In part 2 of this series I focused on how to value slow and moderately growing businesses. In this article, Part 3, I will shift my focus on how to value faster growing companies (growth stocks). My definition of a fast grower (growth stock) is one that has consistently compounded earnings at 15% per annum or better over extended periods of time (five years or longer). Furthermore, the more consistent the growth has been, the better it fits my definition of a pure growth stock.

In Part 1, I also offered the idea that a P/E ratio of 15 was appropriate for most companies. However, with this article I will further refine that concept by suggesting that a P/E ratio of 15 applies when growth rates fell in the range of 0% to 15%. In other words, in addition to the fact that the P/E ratio of 15 has been the average for indices like the S&P 500, there is also a logical and mathematical reality behind its validity. However, although a P/E ratio of 15 was an appropriate valuation to pay for growth of up to 15%, I also pointed out that it did not necessarily indicate the rate of return investors should expect to receive. The ultimate rate of return achieved will be related to the valuation paid and the subsequent growth that the company achieves.

Also, the 15 P/E ratio should not be looked at as an absolute, instead it should be viewed as a baseline barometer for fair value. In other words, the 15 P/E is a good starting point guideline to ensure that you are not overpaying and taking too much risk. Consequently, anytime you come across a moderately growing company (5%-15%), whether a blue-chip or even a moderate to high dividend payer that is trading at a P/E ratio above 15, then caution is called for.

Exceptions to The Rule – Premium Valuations

However, there are certain companies that will always command a premium valuation even when their earnings growth is within the 5 to 15% range. Echo Labs (ECL), Sysco (SYY) and Automatic Data Processing (ADP) are three examples as depicted in the long-term historical FAST Graphs below:

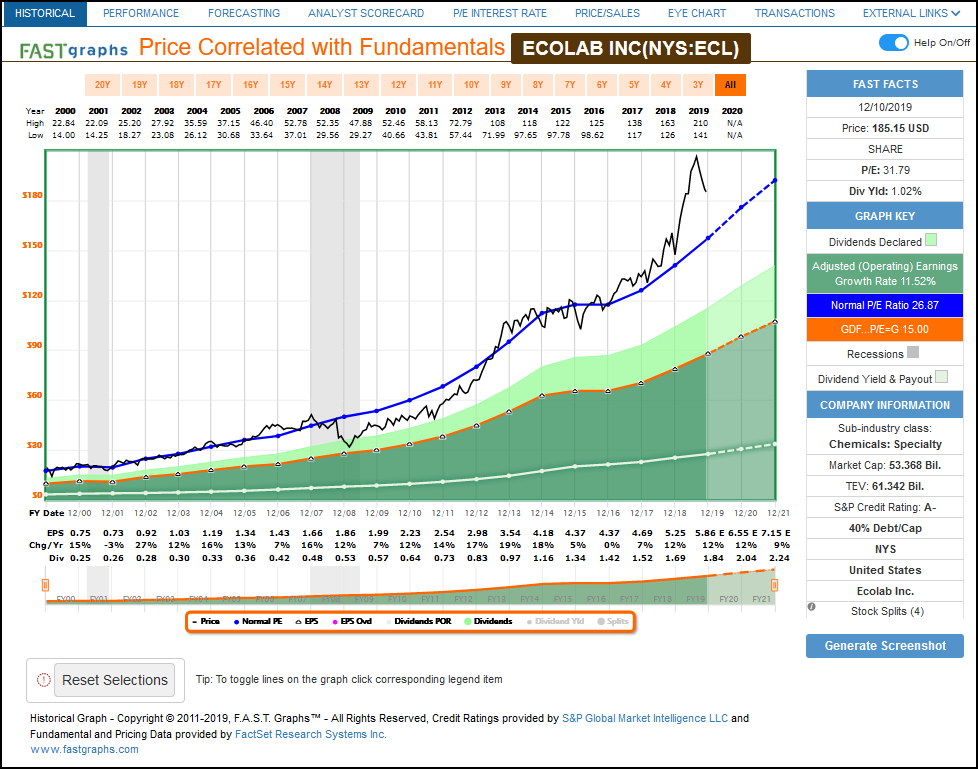

Echo Labs: Historically Valued at a 25-ish P/E Ratio

From the historical earnings and price correlated graph on Echo Labs we see that the market has chronically valued this stock at a P/E ratio in the 25-ish range (The actual P/E of the dark blue line is 26.87). Additionally, note that this stock has never traded at a theoretical fair value P/E ratio of 15 over this entire timeframe. There are exceptions to every rule. The key is to clearly evaluate what you see and accept it as historical reality.

