One of our least favorite things about investing is the remarkable imprecision of language. There are so many terms like “risk,” “momentum,” “smart beta”, and “asset class” (among many others) that have no precise definition– and yet, everyone assumes they know what those terms mean.

We were thinking about this recurrent complaint while being barraged with articles and narratives about the inevitable coming “recession.” While we don’t want to seem callous, our concern is with the effect of a “recession” on portfolio returns, not the actual economic effects. Assuming the next “recession” is more of the garden variety and not like 2008, what would the impact be on the equity market?

Of course, the term “recession” does have a specific definition. The only problem is that it’s arbitrary, utterly useless to investors, and NOT the one you think it is. 99% of professional investors think the official definition is two consecutive negative quarters of real GDP as established by the National Bureau of Economic Research. Wrong! Here’s the official definition: “The NBER does not define a recession in terms of two consecutive quarters of decline in real GDP. Rather, a recession is a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

This is actually much more sensible than the conventional wisdom. Think about it—What if there were one quarter of negative 10 percent growth, and then a quick rebound? That would sure feel like a recession. How about a year with the following sequence of GDP quarters- -3,+1,-3,+1? No recession there either, but that’s also not going to make anyone happy. Alternatively, you could have a year that was -.1,-.1, +4,+4 that is a recession by conventional wisdom but would be the highest growth rate in recent memory. In fact, the NBER says that the U.S. economy was in recession for 8 months in 2001, and yet there were NOT two consecutive quarters of negative GDP growth.

Regardless of how you define them, recessions are by no means homogeneous and will have radically different effects on both the economy and markets. For instance, the 2001 recession was largely in the bubble sectors of technology and telecom and had very little long-term impact on the economy. On the other hand, the 2008 Great Recession still has aftershocks that we are feeling today.

As usual, we cannot perfectly predict when or what form the next “recession” will take. Interestingly, markets may be sending the signal that they have no idea either. We have had an epic collapse in bond yields, down 40% in the past year on the 10-year Treasury. But stocks have barely corrected, and the real economy seems to be slowing, but holding up. As such, the Fed is cutting rates, but at a very deliberate pace. That has created an inverted yield curve that is very different than what we have seen in the past. Certainly, selling stocks in the face of a recession to lock in a 1.5% return for 10 years in US Treasuries doesn’t seem overly compelling. Yet, many in Germany and Japan would be happy to accept it compared to the 0% or negative rates they can access.

In fact, there is a case to be made that we could see a recession with the 10-year bond yield rising and stocks doing very little or even going up a bit. This would be the opposite of history–but as we have seen, many of the historic relationships between markets seem to be less applicable in an era of very active central banks.

Investors may also be failing to understand the enormous advantages that mega-companies in the S&P 500 have over the average tiny non-publicly traded business in economic downturns. Think about it- if demand drops 5% at your local car dealer, they have no way to offset the overhead of fixed costs other than firing people. They don’t have geographic diversity, generally don’t have cash heavy balance sheets or free cash flow, don’t have access to capital debt markets, and can’t buy back stock when prices drop. Mega-companies have so much more flexibility in every aspect that their earnings are way less affected as they ride through the downturn. Especially in the mega-tech sector [think Google, Microsoft, and Apple for instance,] they generate so much cash that they can take advantage of any opportunities that might arise because of the struggles of others.

In conclusion, we find that good investing requires digging through the vague terms and relationships that get tossed around by the talking heads. We can’t predict economic downturns, but we can understand the differences between them and make intelligent decisions as to how they affect the financial markets.

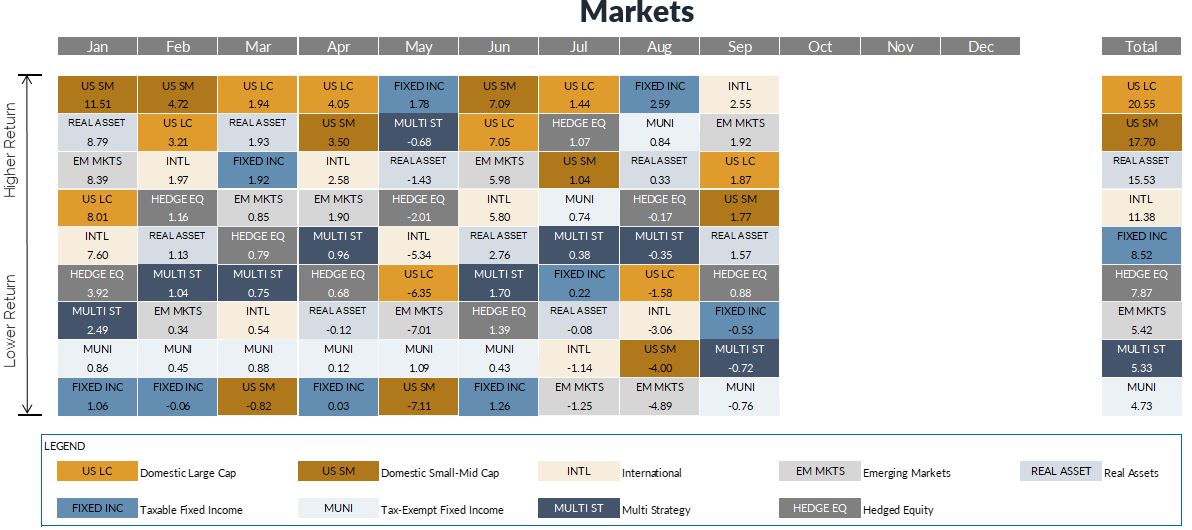

Markets

Despite the unending stream of headlines, markets were little changed in Q3:

- US large cap stocks rose slightly during the quarter, continuing the strong start to the year.

- US small caps and international equity indices were down marginally for the quarter but are also quite positive for the year.

- The winners in Q3 were core bonds, with the Barclays US Aggregate Index rising another 2.3% and the Barclays Municipal Bond 1-12 year index returning +0.8%.

- Falling interest rates and investor hunger for yield remained the theme within fixed income and some other yield-heavy parts of the market including REITs, which rose more than 5% in Q3.

- Alternative investments generally kept up with fixed income in the first half of the year but tended to lag in the third quarter. Strategies with significant exposure to debt (both in the US and abroad) tended to outperform.

A Quick Rundown of the Quarter

- The 25 bps cut in September was well telegraphed, and markets are pricing at least one more cut this year and potentially 1-2 more next year. Fed members, however, are showing a much more mixed outlook, with maybe one more cut presumed in the next 15 months.

- The yield on 10-year US Treasuries fell below that of 2 year in August. This inversion lasted but a week, and the spread has stayed positive in the first few weeks of the fourth quarter. We have previously mentioned that the 10 to 2 spread was one of the more telling gauges in economic parlance, with a better batting average predicting recessions than most economists, but not infallible. The same yield curve trigger is effectively broken overseas, where inversions haven’t mattered over the past decade with interest rates at historic lows.

- Negative yield debt in many sovereigns and some corporates (~$14 trillion worth), are breaking preexisting academic rules. When do you get your money back when you lend at a negative yield? — Never.

- According to the World Bank, services contribution to US GDP outnumber industry 4 to 1. Higher income countries on average are 3:1, while lower income countries are 2:1. Service data is holding up better than manufacturing at this point, helping offset some of the concerns surrounding decelerating manufacturing and trade activity.

© Wealthspire Advisors

More Active Management Topics >