Economic Brief - A Field Guide to Recessions (updated)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDefinitions and Determinations:

The National Bureau of Economic Research (NBER) defines a recession as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.” It is not “two consecutive quarterly declines in real Gross Domestic Product (GDP),” often cited as the “textbook” definition. A recession begins as the level of economic activity reaches its peak (and starts to decline). The recession ends when the economy begins to grow again.

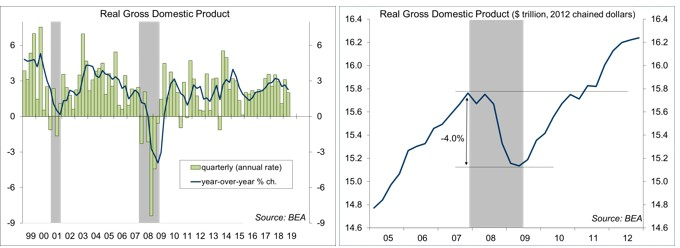

The NBER’s Business Cycle Data Committee, made up of ten well-respected academic macroeconomists, declares starting and ending dates for recessions. The committee’s job is to be definitive, not timely, and it may be a year or more (allowing for revisions to the economic data) before an official pronouncement is made. For example, the start of the 2007-2009 recession, which ran from December 2007 to June 2009, was not declared until December 2008, while the ending date was declared in September 2010, more than a year after the recession had ended. In the most recent recession, real GDP fell 4.0% from top to bottom, and did not exceed the previous peak until 2Q11.

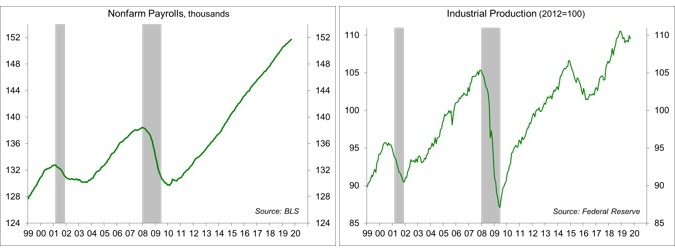

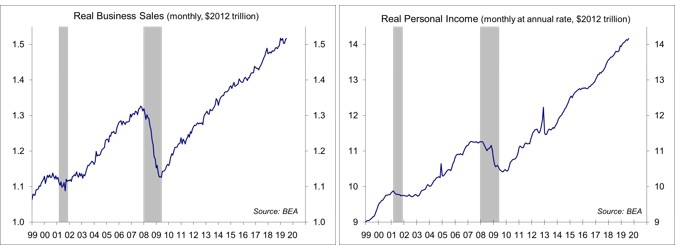

It is difficult to determine when a recession has started. GDP data are available quarterly. Nonfarm payrolls, industrial production, business sales, and personal income are coincident economic indicators (the make of the Conference Board's Index of Coincident Economic Indicators.

The nonfarm payroll figure gets the most weight in the recession determination. Nonfarm payrolls have continued to advance. Job growth has slowed in 2019, but has remained beyond a pace needed to absorb new entrants into the workforce (less than 100,000 per month).

The Federal Reserve’s industrial production figure reflects manufacturing output, mining (including energy exploration and extraction), and the output of utilities. Manufacturing output fell 1.6% from December to July, and was mixed in August and September (with September’s decline reflecting the strike at General Motors). We have often experienced a downturn in industrial production without a recession in the overall economy. The drop in in 2015 reflected a contraction in energy exploration. The Fed’s index of oil and gas well drilling has been falling in recent months.

Real (that is, inflation-adjusted) business sales include wholesale and retail sales plus factory shipments. These data are often uneven from month to month, but the trend since January has been about flat. Bear in mind that services account for a larger share of the economy than goods.

Real (inflation-adjusted) personal income includes wages and salaries, proprietors’ income, farm income, rental income, and interest and dividends, but the measure used by the NBER excludes transfer payments (private pension payments, retirement benefits, unemployment insurance benefits, veteran benefits, disability payments, welfare, and farmer subsidies). The trend through August remained strong.

