Understanding how to value a business is the key to avoiding making obvious mistakes when purchasing or selling common stocks. When you know what your investment is worth, the market cannot take advantage of your gullibility. When you don’t know what your investment is worth, markets can easily influence you with fear or greed. When emotions rule, logic goes out the window. This series of articles has been focused on helping the reader understand what fair value is, how it’s calculated and how it can be used to be a smarter and more successful long-term investor.

A second key is to recognize that these principles apply to long-term investing. As Ben Graham so aptly put it “in the short run the market is a voting machine, but in the long run it is a weighing machine.” The critical aspect of Ben’s profound statement is to accept the reality that the market can and will miss price stocks over short periods of time. On the other hand, it is also a reality that the markets will improperly value stocks over several years. This often is what gets investors in trouble.

However, true prudent value investors recognize that inevitably a company’s stock price will move into alignment with its true worth valuation. It is not a matter of if, but only of when it might occur. Smart investors recognize anomalous values and are prepared to take appropriate action as they occur. This could mean being aware, and therefore, being prepared to take action, or it can also simply mean taking immediate action. Nevertheless, it’s the awareness that is the key to long-term success.

Principles of Valuation Part 4:

In this, my final installment of my series of articles on when and why to buy a stock, I will focus on how to use the principles of valuation to avoid obvious mistakes. As mentioned in previous articles, investing is never a game of perfect. The best that an investor can hope for is to make sound long-term decisions, with most of them working out to their benefit in the end.

However, investing is a very complex endeavor, and mistakes are inevitable. Therefore, it’s imperative that the obvious mistakes – which can and should be avoided – are avoided.

Obviously, mistakes usually occur when the market or people are caught up in emotion. As we all know, the primary emotional responses that can affect investor behavior are fear and greed. When gripped by the hype from greed or by the hysteria from fear, investors rarely behave rationally. It is during times like these when stock prices can become disconnected from true worth valuations. This undeniable fact that stock values are not always rational needs to be recognized and accepted.

In my opinion, one of the primary reasons why investors often make bad investment decisions is because their judgment is usually based only on price movement. As I will illustrate, price movements alone can be very misleading. A rising stock price will often lull an investor to sleep creating a false sense of security where they believe that all is well.

On the other hand, a falling stock price usually creates anxiety and sometimes leads to outright panic. These feelings can only be rational if they are justified by sound fundamentals. Knowing the differences between rational and emotional reactions will make all the difference, as the following examples will illustrate.

In part 1 of this series a comment was made that disturbed me personally. It is not that I was offended by the comment, instead, I was saddened by it. The notion that people refuse to believe that there is no such thing as the intrinsic value of a business is quite dangerous. In truth and fact, I have seen this simple fact destroy more investors’ financial futures than I care to count. I saw it during the tech bubble, and I saw it again during the Great Recession. From my personal experience, this all started after modern portfolio theory hijacked the financial industry. One of their foundational tenants is the efficient market hypothesis. This is the notion that the markets are all-knowing, and that all relevant information is correctly factored in to market prices (stock prices) at all times. Of course, simple common sense indicates that to be nonsense.

Nevertheless, here is the comment referenced above that attempts to deny the reality that a business has an intrinsic value:

“others believe that there is no such thing as intrinsic value.

This is not subject to belief. Only Marx and his early followers thought that labor had intrinsic value. His views on the subject are laughable now.

There are only two kinds of value: individual, quantified by a utility function; and market value, which is the price at which something is transacted. People speaking of intrinsic value don’t know basic economics.”

Perhaps the individual (that will remain nameless) who made the above comment studied economics under the influence of Modern Portfolio Theory. However, I was fortunate enough to be taught economics prior to what is being taught in finance today. As Warren Buffett so aptly put it “I’d be a bum on the streets with a tin cup if the markets were always efficient.” It is a ludicrous idea to believe that stocks are always priced correctly by the market – they are not. Later in the article I will provide irrefutable evidence regarding the veracity of that statement.

With that said, once you recognize and understand that businesses do have intrinsic value, you can learn how to measure that value within a reasonable range of accuracy, and by doing so, protect yourself from making obvious mistakes. Investing is hard, and some mistakes simply cannot be avoided. However, extreme levels of risky overvaluation are obvious and can – and should – be easily avoided. In a bull market like we are currently in, investors must protect themselves from becoming so-called “geniuses in a bull market.” Although less than extreme levels of overvaluation are less obvious, they can also be rationally dealt with if the investor understands what gives a business value and how to calculate it.

