I have always loved Boston. My first recollection of the city was when my parents and I used to fly into it spend a night, or two, and then head for our house in Nantucket. Boy, I wish I still had that house. In later life we use to visit the city to see portfolio managers with Fidelity of particular interest. Back then Fido was located on Devonshire not far from Faneuil Hall. It was a heady time when the great secular bull market of 1982 – 2000 was just beginning. Of interest is that in the early 1980s the analysts were not allowed to have a quote machine in their office so they would spend their time reading Qs, Ks, annual reports, etc. Consequently, in the corner of the hallways there was a Quotron Quote Machine and on the “watch buffer” were the favorite stocks of all the analysts. We used to take a small camera with us and when nobody was looking take pictures of those “watch buffers” and do the research on those names when we returned home; but I digress.

Last Wednesday we once again flew into Logan and felt queasy along the way. Chalking it up to a rough airplane ride we took some medication and headed off to a dinner meeting. During that meeting, and a few glasses of wine but nothing out of my ordinary consumption, it proved to be too much. Shortly after dinner “I hit the wall.” The next morning, I felt a little better and was able to make my presentation to the 200 folks attending the NICSA conference. However, by Friday’s plane ride back to Saint Petersburg I was really sick making the ride discomforting. And while we were flying, the stock market was having some discomforting moments of its own with the D-J Industrials (INDU/26770.13) off some 255-points. Yet, the Dow Dive was not as bad as it appeared on the surface because Boeing (BA/$344.00) was off nearly 7%, which accounted for roughly 175 of the Dow’s 255-point slide (the Dow’s Divisor is ~0.1474807). Given that, without Boeing, the Dow was down ~85-points last Friday.

Friday’s Fade took away what was shaping up to be a decent week for stocks driven by numerous good news data points. For the week the Industrials lost 46.39-points closing lower for the fourth time in five weeks. Meanwhile, the S&P 500 (SPX/2966.20) gained 0.54% and the NASDAQ was up 0.40%. Advancers versus Declines were positive at 1898 versus 1139, as were New Highs versus New Lows (303 vs. 101). Such figures confirm our models that show this is merely a pause in the short and intermediate trends with no damage to the primary trend of the secular bull market.

A for the primary trend, my father used to tell me:

Son, if you think it is going up be bullish. If you think it is going down be bearish. But for gosh sakes make a “call” because there are too many folks on Wall Street that talk out of both sides of their mouths so that no matter what happens they can say – see I told you that was going to happen.

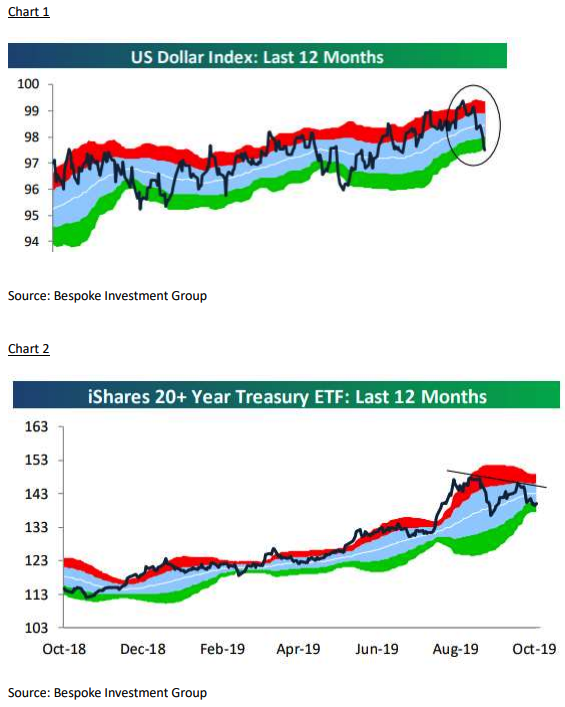

Speaking of going down, the U.S. Dollar Index has been conspicuously weak since its September 30, 2019 closing high (chart 1). Still, we do not hear much talk about “the buck.” If it continues to weaken, however, you will surely hear more about it. The equity markets on the other hand have begun to pay attention to the buck with the strengthening of sectors and stocks that benefit from a weaker dollar. “International” stocks, or stocks that generate a large portion of the revenues internationally have shown hints of outperformance recently. Sectors that tend to benefit are: Consumer Staples (although they are expensive), Healthcare, Industrials, Materials, and Technology.

