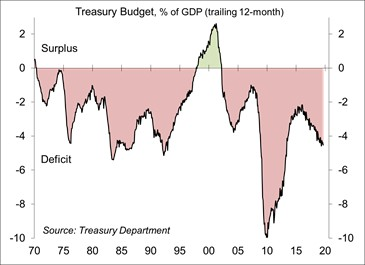

The Treasury Department is expected to report that the federal budget deficit for FY19 (which ended in September) fell short of $1 trillion. That’s a lot of money, especially with an economy running full tilt. However, the government currently doesn’t have any problem borrowing. Some will worry that the deficit will become a crisis, but that’s unlikely. The greater concern is that the deficit will constrain our ability to respond to the next recession and well-meaning efforts to reduce the deficit will either worsen the downturn or restrain the recovery.

The nonpartisan Congressional Budget Office estimates that the FY19 deficit was $984 billion, 26% higher than in FY18 and 68% higher than in FY16. Outlays rose about 8% (Social Security +6%, Medicare +6%, Defense +8%, Interest +14%), and receipts were up 4% (individual taxes +2%, payroll taxes +6%, corporate taxes +12%). While corporate tax receipts improved from FY18, they were still 23% lower than in FY17. We have run larger budget deficits before. The deficit ballooned to $1.4 trillion in FY09 (or 10% of GDP), reflecting the magnitude of the economic downturn. Recession-related spending (unemployment insurance, food stamps, aid to the states) rose, while tax receipts dried up. As the economy recovered, the recession-related spending went away and tax receipts picked up. By FY15, the deficit had fallen to just 2.4% of GDP. While smaller than in FY09, The FY19 deficit comes with an economy near full employment. If we were to fall into a recession, the deficit would climb.

Click here to enlarge

Recessions are fought through a combination of fiscal policy (tax cuts and spending increases) and monetary policy (cuts in short-term interest rates). Fiscal policy stimulus is generally difficult to implement, but has a relatively quick effect on the economy. In contrast, monetary policy changes can be taken quickly, but the impact on the economy may not be felt for a year or more. In a typical recession, the central bank lowers the federal funds target rate by 500 basis points. The scope for monetary policy stimulus is more limited now and the proximity to the zero lower bound on interest rates means that action should be taken quicker. With the deficit trending higher, there is likely to be less scope for fiscal stimulus as well. Moreover, we may see efforts to reduce the deficit (tax increases or spending cuts), which would dampen the recovery. That was the case in Europe during the recovery from the financial crisis. The European economy slowed, leaving deficit improvement short of expectations. The U.S. also went through a brief period of austerity, but on a much smaller scale. There are few signs that politicians learned anything from that.

It’s well known in Washington that the deficit only matters when the other party occupies the White House (even though the budget responsibility is shared with Congress). Heading into an election year, the budget is expected to be a key issue.

There’s a growing debate among economists about deficits. Much of it centers on Modern Monetary Theory (MMT), which has been embraced by Alexandria Ocasio-Cortez (D-NY). Stephanie Kelton, MMT’s main proponent, is an advisor to Bernie Sanders. A key problem with MMT is defining precisely what it is. Countries that borrow in their own currency cannot default. The U.S. is not going to go bankrupt. No argument there. MMT followers argue that high budget deficits should not be a constraint on spending. We can run much larger deficits, although most admit that won’t be true at some level (well above where we are now). MMT suggests that fiscal policy should target inflation not monetary policy (this is where MMT loses most economists).

The MMT debate has fallen into the broader issue of re-evaluating macroeconomic theory. In one sense, it’s seen as a difference between the old guard and the new. However, MMT is not a widely accepted theory. Olivier Blanchard, former chief economist of the IMF and MIT professor, argues that the Fed can’t just print money to finance an increase in government spending. There is some nuance here. The Fed has expanded its balance sheet by purchasing assets, but this is not the same as printing money. Blanchard argued earlier this year that the low level of interest rates implies that governments should worry less about deficits. As long as the (nominal) growth rate of the economy exceeds interest rates, which has been generally true over time (the exception was in the 1980s), there should be no problem. Blanchard isn’t arguing that deficit can increase indefinitely. Rather, concerns about the deficit are overblown and fiscal policy should be employed more aggressively to help the economy out of recession.

Democrats want to increase spending in a number of areas (expanding healthcare, relieving student debt, etc.), but have traditionally struggled with how to pay for it. Republicans want to cut taxes further, and have never worried about paying for it (spending cuts will presumably come later). If one believes that deficits aren’t as much of a constraint as generally feared, then that would open up room for more spending, including a large-scale infrastructure spending program (which has not taken off due to an inability to pay for it).

All of this is just the beginning of a broader discussion among economists about the debt and deficits. The debate among politicians and the general public is likely to be less nuanced, much more heated, and dominated by rhetoric and posturing.

Data Recap – Trade policy perceptions remained the dominant factor for the financial markets. Optimism for a mini-deal or trade truce increased as high level trade talks got underway. The Fed announced Treasury bill purchases (balance sheet expansion), but emphasized that this reflects a focus on maintaining an adequate level of reserves and is not the same as quantitative easing.

In his speech to the National Association for Business Economics, Fed Chair Powell indicated that policymakers “will be data dependent, assessing the outlook and risks to the outlook on a meeting-by-meeting basis.” He said that “at present, the jobs and inflation pictures are favorable.” However, “there are risks to this favorable outlook, principally from global developments.” He acknowledged the mid-September volatility in wholesale funding markets and said that “my colleagues and I will soon announce measures to add to the supply of reserves over time.” As the FOMC indicated in its March statement on balance sheet normalization, “at some point, we will begin increasing our securities holdings to maintain an appropriate level of reserves -- that time is now upon us.” However, he strongly emphasized that “growth of our balance sheet for reserve management purposes should in no way be confused with the large-scale asset purchase programs (QE) that we deployed after the financial crisis.”