Of course, the opposite is also true. Extreme levels of undervaluation can also be correctly evaluated when you understand how to value a business. The obvious mistake here is to sell a business for far less than its worth while simultaneously turning an unrealized paper loss into a real loss. I have seen this action destroy more capital than anything else. Instead of getting excited when one of their stocks goes on sale, investors panic instead and throw away valuable assets.

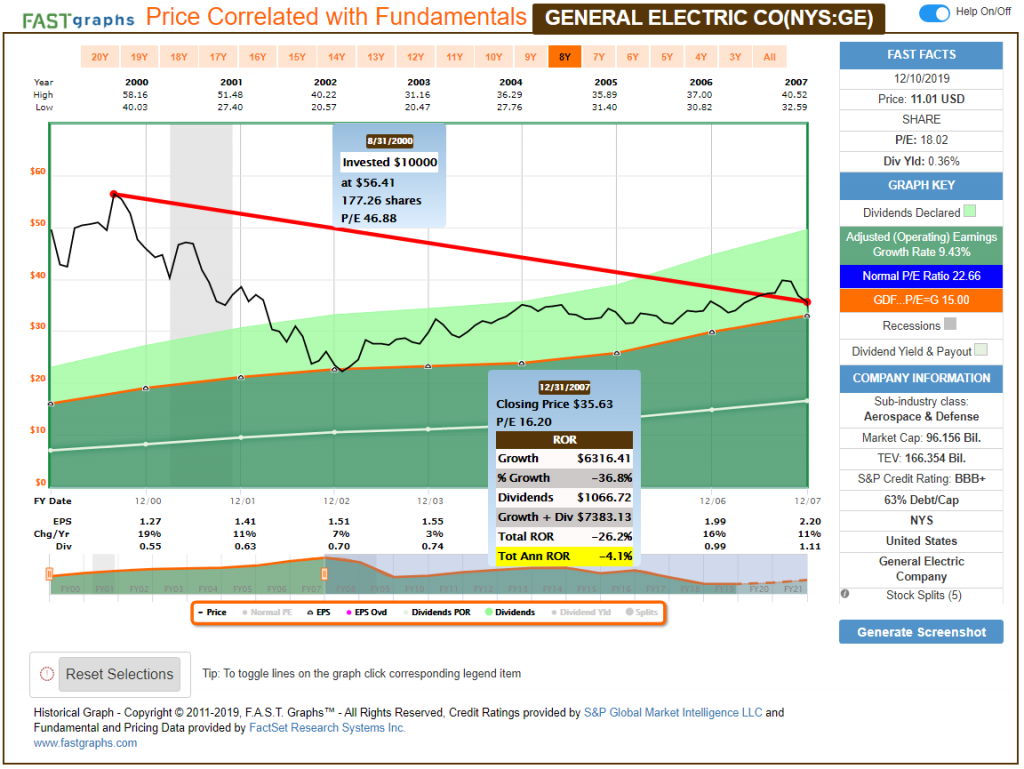

When General Electric’s Stock was an Obvious Mistake

To illuminate these points, let’s look back in time at General Electric Co. (GE), a once highly regarded blue-chip. The following FAST Graphs plot General Electric’s stock price starting with the infamous irrational exuberant timeframe 1999, and then going out to year-end 2007. On August 31, 2000, General Electric’s stock price was trading at a peak P/E ratio of approximately 47 while earnings were growing by 19% in 2000 followed by 11% in 2001.

Those rates of growth would suggest a fair value P/E ratio of 15 (the orange line on the graph) as I discussed in the previous installments of this series. Nevertheless, General Electric’s multiple (P/E 47) was almost 5 times its growth rate (9.43%) over this timeframe. This is a clear case of an obvious mistake for investors that were buying General Electric stock during this timeframe. Even a rudimentary understanding of valuation should have told investors that the market was clearly valuing General Electric’s stock with irrational exuberance.