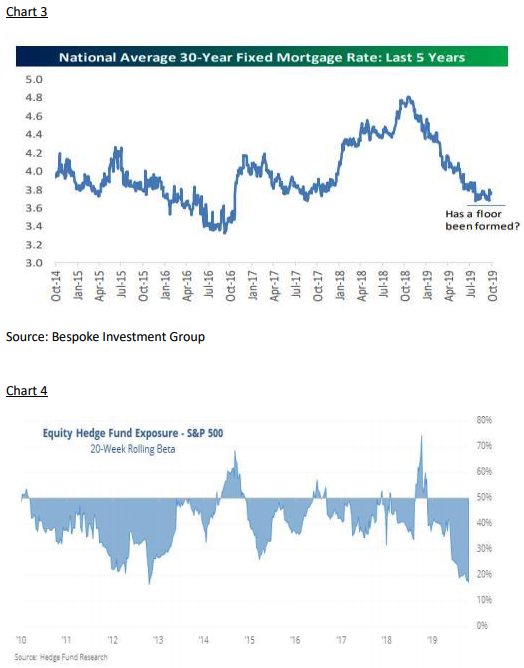

Also not really talked about last week was the fact that a number of “so called” yield curves turn positive (not inverted) with the much watched 10-year Treasury Note yielding ~1.75, up 10 basis points on the week. This has caused a number of fixed income ETFs to decline recently (chart 2) causing one Wall Street wag to ask, “Is the bottom in for mortgage rates?” If so, it could cause some profit taking in the red-hot homebuilder stocks (chart 3).

Given the rate ratchet it is worth noting that the dividend yield on the S&P 500 at 1.92% is still above the 10- year T’note’s yield. This implies that dividends should continue to play an important role in portfolio construction. To this point, I have been writing about the midstream Master Limited Partnerships (MLPs) for a long time and they have not really done much except pay me dividends. My two favorites have been Enterprise Product Partners (EPD/$27.60) that yields 6.41% and Energy Transfer (ET/$12.74) yielding 9.58%; and remember those dividends have a tax favored treatment. We mentioned a few weeks ago some names that screen well on our models and have decent dividend yields. Since the stock market has not moved much in the past two weeks neither have these previously mentioned stocks: AT&T (T/$38.47), Apartment Investment and Management (AIV/$54.48), Blackstone Mortgage (BXMT/$36.21), BCE, Inc. (BCE/$48.87), and Essex Property (ESS/$331.30). There is a much more speculative stock we have repeatedly mentioned in past missives in the low $20s that is currently breaking out to the upside in the charts, Zymeworks (ZYME/$29.62).

As for the economic backdrop. I read this quip from my friend, and one of the best portfolio managers on the Street of Dreams, Craig Drill of Drill Capital:

The US economy continues to chug along close to a 2% pace, with lots of statistical noise. The household sector remains a pillar of strength, with growth in employment exceeding growth in the labor force (a relationship, however, that cannot go on forever). Despite an economic expansion now in its eleventh year -- the longest in history -- inflation expectations remain well anchored around 1.5%. Wall Street strategists forecast a 3% drop year-over-year in third quarter corporate earnings. The consensus for next year is a 10% rise, but others are less optimistic. The Federal Reserve is expected to cut the federal funds rate at least one more time this year. It has also begun to boost its balance sheet at an initial pace of $60 billion a month to reduce market volatility linked to repurchase agreements (repos). As opposed to “quantitative easing,” this action focuses on the purchase of Treasury bills, which provides for a moderate yield curve steepening and indirect support for risk assets.

The call for this week: Well, I spent the weekend in bed with a 101 temperature. The doctor said it was the stomach flu, which has been going around and it started to hit me last Wednesday. My fever broke yesterday and hopefully the stock market will be like me and able to get out of “bed” and “walk” this week. While it is too early to make a call on this quarter’s earnings, our sense remains they are going to come in better than the lowered expectations and that the “beat rate,” companies beating the analysts’ estimates, will be +65%. Certainly, the psychological backdrop is right for an extension of the rally with ex-Merrill Lynch’s brilliant strategist’s Sentiment Indictor showing more pessimism now than at the December 2018 lows. Further, hedge fund exposure to stocks and sectors is the lowest since the end of 2002, 2008 and 2011. The SKEW has jumped to a six-month high (read: bullish). While our models are “bulled up,” there just is not a bunch of “internal energy” available right now. So, the stock market may continue to churn this week, but that is not bearish. This morning China’s GDP growth tags a 30-year low (tariffs) and the U.S. imposes a record $7.5 billion in tariffs on European goods as Europe vows retaliation. But, it seems none of that matters as the preopening ESUs are up ~8-points because it is all about earnings.

Investing/trading involves substantial risk. The author and Saut Strategy do not guarantee or otherwise promise as to any results that may be obtained from using this report. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first consulting his or her own personal financial advisor and conducting his or her own research and due diligence, including carefully reviewing any prospectus and other public filings of the issuer. These commentaries, analyses, opinions, and recommendations represent the personal and subjective views of the author, and are subject to change at any time without notice. The information provided in this report is obtained from sources which the author believes to be reliable.

© Saut Strategy

Jeffrey Saut

[email protected]

More ETF Topics >