The Power of Top Down: 7 Implications for Em Equity Investors

Welcome to Emerging Markets! A huge array of economies all at various stages of development and maturity with different capital market structures. Add in as many different currencies, political frameworks and policy stances and the result is a complex, diverse, evolving and inefficient market universe.

Therein lies both the opportunity and the challenge. How can an investor harvest such market inefficiency, especially with any degree of consistency? The majority of active managers turn to tried and tested approaches employed in developed markets dominated by stock picking approaches.

However, investors beware. Emerging Markets are more dynamic and volatile compared to developed markets with a different balance of price and volatility drivers. While stock research and selection is key, so are a number of other factors, not least country, industry and currency. Indeed, Emerging Markets’ underlying characteristics mean that these so called ‘Top Down’ factors can be disproportionately important in driving prices and hence the alpha opportunity.

We consider seven implications that illustrate why explicitly incorporating a Top Down approach is both a return enhancer and a risk mitigator.

1. The opportunity

Emerging Markets are already a strategic investment in global asset allocations and their importance will only increase over time. They currently account for 74% of global GDP growth (based purchasing power parity adjusted exchange rates) and their stock markets continue to liberalise, broaden and deepen to reflect their economic growth drivers. They represent 40% of global economic activity based on the origination of listed companies’ revenues. They comprise 20% of global total market capitalisation and 12% based on a free float adjusted figure. See Ashmore Emerging View: ‘The EM equity universe: 7 implications of evolution’ for more information on the market universe.

Emerging Markets’ underlying characteristics and how they are traded mean they are highly inefficient. That is, their price movements frequently do not reflect underlying fundamentals. Consequently, they offer the potential for significant alpha generation, much more so than in developed markets. The magnitude of inefficiency and therefore opportunity, is evident when one compares the performance of active managers with common indices and passive ETFs. The latter two are typically towards the bottom quartile of the peer group. The same analysis for more stable developed markets points to the opposite. The S&P 500 is typically towards the top quartile compared to the US All Cap manager universe reflecting the limited alpha opportunity.

Fig 1: EM competitor percentile rank

Source: eVestment, 31 December 2018

Fig 2: US competitor peer group rank

Source: eVestment, 31 December 2018.

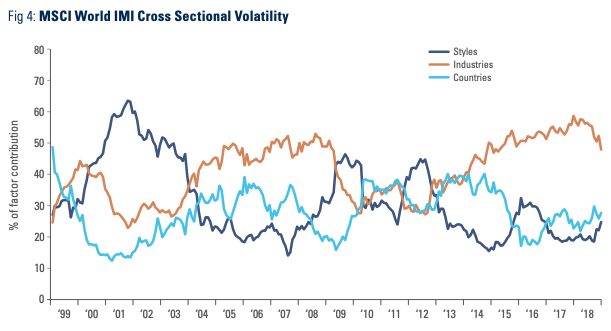

To benefit from this inefficiency and also to navigate the associated challenges, one needs to acknowledge and understand the underlying price drivers at work in Emerging Markets. Country is the single largest explanatory factor of cross sectional volatility, a common metric for the potential to add value from active portfolio management. Industry is increasing in importance, while style has limited explanatory power on a consistent basis. This is in contrast to developed markets where country is typically the weakest driver.

Fig 3: MSCI EM IMI Cross Sectional Volatility

Fig 4: MSCI World IMI Cross Sectional Volatility

Source: MSCI 2019. Cross sectional volatility is the standard deviation of returns across stocks in a universe.

TAKEAWAY 1: THE OPPORTUNITY

Emerging Markets are inefficient and Top Down factors play a disproportionately important explanatory role.

2. Significant diversity

Why are Top Down factors so important in driving market returns and volatility? Part of the answer is diversity. Emerging Markets comprise somewhere between c. 80 and 25 countries, based on Ashmore’s or MSCI Emerging Market’s definition. Each country is characterised by different stages of development, balance of economic drivers and institutional, political and capital market structures.

