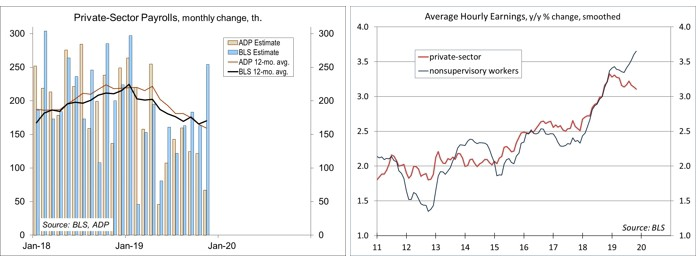

Nonfarm payrolls rose more than expected in the initial estimate for November (+266,000), with upward revisions to the gains for September and October (a net 41,000 higher). In contrast, the ADP estimate of private-sector payrolls rose more modestly (+67,000). What to believe? The unemployment rate has been little changed over the last three months, at around 3.5%. How much slack remains in the job market? The Fed is widely expected to remain on hold this week, but how will the labor market data influence Fed policy in 2020?

As a reminder, the employment report consists of two separate surveys. The establishment survey covers about 142,000 businesses and government agencies, representing about 689,000 individual worksites. Survey responses generate estimates of nonfarm payrolls, hours, and earnings. The household survey, which samples just 60,000 representative households each month, yields estimates of labor force participation and the unemployment rate. There is statistical uncertainty in each of these surveys and seasonal adjustment is often difficult, adding noise to the figures. The monthly change in nonfarm payrolls is reported accurate to ±110,000 and the unemployment rate is reported accurate to ±0.2%. The data are benchmarked once a year – the household survey data in early January, the establishment survey data (incorporating actual payroll tax receipts) in early February. The Bureau of Labor Statistic has indicated that the upcoming benchmark revision will lower the March 2019 level of nonfarm payrolls by about 500,000 (or 0.3%).

In looking at a graph of monthly payroll changes, one can clearly see that they are volatile. One should take any particular month with a grain of salt and focus on the underlying trend. Statistical noise and seasonal adjustment issues will tend to balance out over time. Taking the three- month average reduces the impact of noise, but does not eliminate it. The three-month average for private-sector payroll gains was +200,000 in November, vs. +149,000 for the three months ending in August. Private-sector payrolls averaged a +165,000 gain for the first 11 months of 2019 (vs. +215,000 in 2018 and +172,000 in 2017).

One caveat is that the payroll trend tends to miss at turning points. The BLS uses a birth/death model to account for business creation and destruction. That model does a very good job in normal circumstances, but will mislead at the start and end of a recession. The birth/death model added 274,000 to the unadjusted payroll in October, about the same as a year earlier, which seemed suspicious given anecdotal evidence of softness. The birth/death model was less of a factor in November, subtracting 13,000 (vs. -5,000 a year ago).

Seasonal factors were at work in November, reflecting the start of the holiday shopping season. Unadjusted payrolls rose by 622,000 (vs. +522,000 in November 2018), with most of that in retail and couriers (up 566,000, vs. +587,300 a year ago). Leisure and hospitality added 45,000 jobs on a seasonally adjusted basis, but fell by 200,000 before adjustment.

Click here to enlarge

In a speech given in early October, Fed Chair Powell noted that nonfarm payrolls had significantly underestimated the rate of job losses in the early part of the 2007-2009 recession. Had Fed officials known, they would have taken more aggressive action. Since that time, the Fed has worked with the payroll processing firm ADP to construct a weekly payroll estimate to complement the official BLS figures. Those weekly data are not available publically, but ADP publishes a monthly estimate of private-sector payroll growth, using methodology that is similar to that of the BLS. ADP estimated a 67,000 gain in private-sector payrolls in November, with a three-month average of +104,000 – half of the BLS trend (note that we need a little less than 100,000 job per month to absorb new entrants into the workforce).

Investors tend to dismiss the ADP estimate. It is generally a poor predictor of the monthly change in the BLS figure. However, it ought to be a useful guide in checking exuberance following a sharp upside surprise in the BLS data (as in November). Investors should also keep an eye on the broad range of labor market indicators. The Challenger Job-Cut Report, for example, has shown some moderation in announced corporate layoff announcements in the last three months, following a pickup in the first eight months of the year (still at a low level). Weekly claims for unemployment insurance tend to be volatile from November through February, reflecting difficulties in the seasonal adjustment. The underlying trend was higher in November, but still very low by historical standards.

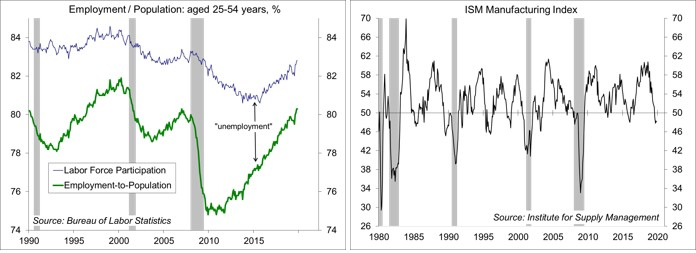

At 3.5%, a 50-year low, the unemployment rate has been essentially unchanged over the last three months, which is a bit at odds with a strong pace of payroll gains. Demographic changes (an aging population, slower growth in the workforce) imply that the unemployment rate ought to trend lower than in previous decades – and we could see it drift down a bit in 2020 without a significant increase in inflation.

Average hourly earnings rose moderately in November (+3.1% y/y), but accelerated for production workers (+3.7% y/y). Anecdotally, firms continue to note a shortage of skilled workers, but at the same time indicate a continued resistance to paying higher salaries (offering signing bonuses for new hires, more vacation, and other perks). There is a relatively wide range of wage increases over time. Some wages rise faster than others. Firms may have to pay up to keep valued employees, but the more moderate gain in overall average hourly earnings suggests that we could be seeing them giving smaller wage increases to support staff. One outcome is that firms ought to invest in improving workers skills.

The Fed has not quite abandoned its belief in the Phillips Curve (the tradeoff between unemployment and inflation). Well-anchored inflation expectations imply that the curve will be flatter than in the past. There is limited evidence that firms are able to pass higher input costs (wages or tariffs) along. Moreover, inflation has remained below the Fed’s 2% goal. So, a tighter labor market and faster wage growth doesn’t mean that the Fed will raise rates anytime soon. (M19-2862030)

Data Recap – Trade policy perceptions continued to drive the stock market. The economic data reports were mixed, with continued weakness in manufacturing, but consistent with moderate growth in the overall economy. The BLS figure on nonfarm payrolls surprised to the upside, but the ADP estimate of private-sector payrolls indicated more moderate job gains.

The November Employment Report was stronger than expected. Nonfarm payrolls rose by 266,000 (partly reflecting the return of 42,000 striking GM workers), with a net revision of 41,000 to the two previous months. Private-sector payrolls rose by 254,000, leaving the three-month average at +200,000. The unemployment rate was essentially unchanged, at 3.5%. Average hourly earnings rose moderately (+3.1% y/y), but accelerated for production workers (+3.7% y/y).

The ADP Estimate of private-sector payrolls rose by 67,000 in the initial estimate for November, a 104,000 average gain over the last three months. “The goods producers still struggled,” according to the report (manufacturing, construction, and mining each fell by 6,000), while “the service providers remained in positive territory driven by healthcare and professional services.” Job growth slowed across all company sizes, but “small companies continued to face more pressure than their larger competitors.”

Click here to enlarge

The ISM Manufacturing Index remained in contraction for the fourth consecutive month in November. The headline figure was little changed at 48.1, vs. 48.3 in October and 47.8 in September. New orders, production, and employment remained below the breakeven level for the fourth consecutive month. Order backlogs were in contraction for the seventh consecutive month (not good). Input price pressures continued to retreat. In their supply managers’ comments, “Global trade remains the most significant cross-industry issue.”

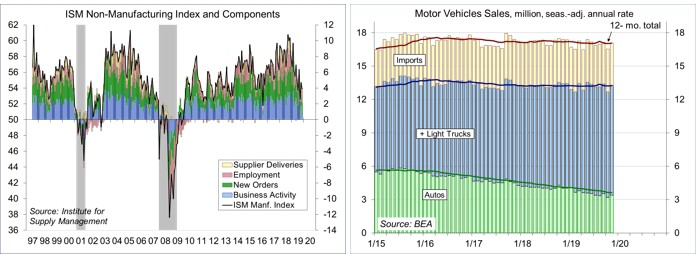

The ISM Non-Manufacturing Index slipped to 53.9 in November, from 54.7 in October and 52.6 in September. Business activity slowed to a modest pace, but new orders and employment growth picked up. Comments from supply managers were mixed. The report was consistent with moderate growth in the overall economy.

Click here to enlarge

Unit Motor Vehicle Sales rebounded to a 17.0 million seasonally adjusted annual rate in November, vs. a 16.5 million pace in October and 17.4 million a year earlier. While there is some month to month variation, vehicle sales have trended flat to slightly lower over the last three years.

The UM Consumer Sentiment Index rose to 99.2 in the mid-December reading, vs. 96.8 in November, at the upper end of the range of the last few years. The report noted that “nearly all of the early December gain was among upper income households, who also reported near record gains in household wealth, largely due to increased stock prices.” There was no sign that the impeachment inquiry (mentioned by just 1% of respondents) had an impact. The sentiment gap between Democrats and Republicans continued to widen (up sharply over the last decade), but sentiment for Independents continued to track the overall index at a “favorable” level.

The Challenger Job-Cut Report showed that announced layoff intentions totaled 44,569 in November, vs. 50,275 in October and 53,073 a year ago (these data are not seasonally adjusted). The total for the first 11 months of 2019 was 13.1% higher than the same period in 2018 (up 36% y/ y in the first eight months of 2019, but down 26% y/y in the last three months).

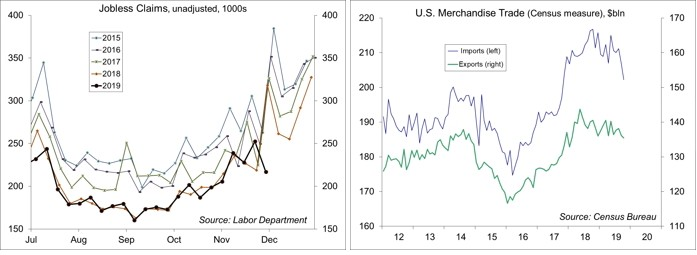

Jobless Claims fell to 203,000 in the week ending November 30. However, adjustments for the Thanksgiving add considerable noise to these data. While still low, the four-week average was higher in November, which will add to the Index of Leading Economic Indicators.

Click here to enlarge

The U.S. Trade Deficit narrowed to $47.2 billion in October, vs. $51.1 billion in September, mostly reflecting a 2.1% drop in merchandise imports. It’s likely that the drop in imports reflects a pullback from stockpiling ahead of expected tariff increases. It’s only one month, but it appears likely that net exports will add to 4Q19 GDP growth (although declining imports are not a sign of strength).

Factory Orders rose 0.3% in October, down 1.2% from a year earlier. Durable goods orders rose 0.5%, revised a bit lower from the previous week, boosted by a 10.7% jump in civilian aircraft orders and an 18.4% increase in orders in defense aircraft. Orders for nondefense capital goods ex- aircraft rose 1.1% partly offsetting the declines of the two previous months.

As expected, the Bank of Canada left short-term interest rates unchanged. The BOC said that future policy decisions “will be guided by the Bank’s continuing assessment of the adverse impact of trade conflicts against the sources of resilience in the Canadian economy – notably consumer spending and housing activity.”

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James