Excessive valuation led to more than 7 years of negative returns. Dividend income helped soften the blow, but not enough to overcome net losses averaging 4.1% annualized. Even worse, General Electric’s stock price has yet to come even close to those historic highs it set during the irrational exuberant period. Moreover, as you will soon see, this is prior to the fundamental deterioration that General Electric’s business eventually fell into.

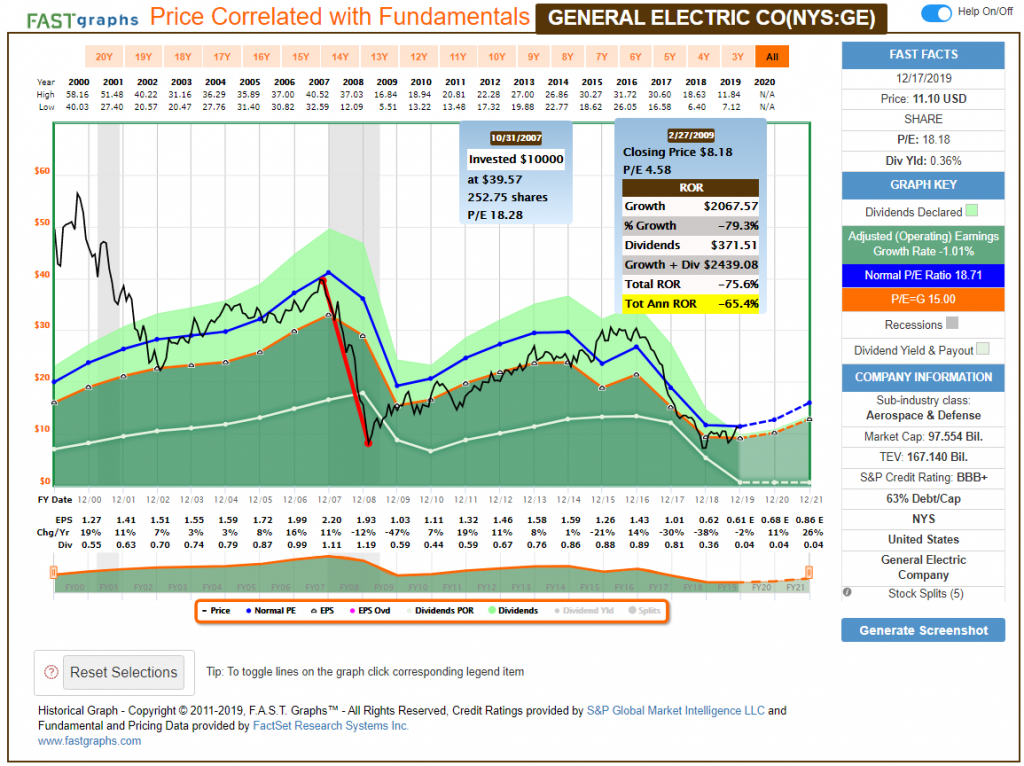

These were the final years of the Jack Welch era, and shareholders were in investing bliss, loving both the company and the stock. What happened next with General Electric was initially less obvious but soon it should have become clear that General Electric’s business was experiencing fundamental challenges.

For example, on June 18, 2009, General Electric slashed its dividend in reaction to collapsing earnings (fundamental deterioration). Of course, stock price followed dropping more than 79% from peak to trough valuation as depicted in the following graphic. Additionally, we see the undeniable relationship between earnings and stock value that has occurred since.

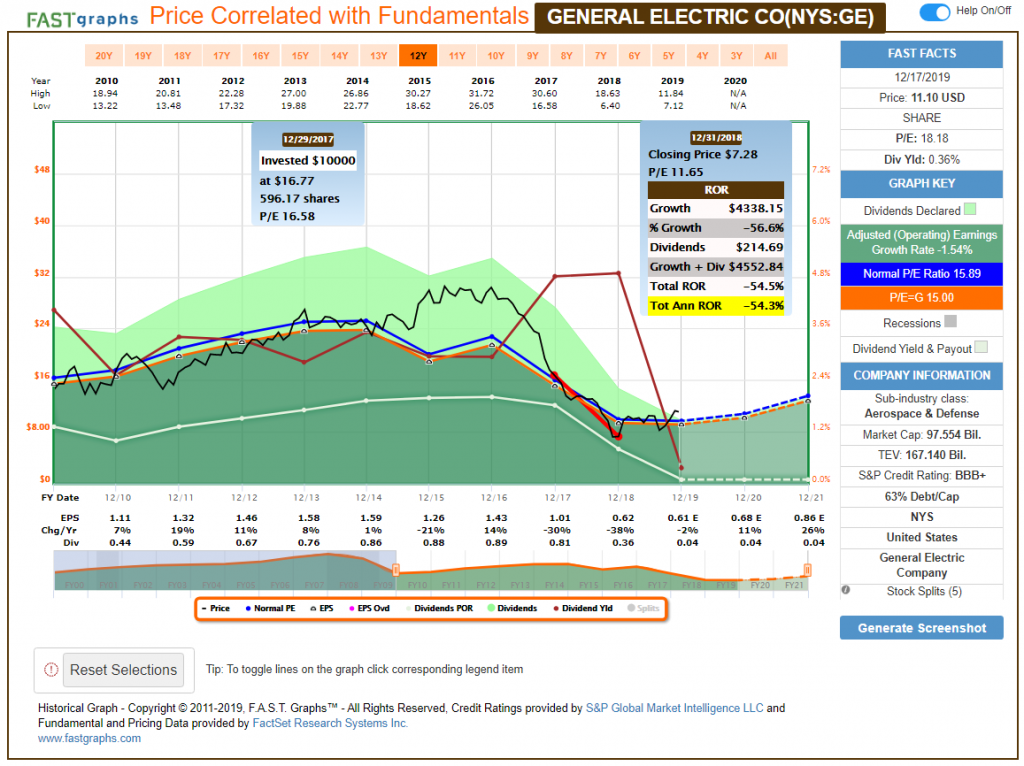

The moral of this final chapter in this General Electric story is that valuation is not simply a statistical calculation. For example, in December 2017 General Electric was offering shareholders a dividend yield of approximately 4.8%. By December 2018, the stock was still generating a 4.89% dividend yield and was available at a low P/E ratio of approximately 11. However, this was only after the earnings, the stock price and the dividends had all fallen precipitously. Earnings fell 38%, stock price fell 54% and the dividend was slashed by 56%. Therefore, at the end of 2018 statistically General Electric looked like an attractive stock. So obviously, in addition to statistical references, investors must also keep their eye on fundamentals.

Recognizing the Obvious Mistake of Overvaluation

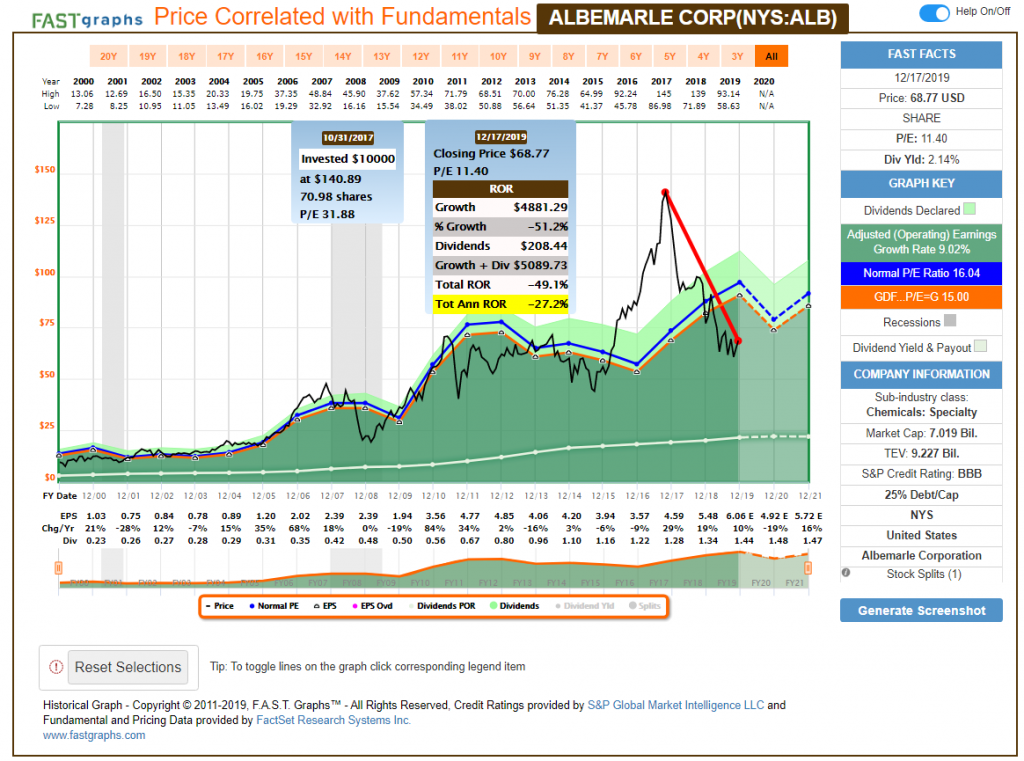

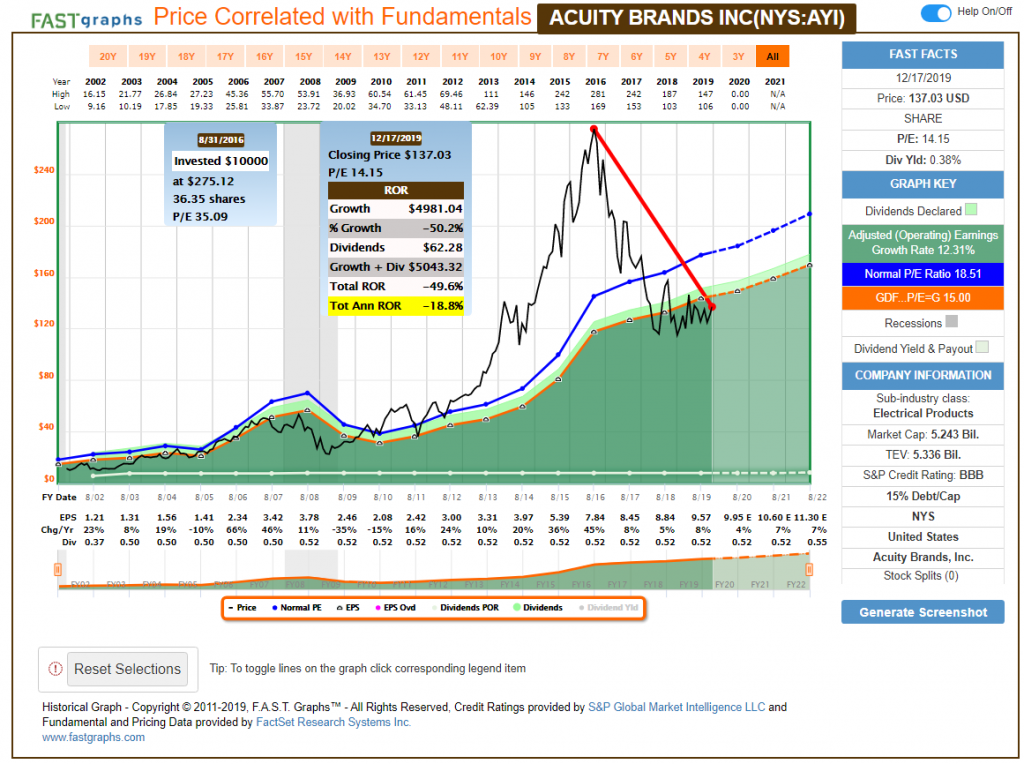

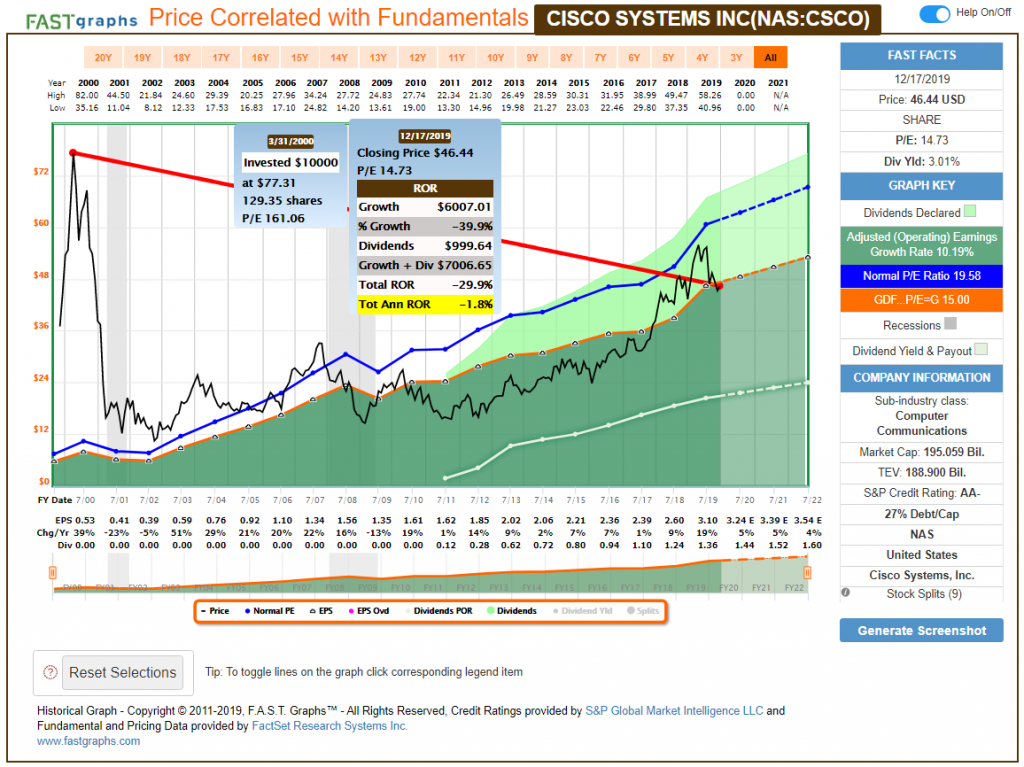

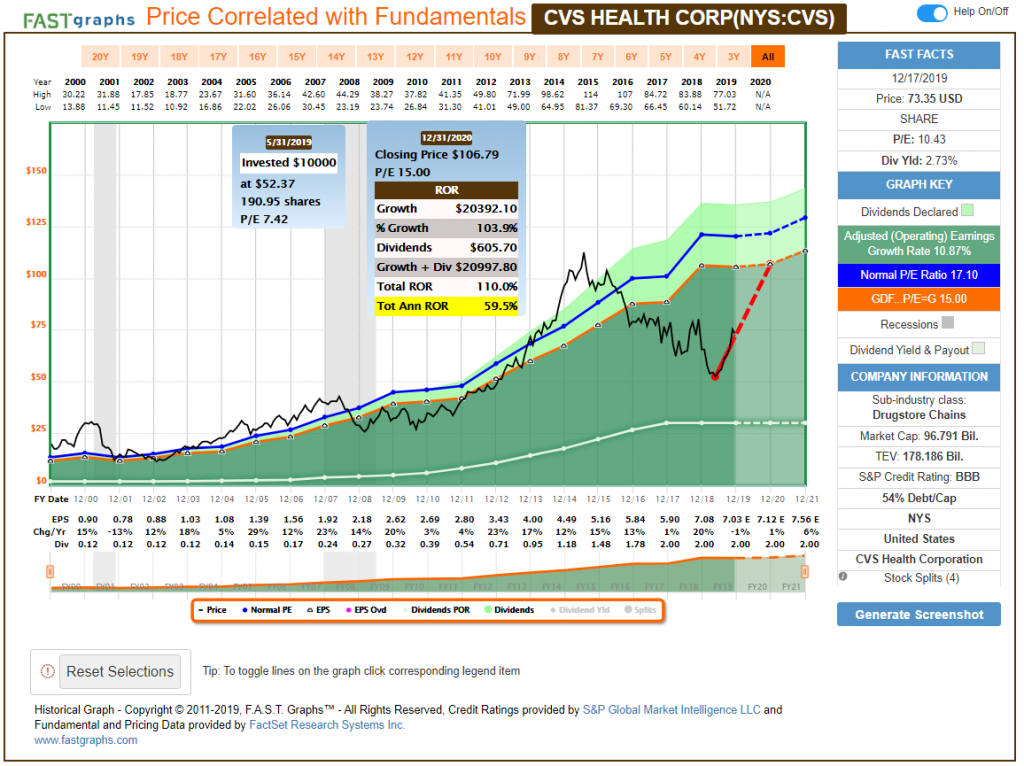

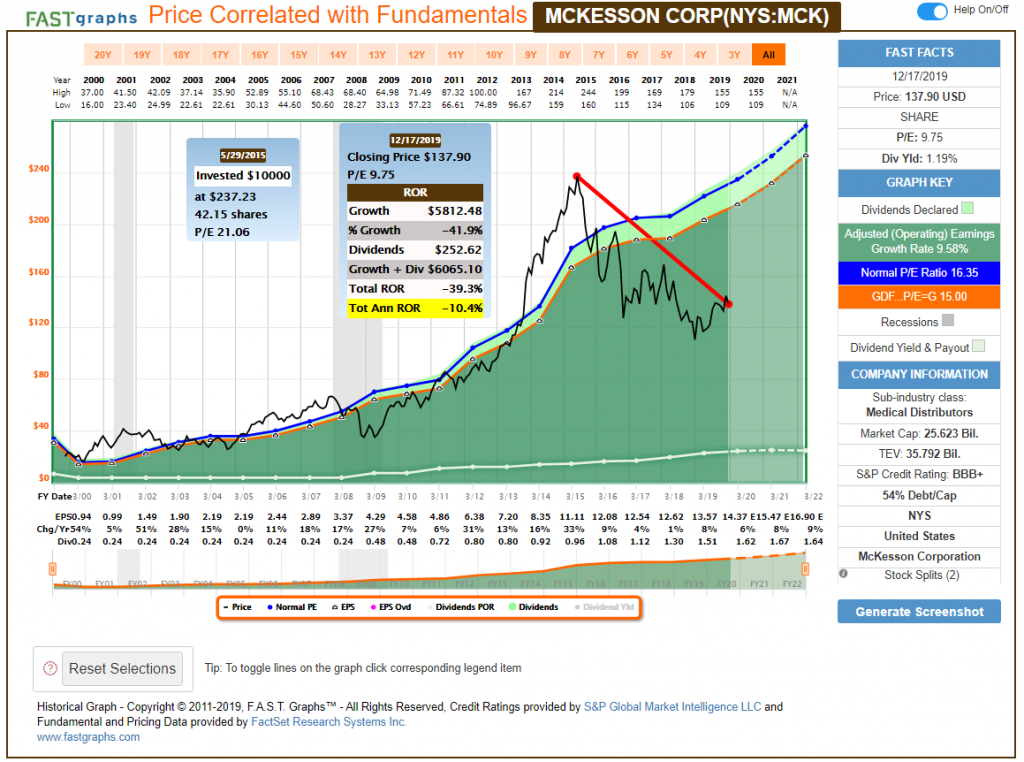

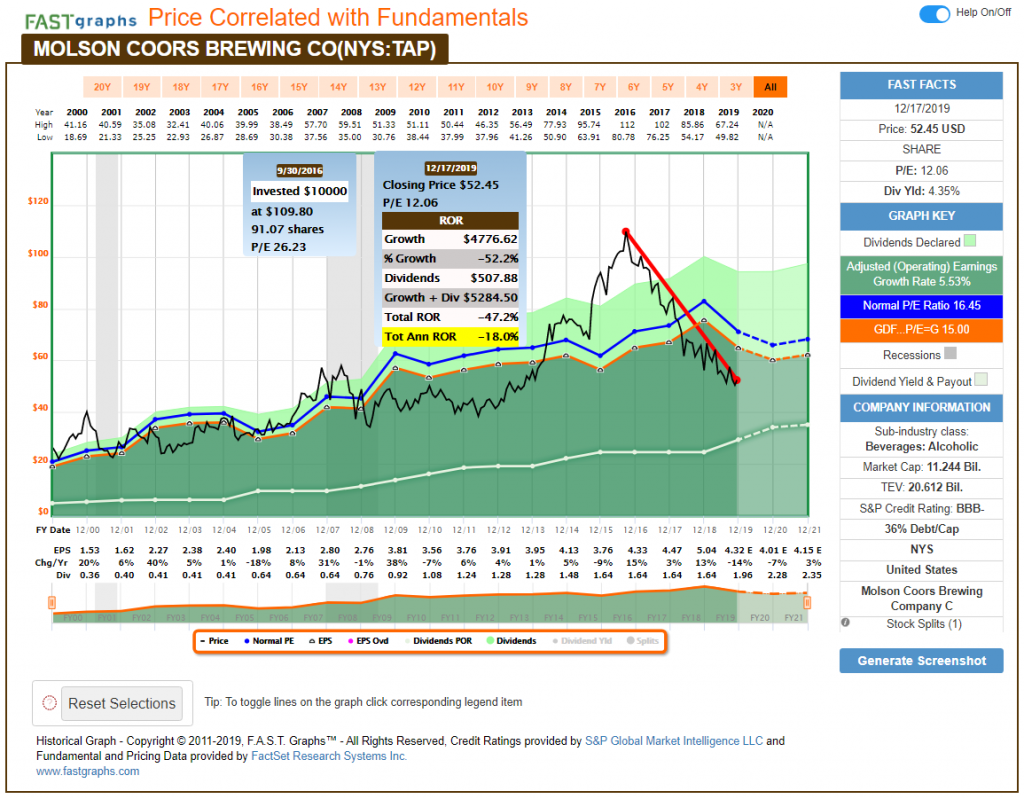

I present the following earnings and price correlated long-term FAST Graphs on several companies as classic examples of when overvaluation was an obvious mistake. With each example it should be crystal clear that stock price had become significantly separated (way above) earnings or fundamental justified valuations.

When this is occurring, stocks become very vulnerable to any type of news that can cause investor sentiment to change. And when it does, the results are usually swift and severe. Consequently, I consider overvaluation one of the biggest risks that investors face, especially when we are experiencing a long-running bull market like we have today.

In essence, I consider this the equivalent of playing musical chairs with your money. Everything is fine as long as the music is playing, but once it stops, investors discover that there is no chair beneath them to support their assets. Nevertheless, with the simple application of basic common sense and simple mathematical realities, overvaluation is a mistake that is obvious that can and should be avoided.

Although these pictures tell a compelling story, in the FAST Graphs analyze out loud video that follows I will elaborate on these important valuation principles. Personally, I believe the real value of this presentation will be found by watching the short video. Please don’t miss it.

Albemarle Corp (ALB)

Acuity Brands Inc (AYI)

Cisco Systems (CSCO)

CVS Health Corp (CVS)

McKesson Corp (MCK)

Molson Coors Brewing (TAP)

FAST Graphs Analyze Out Loud Video: Overvaluation and Undervaluation Are Obvious Mistakes

Conclusions

This series of articles was written in order to provide a foundation of understanding of the principles behind the concept of true worth valuation, also known as intrinsic value or fair value. The idea here is that there is a mathematical basis for value that is a logical function of cash flows or earnings.

In other words, since an investment derives its value from cash flows or earnings, the trick is in knowing how to value the cash flows or earnings an investment generates. The simplest way to accomplish this is to calculate the actual rate of return that the cash flows generate on a given level of investment. Personally, I believe a great shortcut is the inversion of the P/E ratio which provides the earnings yield that the stock is currently offering investors.

After you calculate the returns that your cash flows are giving you (the earnings yield), then it’s only logical to compare those returns to what you can earn from a so-called riskless instrument like a treasury bond. If the cash flows you are earning from your risk investment (example a stock) are not significantly greater than what you could earn from a riskless investment like a treasury bond, then you should immediately recognize that something is terribly wrong.

Why take high risk for lesser return? It simply does not make any sense. However, the only way to know that is to run the numbers and do the calculations.

Calculating valuation correctly is a direct function of forecasting future cash flows accurately. Logic dictates that this is a formidable task that is fraught with traps and surprises. One the other hand, logic and reason applied intelligently can be up to the task within reasonable ranges of probability. Little research and due diligence will go a long way here. Learn from the past, identify the present and do your best to come up with a reasonable forecast of the future.

Remember, forecasting future income streams does not have to be done perfectly, but it does need to be done rationally. Obvious mistakes, that should be avoided, are made when there is no reasonable or rational possibility that valuations can be justified by accomplishable future growth. Simply stated, run the numbers out to their logical conclusion. Never invest in a stock hoping that it can go up. Instead calculate a reasonable range of returns that you believe the company in question is capable of generating on your behalf given current levels of valuation in conjunction with prospects for future growth.

Disclosure: Long CSCO and CVS

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.