This heterogeneity is apparent when looking at country ranks in global development indices. In some cases, they have evolved to the point they match, and sometimes surpass, significant developed markets. In other cases, they have yet to reform and implement practices that meet international standards.

Fig 5:

Source: World Economic Forum: The Global Competitiveness Report 2018, The World Bank: Doing Business 2018 and Transparency International: Corruption Perception Index 2018.

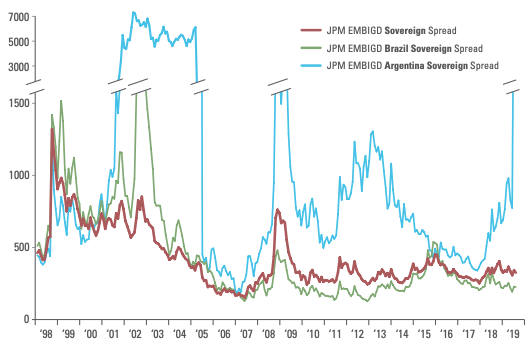

The contrasting standards of Emerging Markets institutional rigour and governance are also reflected in their risk premia. By looking at US Dollar sovereign country spreads versus US treasury bonds as a simplified risk premia, one will note the marked reduction since the early normalisation years of Emerging Markets in the late 1990s. The J.P. Morgan EMBI Global Diversified Sovereign spread has reduced from over 1,400 basis points to around 300 basis points. However, risk premia are still highly divergent among different countries. Brazil and Argentina, for example, had similar Sovereign spreads in the late 1990s yet have seen since meaningful dispersion, aside from a brief period in 2016 when all three spreads aligned, albeit briefly.

Fig 6: Emerging Markets risk premia

Source: Bloomberg.

Economic growth models can also be highly differentiated. Some countries boast world leading technological expertise. Others have a well-trained labour force and/or highly efficient logistic networks and/or abundant high grade mineral resources.

Commodities has notably diminished in importance from a stock market perspective with Materials and Energy sectors halving in index size from 31% in 2011 to 15% today. However, Emerging Markets still comprise some of the world’s largest commodity exporters, for example Russia and Chile, as well as the largest importers, for example South Korea and Thailand. The type of commodity traded also brings its own idiosyncrasies.

This means the impact of commodity price volatility on countries’ balance of payments, economic growth, currency and stock market performance can vary significantly.

TAKEAWAY 2: SIGNIFICANT DIVERSITY

Emerging Markets comprise countries with highly divergent standards of governance, economic growth models and stock market composition. The outcome is significant diversity.

3. Emerging Markets are widely held yet still misunderstood

Emerging Markets are widely held reflecting their strategic role in global asset allocations. Consequently, there is greater information and coverage of their securities. Indeed, in some cases they have more sell side analyst coverage than their developed market peers, for example Alibaba with 65 compared to Amazon with 61. However, counterintuitively, this can exaggerate the volatility of the stock’s price and liquidity. Investor behaviour can diverge based on the country of listing and the perceived characteristics of the industry they are in, among other market factors.

Developed market events can also have a disproportionate and asymmetric impact. To illustrate this, highlighted below are the five largest Emerging Markets drawdowns since the year 2000. In every case, the catalyst has originated from developed markets yet Emerging Markets have underperformed.

Fig 7:

Source: Bloomberg. Financial Crisis: 30/05/08-28/11/08. Eurozone crisis: 29/04/11-30/09/11. Fed hike: 30/04/15-30/09/15. Subprime crisis: 31/12/07-31/01/08. Eurozone debt crisis: 29/02/12-31/05/12.

The behavioural bias for global investors to sell Emerging Markets at times of market stress relates to information asymmetry, a legacy of perceived ‘riskiness’ and the structure of global finance. The result is that Emerging Markets can suffer excessive price volatility relative to underlying risk. This can often serve as an excellent time to invest.