Other Concurrent Indicators:

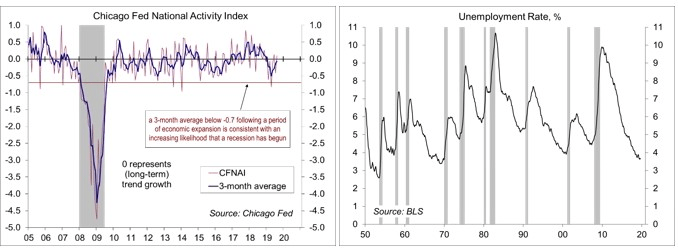

The Chicago Fed’s National Activity Index, a composite of 85 economic indicators, is scaled to have a mean of zero and a standard deviation of one. Zero represents trend growth. A three-month average below -0.7 is associated with an increased likelihood that the economy has entered a recession. The three-month average fell to -0.50 in April, but has since improved (-0.06 in August).

The unemployment rate is a lagging economic indicator, but it can be useful in determining whether a recession has begun. Historically, the unemployment rate has either trended higher or lower; it rarely trends flat. The unemployment rate is reported accurate to ±0.2%, so there’s often a bit of noise from month to month. According to the Sahm Rule, the economy is in a recession when the three-month average rises at least 0.5 percentage points above the minimum of the 12 previous months. The unemployment rate fell to 3.5% in September, a 50-year low -- clearly not trending higher.

Forecasting a Recession:

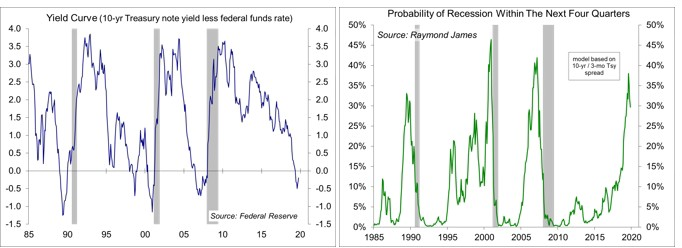

Recessions are difficult to forecast because we have had relatively few of them over the last several decades (11 since the end of WWII). That is a very small sample size. Adding more explanatory variables may provide a better fit in “predicting” past recessions, but will unlikely help in forecasting future downturns. The slope of the yield curve (the difference between long-term and short-term interest rates) is by far the best single predictor of recessions.

The likelihood of entering a recession does not depend on the length of the economic expansion. We are never “due” for a recession. Since the early 1980s, recessions have been few (3) and far between (8-10 years apart).

Narrative economics, the “chronological stories of economic events,” is an old concept (Palgrave Dictionary of Political Economy, 1894), but one that has sparked renewed interest, especially in the aftermath of the 2007-2009 recession. While economic data may provide important clues, getting the story right may be just as important. Each recession is unique in its causes and consequences, but mass psychology typically plays a part.

One concern is that we could talk ourselves into a recession. If, for example, everyone decided to save an extra 5% of their income, that increased savings would coincide with decreased consumption, which is someone else’s income, leading to a further decrease in consumption, and so on. The end result would be a severe recession. A consumer-led recession should not be a big fear currently – job growth, while slower, has still been relatively strong and wage growth has picked up. Gasoline prices have risen recently, which may curtail purchasing power to some extent.

Consumer attitudes usually reflect the overall direction of the economy. However, by itself, confidence doesn’t drive spending. The main driver of consumer spending is income growth, although wealth and the ability to borrow also matter. Presumably, if workers are worried about losing their jobs, they would be less inclined to make big-ticket purchases, such as a new car or a home, contributing to a softer economy. However, most of the evidence of the last few decades suggests that if consumers have the money, they will spend it.

Businesses do have to plan for the future. If a firm expects a weak economy, it will be less likely to expand and hire new workers – and if such sentiments are broader-based, the overall economy will be weaker than it would be otherwise. Conversely, if firms are optimistic, they will be more likely to increase capital spending. There is broad-based evidence that slower global growth and trade tensions have dampened business fixed investment this year and 2020 is an election year. Firms may generally become even more cautious.

Often in the latter stages of an economic expansion, there is a risk that firms could become overly optimistic, and that is especially dangerous if that investment is fueled by leverage. Over-investment or mal-investment would eventually lead to credit problems and a decrease in business investment – the typical boom-bust scenario. There are few signs of such excess currently, but often problems only become apparent when the economy slows.