The Fed’s Board of Governors announced that it will purchase Treasury bills “at least into the second quarter of next year” to maintain an ample level of reserve balances. The Fed also indicated that it would conduct term and overnight repurchase agreement operations (repos) “at least through January.” The Fed stressed that “these actions are purely technical measures to support the effective implementation of the FOMC's monetary policy, and do not represent a change in the stance of monetary policy,” but they may make an October 30 rate cut less likely.

The FOMC Minutes from the September 17-18 policy meeting showed that senior Fed officials were divided on the appropriate course of monetary policy. Their baseline expectations for the economy were little changed, anchored by a belief that “households pending would likely remain on a firm footing.” However, FOMC participants “generally had become more concerned about risks associated with trade tensions and adverse developments in the geopolitical and global economic spheres.” Moreover, “several participants mentioned that uncertainties in the business outlook and sustained weak investment could eventually lead to slower hiring, which, in turn, could dampen the growth of income and consumption.” Participants agreed that policy was not on a preset course and would depend on the implications of incoming information for the evolution of the economic outlook.”

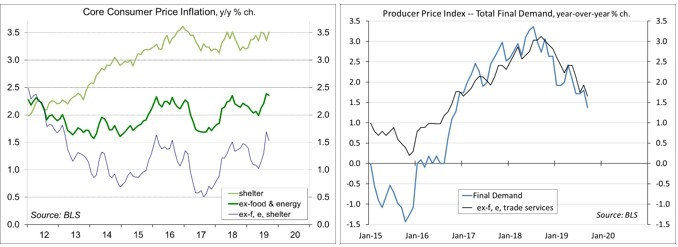

The Consumer Price Index was unchanged in September (+1.7% y/y), held down by lower gasoline prices and a sharp drop in used vehicle prices. The price index for food edged up 0.1% (+1.8% y/y), still mixed (food at home up 0.6% y/y, food away from home up 3.2% y/y). Gasoline (4.0% of the CPI) fell 2.4% (-0.9% before seasonal adjustment, and -8.2% y/y). Ex-food & energy, the CPI rose 0.1% (+2.4% y/y) – note that the year-over- year increase in the core PCE Price Index was 0.6% below the core CPI in August. Ex-food & energy, the price index for consumer goods fell 0.3% (+0.7% y/y). The index for used vehicles fell 1.6%, following a 3.5% rose over the three previous months (+2.6% y/y). Non-energy services rose 0.3% (+2.9% y/y). Shelter rose 0.3% (+3.5% y/y).

Click here to enlarge

The Producer Price Index fell 0.3% in September (+1.4% y/y), reflecting a 2.5% decline in energy prices (-8.7% y/y). Wholesale gasoline prices fell 7.2% (-4.3% before seasonal adjustment, -16.0% y/y). Food rose 0.3% (+2.7% y/y). Trade services fell 1.0% (+3.1% y/y). Ex-food, energy, and trade services, the PPI was unchanged (+1.7% y/y). The index for transportation and warehousing fell 1.0% (+1.0% y/y). Ex-food & energy, unprocessed intermediate goods fell 4.2% y/y, with processed intermediate goods down 2.3% y/y. These figures do not directly include tariffs, but tariffs may be passed through to some intermediate goods. Intermediate services rose 2.4% y/y.

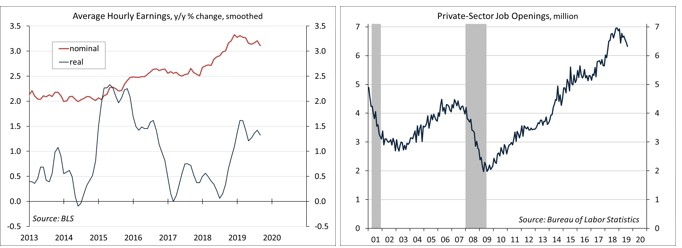

Real Average Hourly Earnings were unchanged in September (+1.2% y/y), but rose 0.2% for production workers (+1.9% y/y).

Click here to enlarge

The Job Opening and Labor Turnover Survey (JOLTS) data for August showed a further retreat in job offerings (down since late last year, but still high by historical standards). Hiring rates and quit rates edged slightly lower.

Import Prices rose 0.2% in September (-1.6% y/y), held up by a 2.3% increase in petroleum costs (-5.8% y/y). Ex-food & fuels, import prices were flat (-1.1% y/y). Ex-fuels, prices of industrial supplies and materials rose 0.5% (-2.2% y/y). The price index for imported capital goods was flat (-1.2% y/y), the price index for imported autos was unchanged (-0.7%), and the index of consumer goods held steady (-0.4% y/y). These data do not include import duties (tariffs).

The UM Consumer Sentiment Index rose to 96.0 in mid-October, vs. 93.2 in September and 89.8 in August. With the exception of the drop in August (from 98.4 in July), the headline figure has remained relatively range-bound over the last several months. Survey responses remain sharply divided by political affiliation (D: 72.3, I: 99.3, R: 120.3).

The Small Business Optimism Index fell to 101.8 in September, vs. 103.1 in August and 104.7 in July – still relatively strong by historical standards. The general business outlook weakened further. The earnings trend remained weak. Hiring plans cooled, although actual hiring was moderate. Capital spending plans remained moderately strong.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

More Tax Planning Topics >