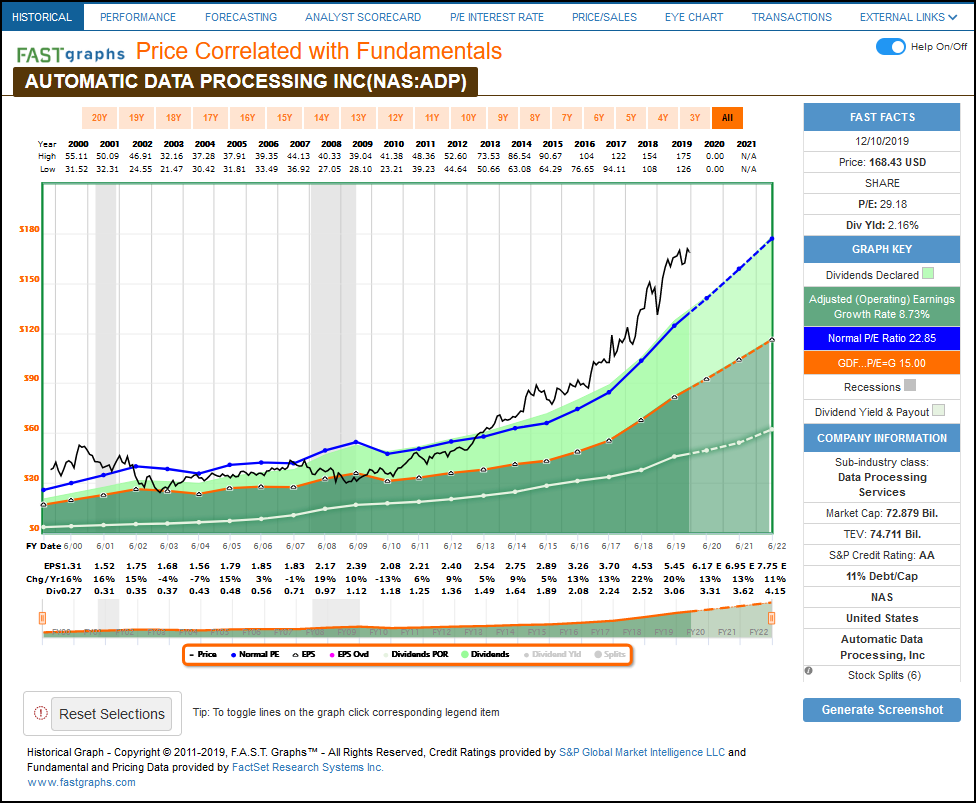

Automatic Data Processing (ADP): Historically Valued at a 20-ish P/E

Once again, we see an example of a company that the market likes to apply a premium earnings valuation to (P/E ratio 20-ish). However, with this example we do see a few occasions where the price did trade at the theoretical fair value P/E ratio of 15. In other words, the price touched the orange P/E ratio 15 line. These rare periods of time when the stock could be purchased at a P/E ratio of 15 or slightly below would be considered optimum for this example.

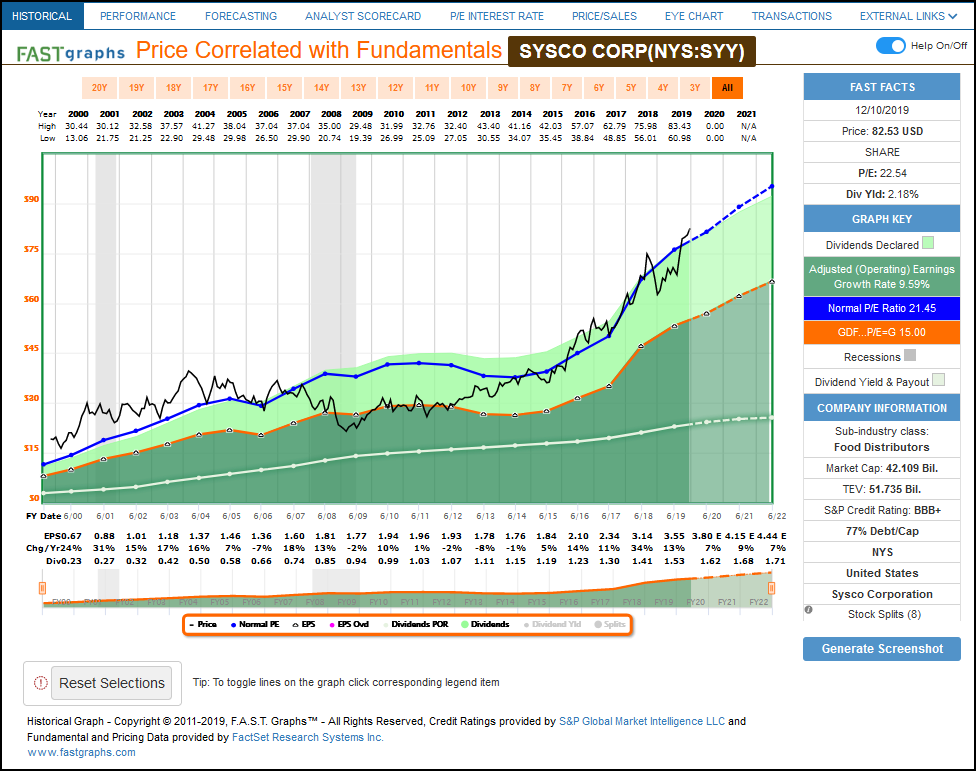

Sysco (SYY): Another Example Of A Premium Valuation

As previously stated, there are exceptions to every rule, Sysco Corp. is one more example. However, in this example, there was a 4-year timeframe (2008 through 2012) where Sysco could have been purchased at a P/E ratio in the 15 range. Therefore, investors had an ample timeframe where they could have purchased Sysco at an optimum valuation with which to invest in this dividend growth stock.

The moral of the story is that the primary determinant of what investors should expect as a reasonable rate of return is the company’s actual growth rate of earnings. To clarify, the assumption is that if a slow to moderate growing stock is bought at a reasonable P/E ratio of 15, in the long run, the investor should expect to achieve capital appreciation that equates to its earnings growth rate. In other words, purchasing a stock at a rational valuation empowers you to participate directly in the company success.

This of course assumes that the P/E ratio at the end of the timeframe being measured is also close to 15. If the ending P/E ratio is higher than 15, then the rate of return the investor achieves will be higher – and vice versa. Also, total returns will additionally include dividends, if any. The bottom line is that investing in a stock at a sound valuation reduces risk and simultaneously provides the opportunity to participate directly in the success of the company.

Principles of Valuation Part3: How to Value a Fast-Growing Business, And How to Think About Stock Prices

Although the 15 P/E ratio as a baseline valuation reference is quite relevant for most companies, it does not apply to all companies. One important deviation is the appropriate valuations that should be applied to growth stocks. As I will discuss later, the venerable Peter Lynch referred to these as “superstocks” and these were also the stocks he favored.

Superstocks: Fair Value Is When P/E Ratio Equals Earnings Growth Rate

Extensive research over many years has led me to conclude that a P/E equal to earnings growth rate (PEG ratio) is more appropriate for companies that grow at faster rates. In Chapter 7 of his best-selling book One Up On Wall Street, the renowned investor Peter Lynch identified six general categories of common stocks: slow growers, stalwarts, fast growers, cyclicals, asset plays and turnarounds. The remainder of this article will focus on the “fast grower” category.

This category of fast grower, Peter Lynch referred to as “superstocks” which he believed deserve the most attention from investors. The reason they deserve the most attention, is because these are the stocks that will generate the highest total returns over the long run. Companies with these attributes are what Peter hunted for when he was seeking his “10 baggers”, because he believed these were the most explosive stocks.

In chapter 13 titled “Some Famous Numbers” Peter Lynch introduced his belief that: “The P/E ratio of any company that’s fairly priced will equal its growth rate.” This statement was the mother of the PEG ratio of 1 representing fair value. However, as I indicated throughout this series, this ratio does not apply to slow to moderate growing businesses. On the other hand, the correlation of P/E ratio equal to earnings growth rate is quite profound when earnings growth is 15% or above. Without going into detail, this is primarily a result of the power of compounding which I discussed in Part 1.

Utilizing FAST Graphs, I will demonstrate how reliably the P/E ratio equal to earnings growth rate (PEG) formula applies to faster growing stocks through real world examples. Also, when dealing with this category of faster growing companies (15% or faster) an accompanying thesis states that a faster growing company is worth more than a slower grower.

In other words, a company growing at 20% a year should logically command a P/E ratio of 20, while a 25% grower should logically command a P/E ratio of 25 and so on. The simple reason for this is because the future stream of income that these fast growers generate will be orders of magnitude (multiples) of what the average company can do. This thesis applies up to a point where very high growth rates are unsustainable, usually growth rates of 30% or above. In other words, there is a limit.

The three fast growers I examine immediately below will provide a look at a range of consistent historical earnings growth of 20% to 30%. In each case notice that the orange earnings justified valuation line will be plotted at a P/E ratio that is equal to its achieved earnings growth rate. The growth rate number will be listed in the dark green color-coded box to the right of the graph. The orange rectangle will list the P/E ratio of the orange line on the graph and the reader should note that it will be equal to the company’s earnings growth rate. The black monthly closing stock price is then overlaid on each graph.

Dividends, if any, are represented by the light green shaded area above the orange earnings justified valuation line. Dividends are paid out of the green shaded earnings area, and are only stacked on top for visual perspective. One benefit this provides is the opportunity to see precisely when dividends are started. Keep in mind that companies that grow at this rate normally do not come with a high dividend yield. Performance graphs will accompany each earnings and price correlated historical FAST Graphs™.

The main point of this analysis is to illustrate how closely the black monthly closing stock price line tracks the orange earnings justified valuation line. This validates the above quote from Peter Lynch’s runaway national bestseller One Up On Wall Street. In Chapter 10, which was titled “Earnings, Earnings, Earnings” Peter also elaborated on the importance of earnings as a valuation reference.

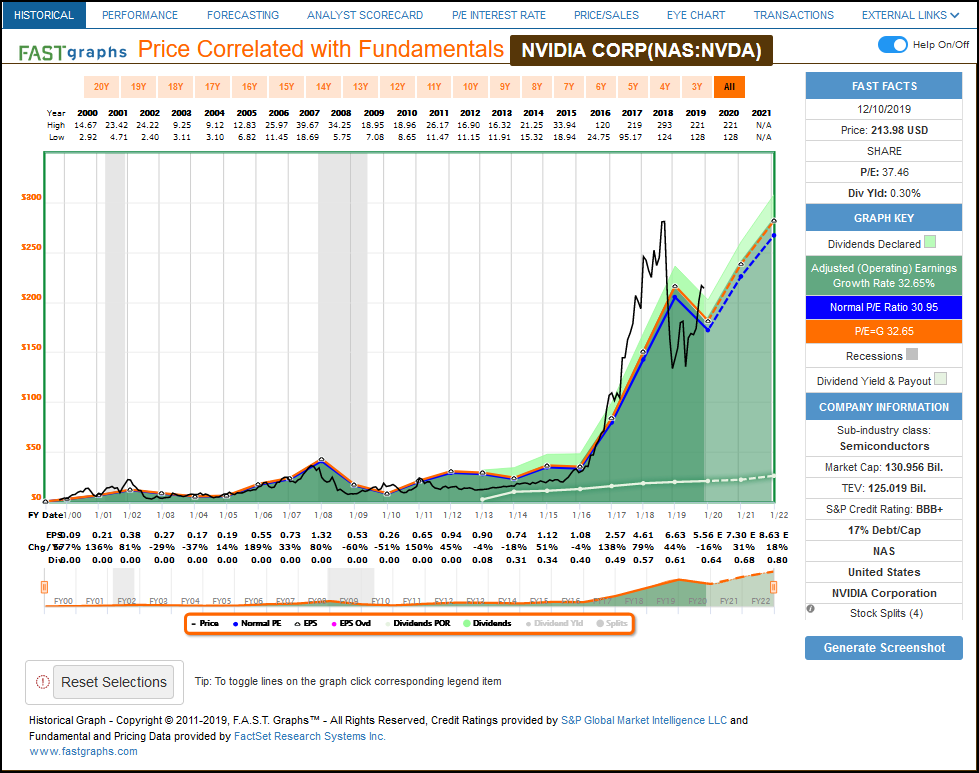

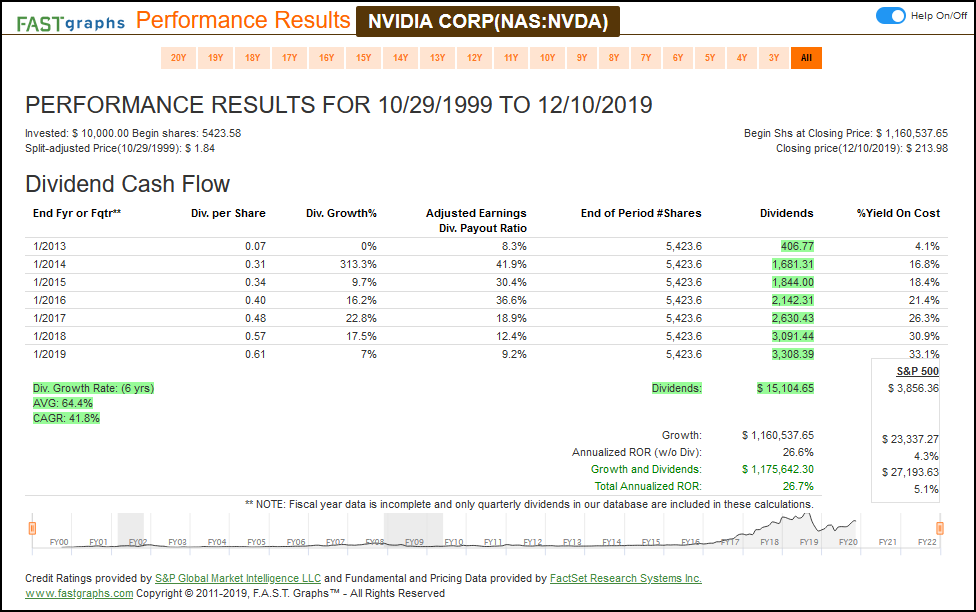

NVIDIA Corp. (NVDA): Superfast Growth Commands High P/E Ratio

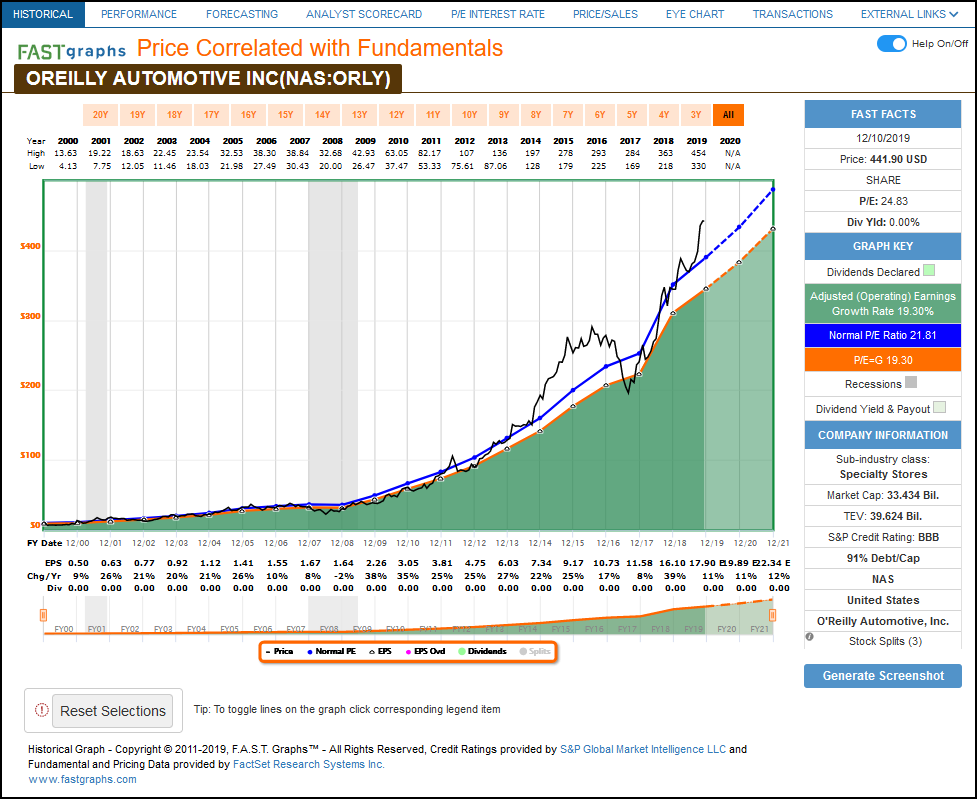

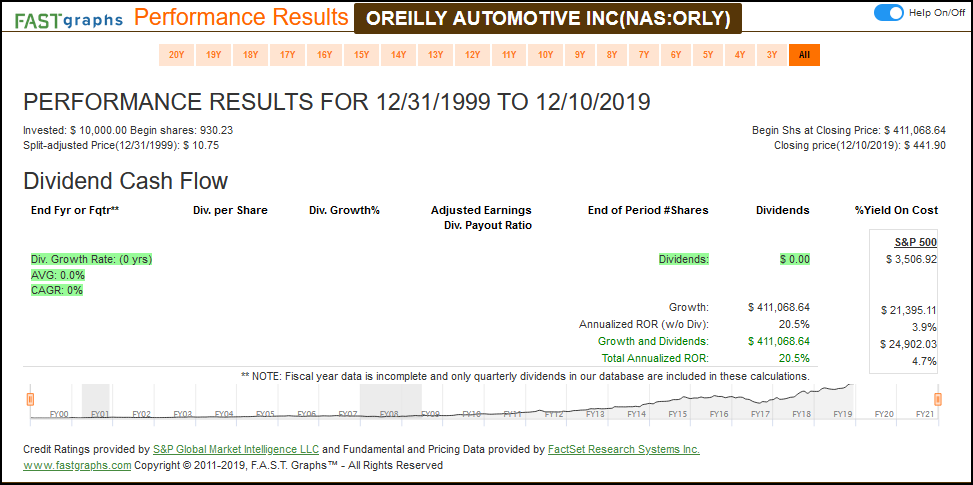

O’Reilly Automotive Inc (ORLY): High Correlation with Price Equal to Earnings Growth

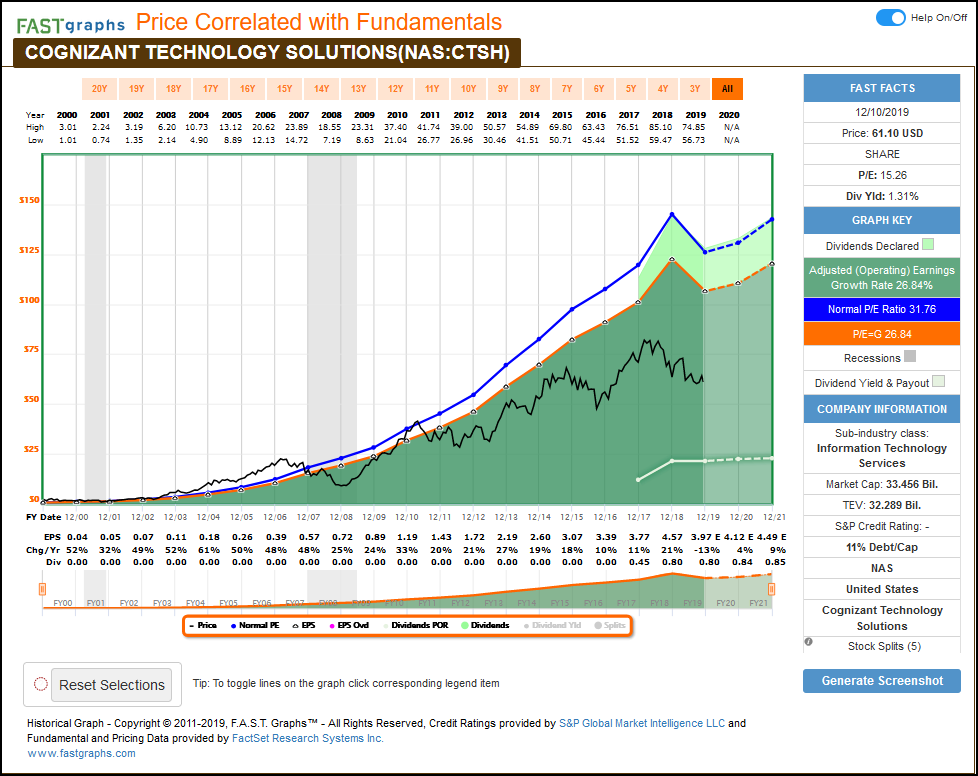

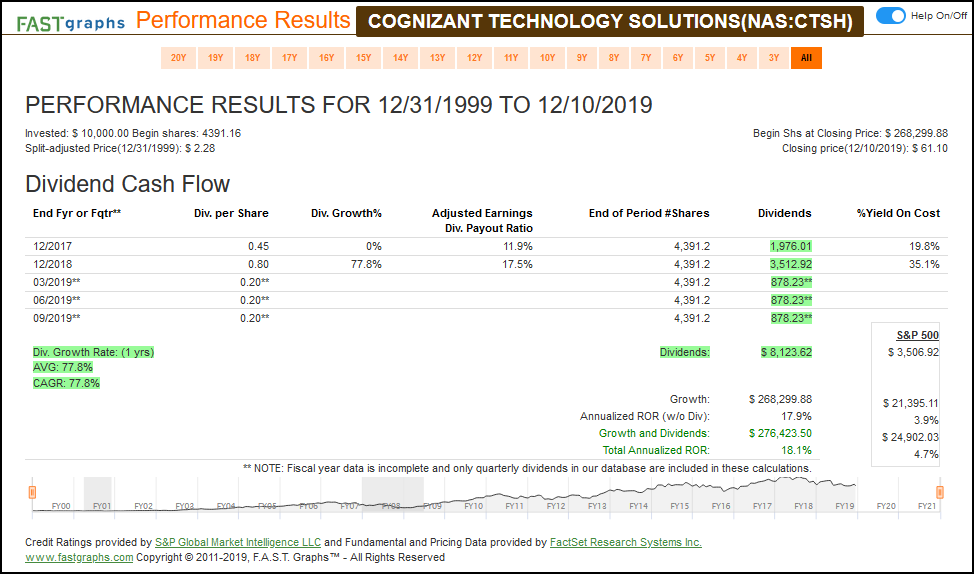

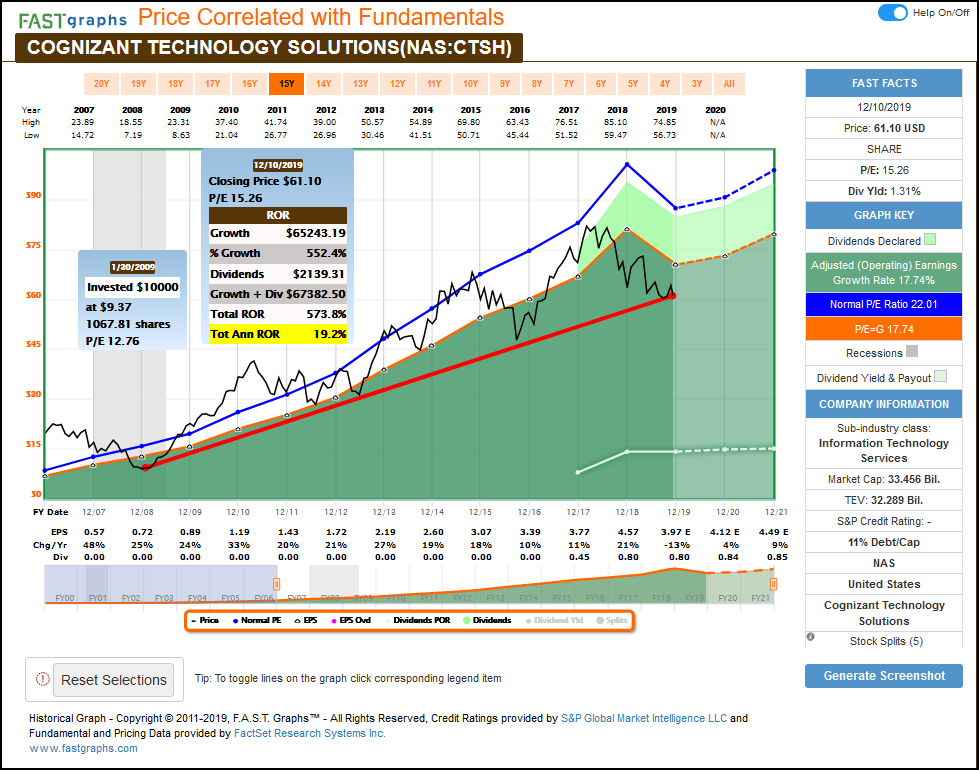

Cognizant Technology Solutions (CTSH): What Happens When Growth Slows?

The reader should note that price has tracked earnings closely since March 2012. However, there is a reason that will be explained below.

When Growth Rates Change So Does Valuation

A company’s earnings growth rate tends to slow down the bigger the company gets. Fair valuation should and does adjust when that occurs.

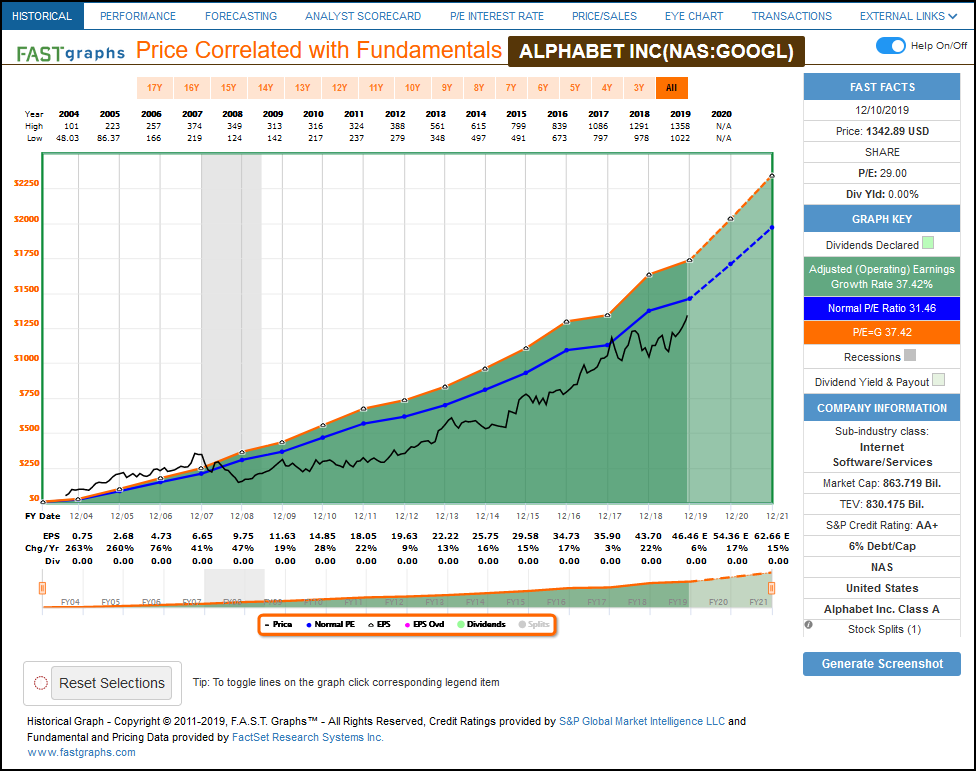

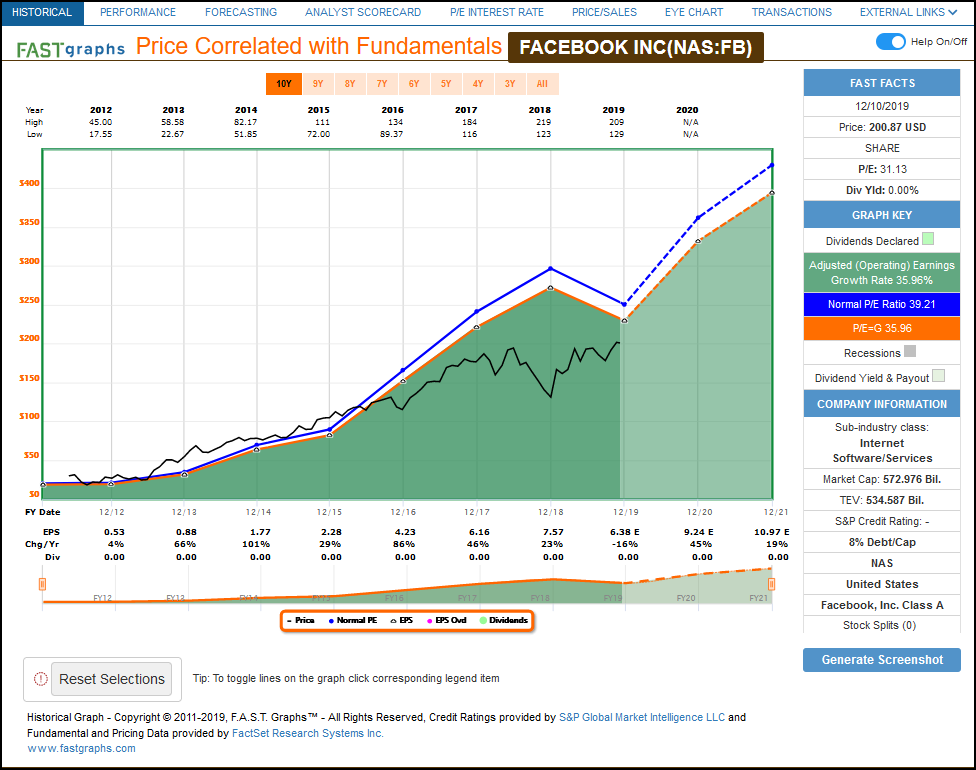

Superfast “Superstocks”

Alphabet Inc (GOOGL)

Facebook (FB)

These Principles Apply To All Metrics Such As Cash Flows, etc.

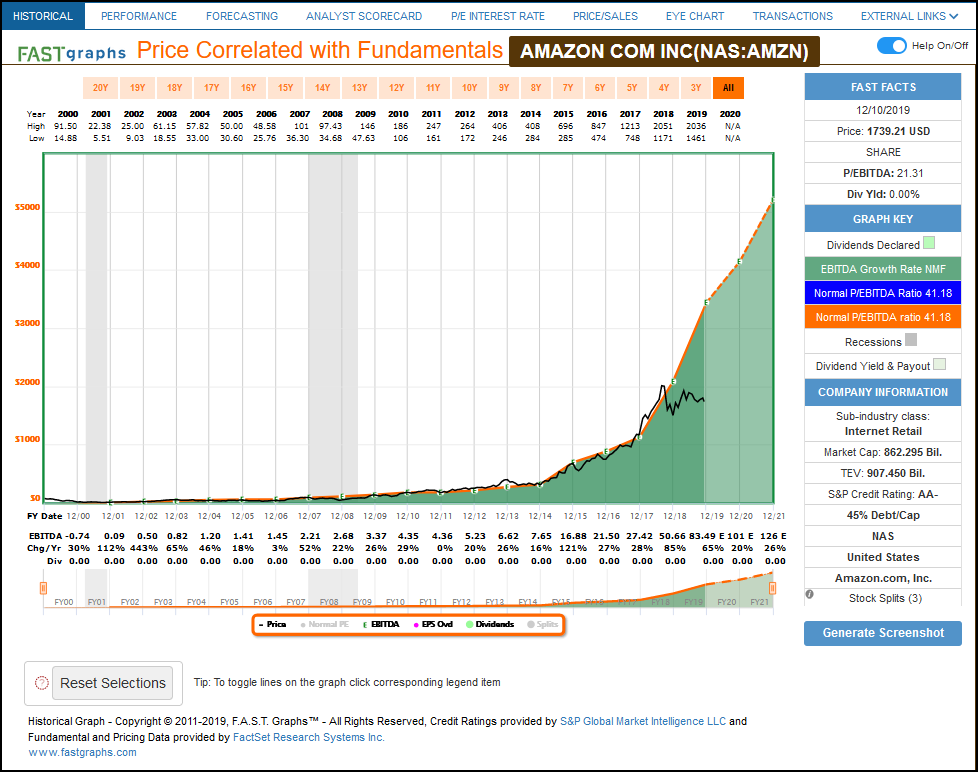

Although everything I’ve written thus far has focused almost exclusively on earnings, it’s important that the reader understands that these principles universally apply to other metrics. There are no better examples that I could show than Amazon’s (AMZN) record based on operating cash flow or EBITDA rather than earnings.

According to Jeff Bezos, Amazon has been willing to eschew earnings in favor of cash flows. Although the market typically values stocks, publicly at least, based on earnings Amazon is the exception. The correlation between Amazon’s stock price and its generation of EBITDA has been uncanny as illustrated below:

Amazon Valued via EBITDA

In the analyze out loud video below I will illustrate how Amazon can also be valued utilizing operating cash flow as a valuation reference. There is more than one way to value a business.

One important consideration that should be highlighted from the above FAST Graphs on these superfast “Superstocks” is how little an effect the general health of the economy or the stock market had on their performance results. Shareholders were rewarded in direct proportion to each company’s operating performance. And, each of these companies’ operating performance was a function of their independent business plans and models.

FAST Graph Analyze Out Loud Video: Revealing the Secret for Valuing Growth Stocks

With this video, I will reveal a very misunderstood aspect of valuation, especially as it applies to high growth stocks. It is so much easier to provide this insight via the video format, so please, don’t miss watching it.

Summary

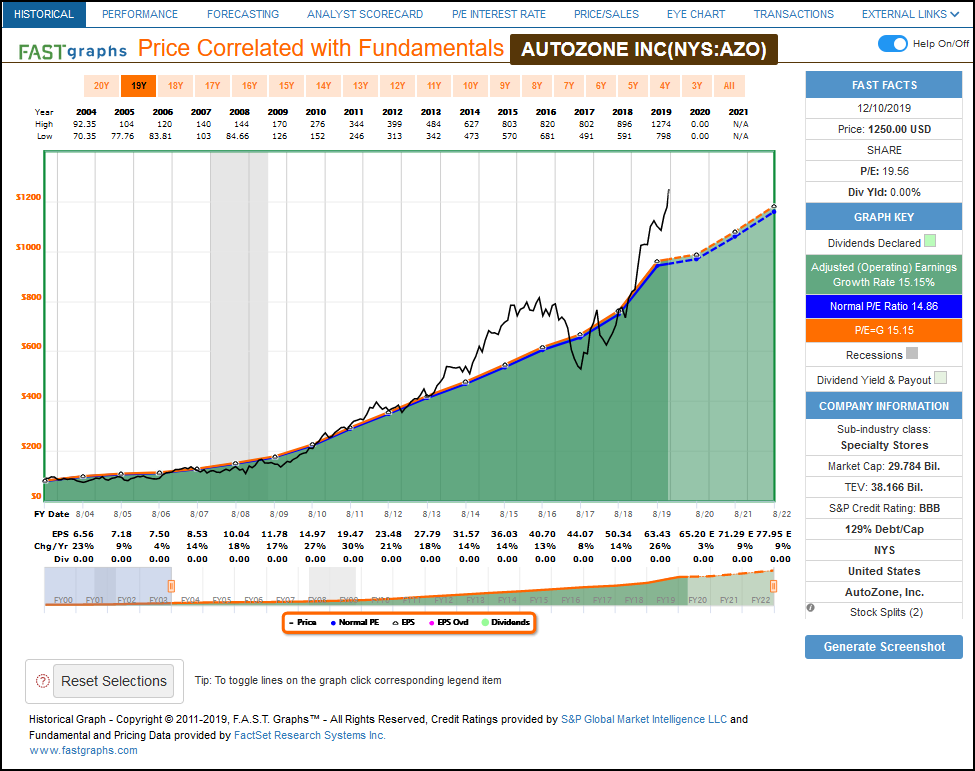

The following graph on AutoZone Inc (AZO) offers me the opportunity to provide a summary of the principles discussed in this series of articles on principles of valuation. AutoZone has historically grown just outside the 15% threshold that my definition of growth stocks suggests. Note that the adjusted operating earnings growth rate has been 15.15%, just slightly above my PE 15 baseline. Therefore, also note that the P/E multiple of the orange line is 15.15, not 15. But most importantly, note how price has closely correlated with and tracked that valuation reference over this timeframe.

Therefore, the reader should further note that these valuation “rules of thumb” are precisely that. In other words, they are not absolutes. Instead, they represent rational ranges of valuation that are prudent and perhaps most importantly apply in the real world over long periods of time. There will be disconnects in the short run, but over the long run stocks will revert to these rational valuation levels based on their growth rate achievements over those timeframes.

Concluding Remarks

From the insights provided by the FAST Graphs above, the relationships between valuation and earnings growth rates should be clear. They also validate the notion that the concept of fair value, or what I like to call true worth, should always be a consideration for investors. Valuation clearly matters, in fact, valuation matters a lot. When stocks are only viewed from the perspective of price alone, the principles behind valuation are easily missed or ignored. This can lead to very expensive investor mistakes.

As Warren Buffett has said: “the fact that people will be full of fear, greed or folly is predictable. The sequence is not predictable.” The relevance of this statement implies accepting and recognizing periods of time when markets are behaving irrationally. There’s no need to attempt to rationalize illogical behavior. That makes no sense, makes no sense. On the other hand, there is a great need to recognize crazy activity when it is occurring. Then and only then, can investors protect themselves from the dangers that exist when irrational exuberance or irrational pessimism rears its ugly head.

My next and final installment in this series on how to know when to buy or sell, or how to value a common stock will focus on how investors can avoid making obvious mistakes. There is no such thing as perfect market timing, but intelligent investing decisions can be made. All it takes is a little common sense and some basic understandings of what gives an investment its value. Investing is rarely a game of perfect, but there is no reason it can’t be intelligent. When it is, appropriate results usually follow.

Disclosure: Long SYY and CTSH

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.