In the past decades, inventory cycles played a role in recessions and recoveries. Unintended accumulation would lead to reductions in production, and when inventories got low enough, production would pick back up. However, much of the inventory cycle has been eliminated due to computer management and shifts to overseas production. However, trade policy uncertainty has likely led to some stockpiling of materials over the last year or so, which would unwind if that uncertainty goes away. Capital spending still accounts for most of the swing in the business cycle.

Federal Reserve policy is often a factor in recessions. The Fed may raise short-term interest rates too rapidly, choking off the expansion, or it may raise rates too slowly, only to have to raise them more rapidly later on. No one really knows what the neutral federal funds rate is, but after the rate increase in December 2018, we were at the lower end of the range of estimates and Fed officials generally expected one or two rate increases in 2019. What the Fed did not anticipate was the slowing in the global economy and the escalation in trade tensions. This increased uncertainty contributed to a softening in business fixed investment.

As a rule, debt doesn’t matter until it does. That is, high debt levels are typically not a cause of recession, but debt can make a downturn more severe. Ahead of the 2007-2009 recession, non-financial business debt was in good shape. Firms had no difficulty in servicing debt. Mortgage debt was matched by home equity appreciation, which was fine as long as home prices didn’t fall too much (but they did). More troublesome, there was a gigantic amount of leverage in the financial sector. Currently, consumer debt levels appear manageable. High levels of student debt, while a problem for many individuals, are not a systemic problem.

The slope of the yield curve, the difference between long-term and short-term interest rates, is considered to be the best single indicator of a recession. A flattening curve is consistent with a slower rate of economic growth. An inverted curve (short-term rates higher than long-term rates) is a strong signal of a pending recession, but it is typically a year or more between inversion and the economy entering a downturn. The likelihood of a recession depends on how far the yield curve inverts and for how long. An inverted curve implies an expectation that short-term interest rates will decline, and that’s because the economy is expected to fall into a recession and the Fed is expected to respond with lower short-term interest rates. Hence, an inverted yield curve could be thought of as part of the self-fulfilling prophesy framework.

Recession models generate a probability estimate by combining one or more leading indicators. The low sample size is a problem. Adding more variables may better “predict” past recessions, but will not necessarily help in forecasting future recessions. A simple model that uses the slope of the yield curve shows about a 30% chance of entering a recession in the next 12 months, down from around 40% in August.

The Conference Board’s Index of Leading Economic Indicators, which has ten components (including the slope of the yield curve), was designed to predict business cycle peaks and troughs (not the overall strength of the economy). For the last eight recessions, the LEI peaked an average of 13 months before the start of the downturn (and it takes about three months to determine if the LEI has peaked). The LEI has been trending about flat over the last several months and fell in both August and September.

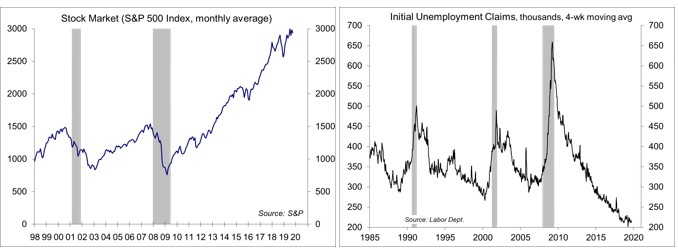

The standard joke is that the stock market has predicted nine of the last five recessions (and economists haven’t predicted any of them). The basis of that joke is that the stock market often gives out false signals. The public still associates the Great Depression with the stock market crash of 1929 (although the story is a lot more complex). In contrast, the market crash in 1987 did not lead to a recession.

State claims for unemployment benefits are an important leading indicator. Weekly figures are subject to some degree of noise. Seasonal adjustment can be tricky. However, the four-week average has continued to trend at a very low level.

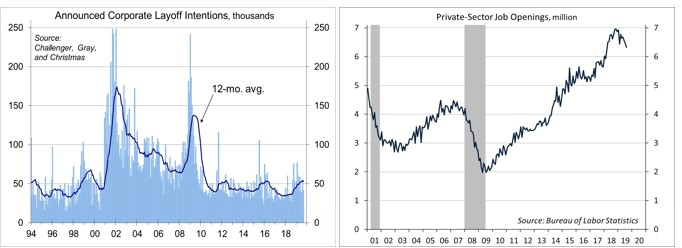

The Challenger Job-Cut Report tallies announced corporate layoff intentions, providing some clues about the strength of the job market. Announced job cut intentions aren’t the same as actual job cuts (as you get attrition and sometimes a change in conditions), but can signal a change. In the first nine months of the year, corporate layoff announcements were 27% higher than the same period in 2018, although still low by historical standards.