Emerging Markets’ ‘riskiness’, defined as permanent loss of capital, is considerably lower than often perceived. Their economies are, generally speaking, in balance, inflation is low, floating exchange rates are prevalent, central bank independence is typically established and governments and companies can fund themselves in the local currency. This last point was the focus of an Ashmore Emerging View: The case for EM local currency debt. Emerging Markets remain prone to abrupt changes in global liquidity conditions given they only account for 23% of global finance. This said, now 82% of their funding is domestic, the risk of capital flight triggering economic crisis, as was the case during the 1990s, is far more remote. The few exceptions that currently remain are those countries that have not yet established a permanent source of domestic funding, for example Argentina and Turkey.

Should investors buy every dip then? No. Emerging Markets are at an earlier stage of institutional development so drawdowns require careful assessment and selectivity is key. Moreover, investors should be aware that liquidity is pro cyclical in Emerging Markets. An abrupt change in the macroeconomic backdrop, or policy stance, can have a meaningful impact on liquidity conditions.

TAKEAWAY 3: EMERGING MARKETS ARE WIDELY HELD YET STILL MISUNDERSTOOD

Emerging Markets are still misunderstood and consequently suffer disproportionate market volatility from non-fundamental drivers creating investment opportunity.

4. The importance of currency

For US dollar investors especially, currency can often be a key price and volatility variable. However, investment approaches often overlook or disregard FX. Worse still, currency views are sometimes incorporated into investment theses based on consensus expectations for a normalised forward curve. For some investors, currencies are too volatile to assess or their fundamental drivers are too complex to rationalise. One would beg to differ.

There is a well-founded and credible view that Emerging Markets increased importance to the world, from an economic growth and global capital flows perspective, should lead their currencies to strengthen over time. In these circumstances, currency is then a positive factor and value accretive. This makes some sense, all else equal.

Fig 8: MSCI Emerging Markets indices

Source: Bloomberg, MSCI.

Nevertheless, this is not supported by aggregate market returns as reflected by MSCI indices. Since 2001, the MSCI Emerging Markets in local currency has outperformed the standard US dollar denominated index. This implies that currencies have weakened compared to the dollar and have been a headwind for returns. Both indices have outperformed the US dollar hedged index.

This is an oversimplification and it raises several important points. Understanding the fundamental drivers behind a currency move, its potential magnitude and longevity, are all useful insights. They enable proactive risk management by reducing or avoiding exposure ahead of currency weakness. Currency views can also help to model and build out sensitivities and scenarios for countries, industries and stocks. The impact of currency on different industries and stocks has also become more nuanced as Emerging Markets have evolved. A weakening currency can be a tailwind for certain industries or corporates. Consequently, selectivity is clearly important, as not all currencies will appreciate over time compared to the US dollar, as the table above demonstrated.

The very best intended stock thesis and earnings forecasts are at risk from currency volatility. Take Turkey in 2016, for example. Policy orthodoxy deteriorated, inflation expectations rose and the Turkish lira sharply weakened compared to the US dollar. This turned optically low stock valuations and resilient corporate earnings growth into a mirage since they were more than offset by currency depreciation.

As shown below, periods of elevated currency volatility are not unusual in Emerging Markets. Consequently, building an understanding for a currency’s drivers can be an important return enhancer as well as risk mitigator.

Fig 9: Emerging Markets currency % spot price change

Source: Ashmore, Bloomberg. MSCI Emerging Markets country indices returns in $TR.

Currencies are correlated with macroeconomic and financial conditions in the form of nominal and real export growth, commodity prices and the trade-weighted US dollar. While a hedged strategy may reduce currency volatility, it is too blunt an instrument to deal with the inherently dynamic and complex universe of Emerging Markets. It also comes with a cost, which in some cases is still high. As shown in Figure 8, the cost of hedging is 300 basis points annualised, the difference between the performance of the US dollar hedged index and the local currency equivalent index.

