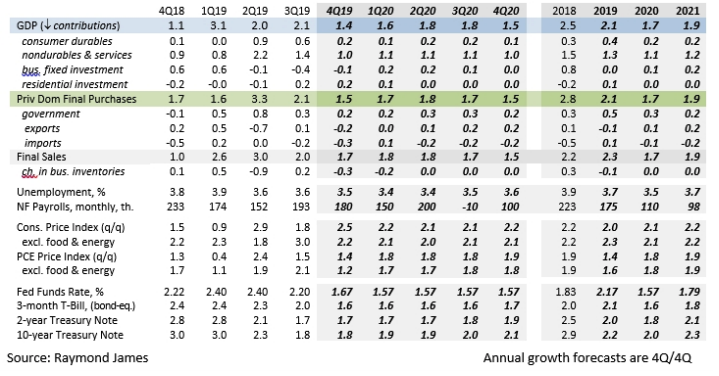

The U.S. economy is expected to expand 1.5-2.0% in 2020. Many of the uncertainties that weighed against business fixed investment in 2019 seem likely to continue into the first half of the year, but the downside risks to the growth outlook appear to be less worrisome than they did in the summer. Consumer spending is likely to grow at a moderate pace, supported by job gains and wage growth, but limited by slower growth in the labor force. Business fixed investment is likely to be mixed and somewhat restrained, but we ought to see some general improvement. Federal Reserve officials have signaled that monetary policy will remain on hold until there is a material change in the economic outlook.

Job growth, while uneven, slowed in 2019, partly reflecting a tighter job market. Firms continue to report difficulties in finding skilled workers. The unemployment rate fell to a 50-year low. Demographic changes (an aging population, slower growth in the working-age population, reduced immigration) imply that the workforce will grow at about 0.5% per year over the next 10 years, slower than in previous decades. Workers are also consumers, so the potential upside on consumer spending growth is likely to be limited (labor force growth of 0.5% plus productivity growth of 1.0-1.5% gets you a potential GDP growth rate of 1.5-2.0%). Despite a low unemployment rate, there is likely some slack remaining in the job market, but it’s unclear how much.

The Bureau of Labor Statistics has estimated that the March 2019 level of nonfarm payrolls will be lowered by about 500,000 in its annual benchmark revision (to be applied February 7). This revision, based on payroll tax receipts, implies that job growth was somewhat slower than reported in 2018.

Over half a million temporary workers will be hired for the 2020 census, boosting payrolls in the spring, but this will fall off in the summer. Given the tight labor market, the Census Bureau may have difficulties in finding enough workers, but many of these positions will be part-time.

Tight labor markets have led to some upward pressure on wages. Over the years, reduced union membership and a greater concentration of large firms have shifted wage bargaining power from workers to businesses. Skilled labor shortages have boosted wage gains for key employees, but firms have also used non-wage incentives to attract and retain workers, including signing bonuses and offering more vacation and other perks. Cost containment remains a key theme for corporate America.

Business fixed investment weakened in 2019. Some of the factors that restrained capital spending in 2019, including a contraction in energy exploration, problems at Boeing, and the General Motors strike, will be behind us in 2020. However, trade policy uncertainty and slow global growth, the two negative factors most often cited across manufacturing industries, may continue. In contrast to consumer confidence, which has remained elevated, business sentiment weakened in 2019.

While a full trade agreement rolling back tariffs appears unlikely, there is hope for a truce in trade tensions between the U.S. and China (that is, an agreement not to escalate). However, there is a danger of a further separation of the world’s two largest economies, and protectionist sentiments have risen around the world. The trade dispute has led to a shift in production away from China to Vietnam, Thailand, Mexico, and other countries.

China has behaved badly, especially in the past. Fifteen years ago, the country actively pushed its currency down, to make its exports more competitive. That’s not the case now (instead, China has intervened to keep the yuan from weakening). Recent trade issues have focused on forced technology transfers and the theft of intellectual property. The U.S. isn’t the only country with concerns. The best approach to deal with that would be through coordinated international pressure. Tariffs raise costs for U.S. consumers and businesses, invite retaliation, disrupt supply chains, and undermine business investment. Moreover, the administration has weakened the World Trade Organization, the arbiter of global trade disputes. While trade disputes take time, the WTO rulings have largely favored the U.S. You don’t bulldoze the house to the ground if you have a plumbing problem – you fix it.

Basic economics tells us that it is misguided to focus on bilateral trade deficits. The U.S. runs an overall trade deficit because we consume more than we produce – or equivalently, we don’t save enough (and remember, the federal budget deficit counts against overall U.S. savings). The current account deficit, the widest measure of trade, is running at about 2.3% of GDP, moderate by historical standards.

Ahead of the 2020 election, there ought to be incentive for President Trump to put trade issues behind him and focus on the economy. However, bashing China (and others) on trade plays to his base, and some of the Democratic contenders have adopted similar anti-China rhetoric.

A simple yield curve model of recession currently suggests about a 25% chance of a downturn within the next 12 months, down from 40% in August, but still a little too high for comfort. The main risk is that the factors that have restrained capital spending will worsen, leading to reduced hiring and increased layoffs, but there are currently few signs of a deterioration in labor market conditions. Consumer debt appears manageable, but business debt has risen significantly, especially for firms with greater credit risk, which could make a downturn worse. Investors should focus on corporate layoff intensions and job offerings, two early indicators of a shift in labor market conditions.

It’s a presidential election year, so political uncertainty will be a factor in 2020. The Democratic platform is expected to center on universal healthcare, climate change, income inequality, tax policy, and antitrust/monopoly regulation – any one of which would have repercussions for certain corners of the financial markets. Over the course of the year, investors may begin to fear change in Washington, which would dampen business investment. However, it’s unlikely that the Democrats will gain a 60-seat super-majority in the Senate, making it extremely difficult to raise taxes or to shift the regulatory environment significantly.

Outside of the U.S., the advanced economies face the same demographic challenges of aging populations and slower growth in workforces. Disruptions from Brexit are a risk. New leadership at both the European Commission and the European Central Bank will seek changes.

Emerging economies were weaker than anticipated in 2019, but are likely to pick up in 2020. These countries face the same demographic challenges as the advanced economies. However, many have made significant strides in education in recent decades and have more room for improvement in living standards. Over the last decade, emerging economies have become increasingly sensitive to changes in U.S. Federal Reserve policy. The Fed’s 2019 rate cuts will help in 2020.

China’s current problems go far beyond trade policy issues – growth has been fueled more by debt in recent years, there’s been a greater reliance on state-owned enterprises, and the Chinese economy appears to be less sensitive to monetary policy stimulus. As growth in China slows (while still very strong by world standards), structural problems will become more challenging.

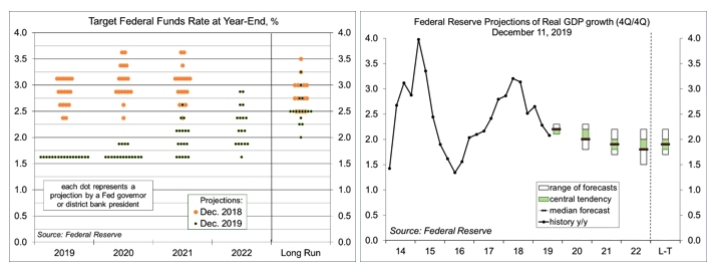

What a difference a year makes. The Fed had raised short-term interest rates in 2018 as part of its policy normalization. A year ago, officials thought that monetary policy was still accommodative and expected one, two, or three further rate increases in 2019. Instead, the Fed lowered the federal funds target rate range three times (to 1.50-1.75%) as it reacted to increased downside risks from trade policy uncertainty and slower global growth. These cuts were viewed largely as insurance against downside risks to economic growth in 2020. Fed officials believe that monetary policy is currently well positioned to support economic growth, a strong labor market, and inflation near 2%. No change in rates is anticipated through 2020, but the Fed will respond if conditions warrant (that is, if we see material change in the economic outlook, such as a deterioration in labor market conditions). The Fed values its independence and its policy decisions will not be influenced by political pressure.

The Fed was unwinding its balance sheet at the start of 2019, but expected to end that in October. In February, the Fed shifted its balance sheet policy framework from a specified size goal to one of maintaining an adequate level of reserves in the banking system. Officials anticipated that the balance sheet would eventually expand in line with that goal. The Fed ended the unwinding of the balance sheet in July, three months early.

In September, a squeeze developed in the repo market. The Fed stated that this was a technical issue. A number of factors boosted the need for cash, and banks appeared unwilling to step in and lend. The central bank followed up with efforts to insure liquidity into early 2020.

U.S. bond yields have been held down by low long-term interest rates abroad. Some increase in U.S. bond yields is likely in 2020, reflecting somewhat higher bond yields outside the U.S., but probably not much, as inflation is expected to remain relatively low. Firms have generally had difficulties in passing along the added costs of tariffs and higher wages. The Phillips Curve, the trade-off between the unemployment rate and inflation, appears to have flattened significantly, largely due to well-anchored inflation expectations. Consumer price inflation, as measured by the deflator for personal consumption expenditures, has consistently been below the Fed’s 2% goal in recent years. That shortfall is a concern for the Fed, as low inflation would reduce inflation expectations, which would in turn lead to lower inflation.

In 2019, the Fed made a comprehensive review of its monetary policy strategies, tools, and communication practices. This review included academic conferences and town hall meetings. Some changes may be announced in 2020, but probably nothing major. One possibility would be a “catch-up” policy, where inflation would be allowed to move above the 2% target for some specified period if it had fallen below 2%. However, comments from officials make this doubtful. The Fed has also been reviewing its strategies for fighting a recession. The Fed normally lowers the federal funds target rate by 500 basis points during a recession. Given the proximity to the effective lower bound (0-0.25%), the central bank should be more aggressive in lowering short-term interest rates, moving sooner and making larger cuts than it would otherwise. Officials have ruled out negative interest rates, but would rely on forward guidance (a conditional commitment to keep short-term interest rates low for an extended period) and further asset purchases (QE) if warranted.

In town hall meetings, Fed Chair Powell was particularly impressed with the comments of those from low-income communities. These communities had been largely bypassed during the economic recovery, but we are now seeing increased opportunities and the benefits of a tight labor market. With inflation below the Fed’s 2% goal, monetary policy is expected to remain accommodative for an extended period.

(M19-2870186)

Notes on the forecast: The table represents a baseline forecast, but incorporates some degree of downside risk. Any forecast will be wrong. Forecasts should be thought of in probabilistic terms – a most likely scenario, but one surrounded by risks. While growth is expected to be moderate in 2020, the risks to the growth outlook remain prominently to the downside. Much hinges on trade policy and there is a general expectations that we will see some positive developments.

GDP growth figures can be quirky from quarter to quarter. Net exports and the change in inventories make up a relatively small portion of the level of GDP, but they account for more than their fair share of volatility in GDP growth. As Fed Chair Powell has put it, net exports and inventories are “components that are generally not reliable indicators of ongoing momentum.” Investors should focus on Private Domestic Final Purchases, which is consumer spending plus business fixed investment plus residential fixed investment (or equivalently, GDP less government less net exports, less the change in inventories). Powell: “The more reliable drivers of growth in the economy are spending on consumption and business investment.”

Underlying domestic demand transitioned to a more sustainable pace in 2019, and a further moderation is anticipated for 2020. While there is likely some slack remaining in the job market, constraints can be expected to limit the pace of job growth.

Trade data are notoriously choppy, making it difficult to discern the impact from trade policy. Trade policy uncertainty appears to have led to some temporal shifts in activity and a stockpiling in inventories, but it’s unclear by how much.

Nonfarm payrolls should be boosted by temporary hiring for the decennial census in the first half of 2020, falling back in the 3Q20.

Once again, long-term interest rates are expected to move somewhat higher, but more gradually than previously. A moderate inflation outlook and low long-term interest rates outside the U.S. should had put downward pressure on U.S. bond yields, but overseas yields have risen from their lows and may edge a bit higher in 2020.

The Fed is on hold for the foreseeable future, but would respond with more rate cuts if there were more significant signs of weakness. The hurdle for a rate increase appears to be high for the time being.

IMPORTANT INVESTOR DISCLOSURES

This material is being provided for informational purposes only. Expressions of opinion are provided as of the date above and subject to change. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Sector investments are companies engaged in business related to a specific sector. They are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Commodities and currencies investing are generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

Links to third-party websites are being provided for informational purposes only. Raymond James is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

This report is provided to clients of Raymond James only for your personal, noncommercial use. Except as expressly authorized by Raymond James, you may not copy, reproduce, transmit, sell, display, distribute, publish, broadcast, circulate, modify, disseminate, or commercially exploit the information contained in this report, in printed, electronic, or any other form, in any manner, without the prior express written consent of Raymond James. You also agree not to use the information provided in this report for any unlawful purpose. This report and its contents are the property of Raymond James and are protected by applicable copyright, trade secret, or other intellectual property laws (of the United States and other countries). United States law, 17 U.S.C. Sec. 501 et seq, provides for civil and criminal penalties for copyright infringement. No copyright claimed in incorporated U.S. government works.

© Raymond James

© Raymond James

Read more commentaries by Raymond James