The Job Opening and Labor Turnover Survey (JOLTS) data, which include hiring and quit rate, provide some insight into the labor market. Job openings have been trending lower since last 2018, but are still very high. The trend bears watching.

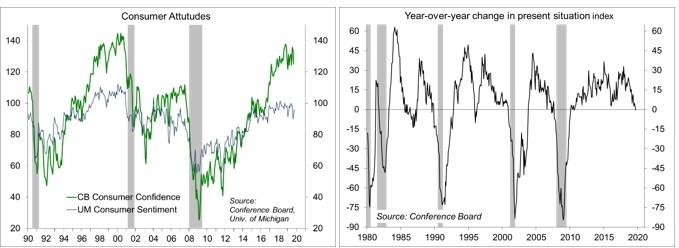

Consumer attitude measures typically fall early in a recession. Surveys have been range-bound over the last several months, but there is some sensitivity to trade policy news.

The year-over-year change in the Conference Board’s present situation component (from the Consumer Confidence report) often drops below zero before a recession, but it has also given some false signals. The figure moved to below zero in the initial estimate for September.

Countering a Recession:

Recessions can be fought through monetary policy (cuts in short-term interest rates) and fiscal policy (tax cuts and spending increases). Monetary policy is quick to be implemented, but affects the economy with a long and variable lag (often a year or more). Fiscal policy has a more immediate effect, but takes longer to implement.

The Federal Reserve takes the leads in countering recessions. Lower short-term interest rates hurt savers, but are the first line of defense in a downturn, reducing borrowing costs for consumers and encouraging bank lending. However, in a typical recession, the Fed lowers the federal funds target by 500 basis points. Currently, the central bank has less than 200 basis points to work with. In the financial crisis (and recovery), the Fed initiated three large-scale asset purchase programs (QE1-3). Each round was seen as less effective, and policymakers are likely to be reluctant to embark on QE4. However, the Fed has embarked on a reconsideration of its monetary policy framework this year. That includes an analysis of possible tools to deal with the next recession. While nothing will be decided right away, we may see some changes announced in 2020. Forward guidance, the conditional commitment to keep short-term interest rates low for an extended period, will remain an important tool. Fed officials have indicated a strong reluctance to implement negative interest rates, where banks would be charged to hold excess reserves. The Fed considered, and rejected, the use of negative rates during the financial crisis.

Fiscal policy (tax cuts, increased government spending) is an option in a recession, but that requires a legislative effort and it’s usually difficult to reach agreement right away. Politicians will often agree to send out tax rebate checks, which is about the least effective stimulus there is (as such checks are much more likely to be saved than spent). The idea behind increased government spending is that it will help to offset a temporary shortfall in private-sector demand. However, determining the size and duration of the stimulus is difficult (let alone the specifics of what to spend it on). The $831 billion stimulus applied to the 2007-2009 recession was mostly over three years (2009-2011). More than a third of the stimulus was tax cuts (which were included in the bill to get the votes of three Republican senators). A third was aid to the states (which were suffering from budget shortfalls). A fifth was infrastructure spending, which only partly replaced the decrease in spending at the state level. The stimulus did help to fill in the gaps on local spending (as suggested by monitoring efforts at the time) and to lessen the impact of the downturn, but was not large enough or of sufficient duration to generate much stronger growth. After the stimulus ran out, a contraction in state and local government dampened the pace of the economic recovery.

The federal budget deficit is expected to have been just under $1 trillion for FY19 (which ended in September), and will likely be a lot larger if the economy falls into a recession. The scope for fiscal stimulus, if needed, may be limited. Moreover, a rising deficit would likely lead to calls for austerity (tax increases or spending cuts), which would restrain the recovery.

In Conclusion:

The key question is not whether we are in a recession now. It is whether we will enter one in 2020. The U.S. economy is expected to slow, reflecting the demographics of an aging population and slower growth in the workforce. Risks to the growth outlook for 2020 remain weighted to the downside. Looking ahead, investors should keep a close eye on the broad range of labor market indicators.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits