The obvious caveat, however, is that in investing we never really know for sure where we’re going. But we do know where we’ve been. And we understand how emerging markets performed subsequent to historical events that we think are similar to events of recent years.

In this regard, we know that for a few decades, emerging-market currencies as a group have moved up and down relative to the U.S. dollar within a general range. Although we believe the current currency mismatch will reverse at some point, we’re not relying on such a reversal. There are other factors that we think will provide a tailwind for emerging markets: Central banks have expanded their reserves of foreign currencies, which should tend to enhance investor confidence. Emerging-market currencies themselves have better backing because current–account deficits relative to GDP have generally come down in the past few years. Moreover, inflation rates have declined and seem to be stabilizing.

Relative to developed markets, emerging markets overall have lower public debt levels, higher domestic savings rates and better profits on investments. Moreover, emerging-market price-to-book value ratios are generally below their long-term averages. And the volatility of the MSCI Emerging Markets Index has come down in the past several years.

Again, while we believe the broad emerging-market universe has become more compelling from an investment standpoint, we think the old commodity-oriented companies will continue to decline in relative attractiveness. At the same time, we’re optimistic regarding new business models that in some instances will even leapfrog those in the West due to the enabling factor of technology. Based on the need to research and understand these business models, we believe active portfolio management—a key Wasatch strength—is especially important.

With sincere thanks for your continuing investment and for your trust,

Ajay Krishnan, CFA

Dan Chace, CFA

Scott Thomas, CFA

RISKS AND DISCLOSURES

Mutual–fund investing involves risks, and the loss of principal is possible. Investing in small–cap and micro–cap funds will be more volatile, and the loss of principal could be greater, than investing in large–cap or more diversified funds. Investing in foreign securities, especially in frontier and emerging markets, entails special risks, such as unstable currencies, highly volatile securities markets, and political and social instability, which are described in more detail in the prospectus.

Diversification does not eliminate the risk of experiencing investment losses.

An investor should consider investment objectives, risks, charges and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit wasatchglobal.com or call 800.551.1700. Please read the prospectus carefully before investing.

Information in this document regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

The investment objective of the Wasatch Emerging India Fund, Wasatch Emerging Markets Select Fund and Wasatch Emerging Markets Small Cap Fund is long-term growth of capital.

Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk.

As of December 31, 2019, the percentage of net assets of Silergy Corp. held in the Wasatch Emerging Markets Select Fund was 5.4% and the Wasatch Emerging Markets Small Cap Fund was 4.3%. The Wasatch Emerging India Fund did not hold Silergy Corp. The percentage of net assets of MercadoLibre, Inc. held in the Wasatch Emerging Markets Select Fund was 5.3%. The Wasatch Emerging India Fund and the Wasatch Emerging Markets Small Cap Fund did not hold MercadoLibre, Inc.

Wasatch Global Investors is the investment advisor to Wasatch Funds.

Wasatch Funds are distributed by ALPS Distributors, Inc. (ADI). ADI is not affiliated with Wasatch Global Investors.

DEFINITIONS

The Association of Southeast Asian Nations (ASEAN) is an organization of countries in southeast Asia set up to promote cultural, economic and political development in the region. The ASEAN-5 are Indonesia, Malaysia, the Philippines, Singapore and Thailand.

The global financial crisis (GFC), also known as the financial crisis of 2007-09 and 2008 financial crisis, is considered by many economists to have been the worst financial crisis since the Great Depression of the 1930s.

Gross domestic product (GDP) is a basic measure of a country’s economic performance and is the market value of all final goods and services made within the borders of a country in a year.

A “hard currency” refers to money that has had a stable exchange rate over a long period and generally comes from a country with a strong economy and stable political structure. The most common hard currencies include the U.K. pound sterling, the euro and the U.S. dollar.

An initial public offering (IPO) is a company’s first sale of stock to the public.

The JPMorgan Emerging Market Currency Index measures the strength of the most traded developing country currencies against the U.S. dollar. You cannot invest in this or any index.

The MSCI All Country World Index is a free float-adjusted market capitalization weighted index designed to measure the equity market performance of developed and emerging markets.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index designed to measure the equity market performance of emerging markets.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indexes or financial products. This report is not approved or produced by MSCI. You cannot invest in these or any indexes.

The price-to-book value ratio is used to compare a company’s book value to its current market price.

Return on assets (ROA) measures a company’s profitability by showing how many dollars of earnings a company derives from each dollar of assets it controls.

Return on capital is a measure of how effectively a company uses the money, owned or borrowed, that has been invested in its operations.

Return on equity (ROE) measures a company’s efficiency at generating profits from shareholders’ equity.

The S&P 500 Index includes 500 of the United States’ largest stocks from a broad variety of industries. The Index is unmanaged and is a commonly used measure of common stock total return performance. You cannot invest in this or any index.

Sales growth is the increase in sales over a specified period of time, not necessarily one year.

A “soft currency” refers to the money of a specific country that is liable to depreciate in value and is difficult to exchange for another currency. Soft currencies are typically those of developing nations with relatively unstable governments and uncertain economic prospects.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits