Academics and market watchers alike have long debated the relative merits of active versus passive management. We approach the issue from the perspective of a practical investor, recognizing the need for both management styles. We believe that there are segments of the market where either active or passive management can offer a distinct advantage, but in gold and precious metals mining equities, we favor an active investment strategy.

Market and industry dynamics may give active managers an advantage in gold and precious metals mining equities

Our team’s active approach seeks to benefit from several unique characteristics of the gold and precious metals mining sector. Those characteristics include the operating dynamics of the sector, the volatility of the asset class, and the potential advantages to be gained from fundamental research. The precious metals sector is highly dynamic at the operating level. Miners do not set prices for the metals they produce, the market does. Because miners are price takers, a key driver of their stock price performance is how well they operate their underlying asset base. Doing this well encompasses having high production efficiency plus an ability to find and grow reserves, build and expand mines, and produce metals profitably. We believe companies that can execute on these objectives have a greater chance of delivering outperformance. Active managers have the flexibility to overweight companies that they believe offer the best risk-adjusted opportunities and underweight the companies that they consider to be potential laggards.

Furthermore, gold and precious metals equities are volatile assets, as companies’ stock prices can be subject to wide swings. In illustration of this, the returns on the Philadelphia Gold & Silver Index have had nearly three times the annualized standard deviation of US equities and twice the standard deviation of gold bullion over the past 10 years.1 It is important to note that active managers can adjust position sizes or exit holdings in response to changes in fundamentals, valuations, and corporate actions.

Our fundamental research in the gold and precious metals mining sector addresses both the top-down and bottom-up factors in the metals sector that can influence corporate performance. From a top-down perspective, regional risks are inherent in the sector. Miners are constrained by the opportunities that geology presents them–and that often translates into operating in remote areas of the world where metal deposits are located. Miners are also subject to potential changes in host government regulations, including licensing, taxes, and environmental rules. Additionally, some miners may have a portion of their operations in less stable regions or countries, a circumstance that can create a wider dispersion of potential outcomes. At the company level, miners often face challenges such as securing the equipment, water, electricity, and personnel needed to conduct operations effectively and efficiently. We assess these factors and make informed decisions about the potential risks, favoring regions and companies that appear to be the most promising while avoiding regions and companies that could have negative outcomes.

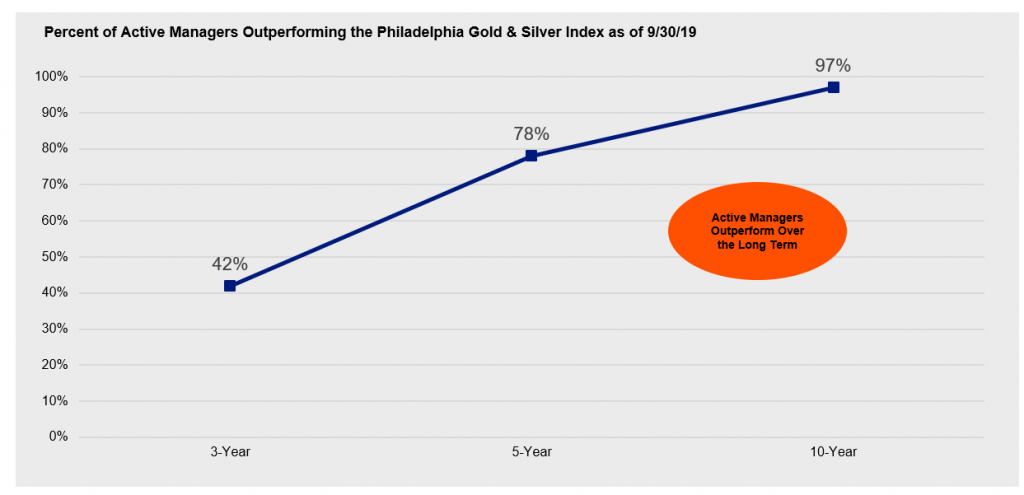

Getting down to brass tacks – the advantage of active managers

The Invesco Listed Real Assets team, which oversees our gold and special minerals strategy, favors an active investment management approach in the mining space. A significant percentage of active managers in the sector have been able to outperform the benchmark for this strategy, the Philadelphia Gold & Silver Index (XAU Index). In this regard, 42% of active managers outperformed the XAU Index over the three-year period ending 9/30/19, 78% outperformed over the last five years, and 97% outperformed over the last 10 years.2

Figure 1: Gold and precious metals mining equities—passive performance

Source: Morningstar, 8/30/19. Gold & Precious Metals Mining Equities are represented by the Philadelphia Gold & Silver Index. Active managers are represented by the Moringstar Equity Precious Metals peer group. Past performance does not guarantee future results. Performance shown is gross of management fees. Net returns will be lower. An investment cannot be made directly in an index.

Implementation of an actively managed investment approach

Invesco Oppenheimer Gold & Special Minerals Fund (OPGSX) provides an actively managed approach to the gold and precious metals mining sector. Portfolio manager Shanquan Li has managed this strategy since 1997, a lengthy tenure that makes him one of the most experienced managers in this space. Shanquan’s investment approach encompasses detailed top-down analysis combined with rigorous bottom-up company research.

As with any comparison, investors should be aware of the material differences between active and passive strategies. Unlike passive strategies, active strategies have the ability to react to market changes and the potential to outperform a stated benchmark. Other differences include, but are not limited to, expenses, management style and liquidity. Investors should consult their financial adviser before investing.

US equities are represented by the S&P 500 Index. An investment cannot be made directly into an index.

The Philadelphia Gold & Silver Index is an index of 30 precious metals mining companies that are traded on the Philadelphia Stock Exchange. Index performance includes total returns. The index is unmanaged, includes the reinvestment of dividends and cannot be purchased directly by investors. Index performance is shown for illustrative purposes only and does not predict or depict the performance of any fund. Past performance does not guarantee future results.

In general, stock values fluctuate, sometimes widely, in response to activities specific to the company as well as general market, economic and political conditions.

Derivatives may be more volatile and less liquid than traditional investments and are subject to market, interest rate, credit, leverage, counterparty and management risks. An investment in a derivative could lose more than the cash amount invested.

Fluctuations in the price of gold and precious metals may affect the profitability of companies in the gold and precious metals sector. Changes in the political or economic conditions of countries where companies in the gold and precious metals sector are located may have a direct effect on the price of gold and precious metals.

The risks of investing in securities of foreign issuers, including emerging market issuers, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Because the Subsidiary is not registered under the Investment Company Act of 1940, as amended (1940 Act), the fund, as the sole investor in the Subsidiary, will not have the protections offered to investors in US registered investment companies.

The fund is non-diversified and may experience greater volatility than a more diversified investment.

The fund is subject to certain other risks. Please see the current prospectus for more information regarding the risks associated with an investment in the Fund.

John Corcoran is a Senior Client Portfolio Manager for the Real Estate and Real Assets team.

Mr. Corcoran joined Invesco when the firm combined with OppenheimerFunds in 2019. Before joining OppenheimerFunds in 2011, Mr. Corcoran was a portfolio manager and senior equity analyst with Noble Partners, a hedge fund where he focused on commodities, energy, precious metals, and other sectors. Prior to joining Noble Partners, Mr. Corcoran was a portfolio manager for Brevan Howard Asset Management, a multi-strategy hedge fund. He has also held senior investment management positions at Fortis Investments, Harbor Capital Management, CIBC World Markets, and Stephens Inc. Mr. Corcoran has been in the asset management industry since 1997, focusing on portfolio management, fundamental research, business development, and product management. Before transitioning to investment management, Mr. Corcoran practiced law at Gibson, Dunn & Crutcher, where he specialized in complex business litigation for Fortune 500 clients.

Mr. Corcoran earned an MBA from Wharton Business School at the University of Pennsylvania, a JD from Boston University, and an AB degree from Harvard College.