TAKEAWAY 4: THE IMPORTANCE OF CURRENCY

In Emerging Markets disregard currency at your peril.

5. Significant dispersion

The outcome of all the points made so far is significant dispersion of market returns. Therein lies both the investment opportunity and the challenge. See below the magnitude of dispersion and country divergence over time.

Fig 10: Dispersion of Emerging Markets country index USD returns

Source: Bloomberg, as at 31 December 2018. MSCI EM Index calendar year country market returns (USD).

Fig 11: Emerging Markets country index USD returns

Source: Ashmore, Bloomberg. MSCI Emerging Markets country indices returns in $TR.

There are several lessons one can draw:

1. Emerging Markets should not be treated as homogenous:

Returns are highly divergent between countries during the same period and across periods

2. Subdividing Emerging Markets into regions has limited investment justification:

Countries in the same region typically have little in common, as is reflected in their divergent returns.

3. China is important, yet not necessarily always an attractive investment:

Volatile Chinese market performance underscores why exposure should be treated opportunistically, the same as for all Emerging Markets

4. Investment diversity is key, however attractive a country is perceived:

Returns for the same country are highly divergent from one period to the next

5. Emerging Markets have evolved and are more stable:

While performance dispersion will remain elevated for structural reasons, dispersion is unlikely to return to the highs of the 1990s

6. The universe of Emerging Markets is dynamic:

The market universe continues to evolve reflected here by reclassifications made to the index in white.

7. Country ‘cycles’ and inflection points are key triggers for stock market returns:

For example, Brazil – from commodity boom (2003-2007), when market returns were strong, to policy stagnation (2011-2015) when returns were weak, to improved policy orthodoxy (2016 onwards?).

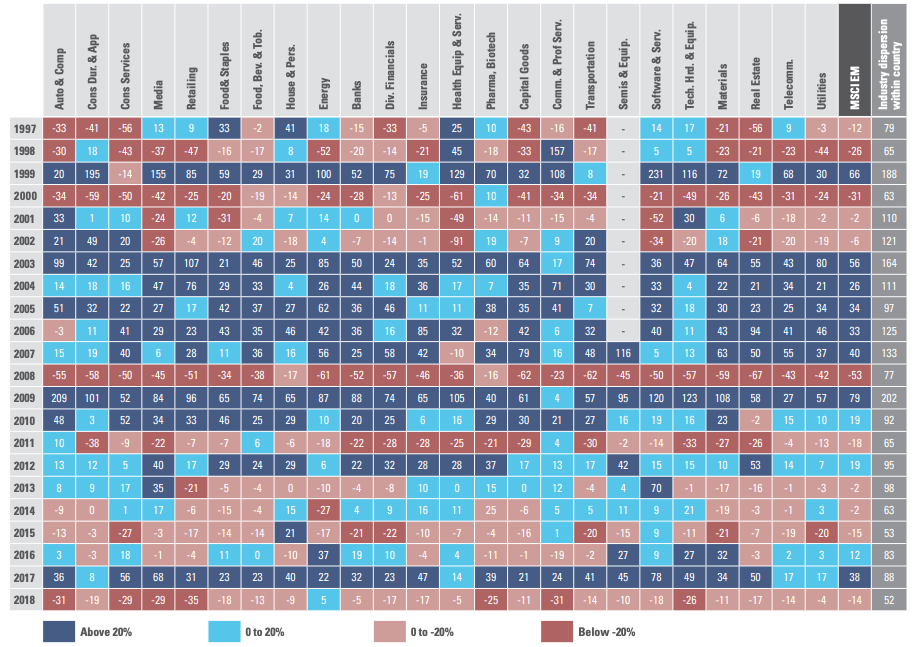

Enhanced institutionalisation across Emerging Markets over time has garnered increased investor confidence. In turn, this has led their stock markets to broaden, deepen and better represent industry drivers. Some industry groups are more domestic in orientation while others are more sensitive to global drivers. High dispersion of returns among industry groups, including within the same country - see the last column, also provides an investment opportunity.

Fig 12: Emerging Markets industry index USD returns

Source: Ashmore, Bloomberg. MSCI respective industry index. Returns in $TR price. Median differential between the best and worst performing industry groups for the largest 10 countries in the MSCI EM index (as at 31 December 2017) on an annual basis. The median differential from 1997 – 2000 reflects MSCI EM sector dispersion as industry data is unavailable.

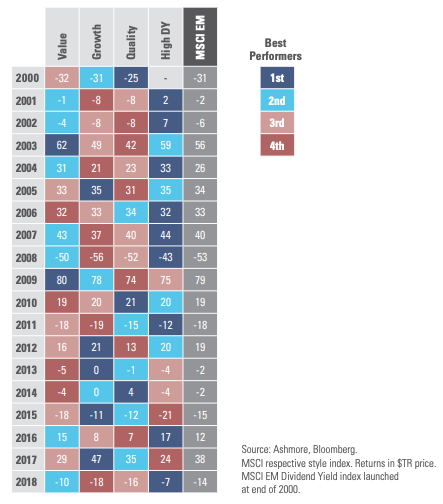

Emerging Markets’ dynamism and volatility tend to mean Top Down drivers are too powerful and overwhelm style factors. This reduces the explanatory power of style on price returns at least on a consistent basis. As can be seen below, the winning style factors interchange frequently.

Fig 13: Emerging Markets style indices USD returns & performance rank

Source: Ashmore, Bloomberg.

MSCI respective style index. Returns in $TR price.

MSCI EM Dividend Yield index launched at end of 2000.

TAKEAWAY 5: SIGNIFICANT DISPERSION

Emerging Markets structural and behavioural inefficiencies manifest themselves in significant market dispersion and hence investment opportunity.

6. Top Down research

A great deal of Emerging Markets’ price action and volatility can be attributable to Top Down drivers. This begs the question how can one analyse and translate this into alpha, especially on a systematic basis?

Some of the most valuable insights are those generated on a rolling basis. This enables one to build a trajectory for an economic cycle, its rate of change and likely inflection points. It trumps a point in time assessment, for example quarterly reviews, given they risk only explaining the past rather than the future.

Similarly, the most insightful data to assess is forward looking, in combination with more commonly referenced macroeconomic data, albeit this can be subject to revision. For example, an assessment of policy stance, the business cycle and market implications can all help inform the direction of data and help one to build conviction.

Insights need to be understood in the context of the equity market, which can be quite different compared to other parts of the capital structure. Moreover, assessment should not stop at single country views. As highlighted earlier, Emerging Markets have evolved leading to different ramifications for different industries within the same country or indeed global industries.

The most important driver of Emerging Market’s absolute returns is earnings. Consequently, it is through an assessment of market earnings expectations that one can determine what is already ‘priced in’. This trumps an assessment based on market valuation.

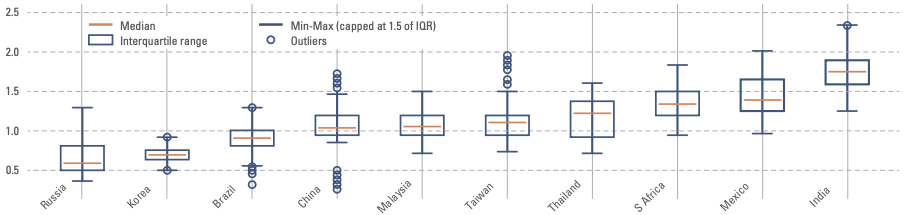

Some markets are structurally lower or more richly valued. A valuation focus can risk a bias towards momentum investing which can be prone to macro shocks. Valuations are not necessarily normally distributed nor mean reverting. Simply put, emerging countries are still too unstable for valuation to systematically add value. This is reflected in the chart below.

Fig 14: Valuation analysis – MSCI Emerging Markets price-to-book

Source: MSCI. Period: 31 December 1998 to 31 January 2019.

Both Top Down and stock conviction should be integrated to ensure Top Down conviction is not misplaced or offset by idiosyncratic stock drivers. Stock due diligence and stock selection remain key. After all, the final outcome is a portfolio of stocks.

TAKEAWAY 6: TOP DOWN RESEARCH

Emerging Markets heterogeneity mean that different drivers at different points influence different market nodes with differing outcomes.

7. Manager diversification

Active equity managers who explicitly incorporate Top Down in their investment approach are in the minority. To be consistently effective it requires an in depth understanding of structural inefficiencies, as well as behavioural biases, to exploit them systematically. This requires specialist experience, a strong network of contacts, global resources and a willingness to employ a tailored approach.

The rewards, however, can be significant. Through building top down conviction, investors can stay alert to areas of the market that are conducive to an improving operating environment and hence improving earnings potential for corporates. Conversely, a deteriorating backdrop can enable an investor to take precautionary action pro-actively and act as an amber alert for companies that could be more vulnerable to that scenario.

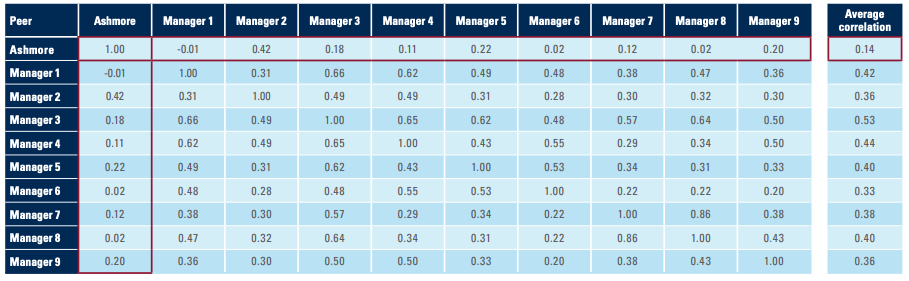

Finally, by combining a truly Top Down driven approach with other managers can serve as a powerful diversification tool. This is evident by a notably low correlation of performance returns compared to the peer group, at least based on Ashmore’s experience.

Fig 15: Five years excess return correlation for best performing managers

Source: eVestment as at 30 June 2019. The peer group is defined as the nine best performing GEM Equity managers in eVestment’s Global Emerging Markets All Cap Peer Group. Based on excess returns over MSCI EM (Net) Index.

TAKEAWAY 7: MANAGER DIVERSIFICATION

By explicitly incorporating Top Down in an investment approach, a manager can potentially enhance return, mitigate risk and be a manager diversification tool.

No part of this article may be reproduced in any form, or referred to in any other publication, without the written permission of Ashmore Investment Management Limited © 2019.

Important information: This document is issued by Ashmore Investment Management Limited (‘Ashmore’) which is authorised and regulated by the UK Financial Conduct Authority and which is also, registered under the U.S. Investment Advisors Act. The information and any opinions contained in this document have been compiled in good faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Save to the extent (if any) that exclusion of liability is prohibited by any applicable law or regulation, Ashmore and its respective officers, employees, representatives and agents expressly advise that they shall not be liable in any respect whatsoever for any loss or damage, whether direct, indirect, consequential or otherwise however arising (whether in negligence or otherwise) out of or in connection with the contents of or any omissions from this document. This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any Fund referred to in this document. The value of any investment in any such Fund may fall as well as rise and investors may not get back the amount originally invested. Past performance is not a reliable indicator of future results. All prospective investors must obtain a copy of the final Scheme Particulars or (if applicable) other offering document relating to the relevant Fund prior to making any decision to invest in any such Fund. This document does not constitute and may not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment in any such Fund. Funds are distributed in the United States by Ashmore Investment Management (US) Corporation, a registered broker-dealer and member of FINRA and SIPC.