Psychology is the reason most investors fail to keep up with the markets, and why contrarian strategies have turned in consistently superior performance over time. This same inability to understand psychology is often why academics don’t incorporate its use and instead stay with what may be flawed modern portfolio theory. This is the major premise of David Dreman’s new book, Contrarian Investment Strategies: The Next Generation. . . . The major reason why most conventional investment approaches fall short is because predicting and forecasting is so difficult, and most people don’t recognize the limitations of forecasting. Investors typically overreact in either direction, and this is where the opportunities arise. The strategies that Dreman endorses involve the pursuit of those stocks that the experts would avoid and, conversely, to eschew those exalted favorites whose risks may be understated. In unloved companies, the risks are generally overstated. There are many dimensions of risk, and the one now in common use of equating risk with volatility is faulty. This methodology doesn’t mean to confine attention to companies that appear headed for the junk heap, but to find solid companies that for a variety of reasons may currently be in disfavor. In his book, Dreman trots out a number of studies, both old and new, that he believes illustrate the superior results of contrarian strategies over time. He also espouses a new approach incorporating relative rather than absolute valuation standards.

. . . Eric Miller, Donaldson, Lufkin & Jenrette (May 13, 1998)

We recalled Eric Miller’s quip from an era gone by while reading this from the uber smart Jason Goepfert of SentimenTrader fame:

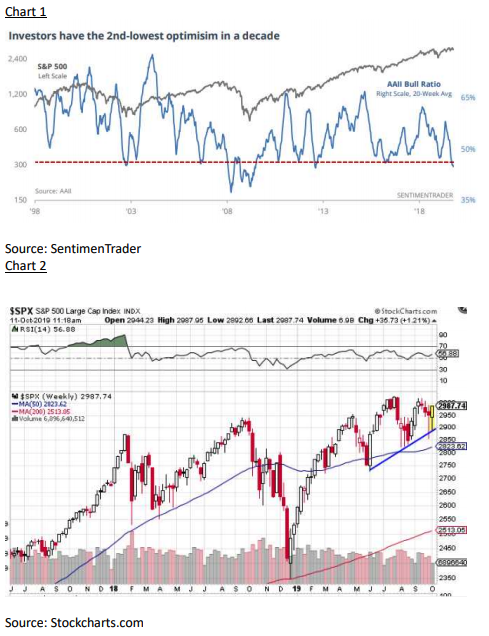

Individual investors just won’t buy into this market. The latest AAII survey showed yet another drop in optimism. Over the past 20 weeks, the Bull Ratio has dropped to the 2nd-lowest level since the financial crisis, nearly exceeding the prior extreme from August 2012. For a year when the S&P has done very well, the average Bull Ratio year-to-date ranks among the 10 lowest all-time (chart 1).

For the contrary investor such pessimism is a clear cut “buy signal” for stocks. Indeed, we deemed the August 5, 2019 “selling climax” low to be THE low. That low of ~2822 basis the S&P 500 (SPX/2970.27) was retested three times and was never violated. Subsequently, last Monday (10-7-19) we wrote:

Provided there are not any more shocking news revelations, it looks to us like the stock market bottomed last Thursday morning (October 3). However, unlike August 5th’s V-shaped “selling climax” low this bottom should be more of a process with the potential for a few retests of last week’s low (2855 basis the SPX). Eventually, the SPX should switch back to a mildly bullish mode and move towards the all-time highs. The problem is the stock market’s “internal energy” has been used up making a rally to above new all-time highs difficult in the short run.

Later in the week we told several institutional accounts that if the upward sloping blue trendline was not violated on a closing basis the upside should be favored (chart 2). That trendline was never violated. So, what we have is the “selling climax” low of August 5th followed a “throwback rally, and then a secondary low on October 3rd at ~2855. Admittedly, our “bottoming process” did not play all that well, or for quite as long as we thought, yet it certainly looked like it would until last Friday’s Fling (+320 Dow points). For example, the SPX’s intraday high on October 3rd was ~2911 and last Thursday’s intraday low was ~2917 (read: bottoming process), but then came Friday’s Dow Wow on news of a trade deal with China. As often stated in these missives, “In secular bull markets most of the surprises come on the upside!”

Also as often stated, we do not make individual stock/bond/mutual fund, ETF, etc. recommendations unless we think the odds of making money are tipped in favor of participants. To that point in last Monday’s strategy reports we wrote:

One good thing about a pullback is that you get to see which stocks hold up the best. Some of the ones that hit our screens, and model well under our systems: AT&T (T/$37.58), Apartment Investment and Management (AIV/$53.55), Blackstone Mortgage (BXMT/$35.85), BCE, Inc. (BCE/$48.88), and Essex Property (ESS/$326.96) all of which possess decent dividend yields. There is a more speculative stock that has recently been ruffed-up (-18%) and has hit our screen, which is owned by Mary Lisanti, as well as another great small cap portfolio manager and our friend, Amy Zhang. Amy manages The Alger Small Cap Focus Fund (AOFAX/$20.18) another fund we own. The name both own is Wingstop (WING/$88.65).

Given last week’s early-week gyrations none of those names have moved very much and we still like them.

Moving on, last week’s late strength broke the SPX above the downtrend line that has been in place since September (chart 3) leaving ALL the major indices we monitor higher for the month of October. However, on a sector basis the news is a tad different. On the downside Energy, Materials and Utilities have been the losers with Utilities likely getting hit because of the rather large backup in interest rates (chart 4). That backup caused the yield curve to giggle (chart 5), which should be good for Financials and bad for defensive names. The quid pro quo is that the Technology and Communication Services sectors were up some 1%. Surprisingly, given the backup in rates, the euro has been manifestly higher versus the U.S. dollar (chart 6). As for the economy, for weeks we have written that the “hard” economic data was much stronger than the “soft” economic date (read: surveys). That changed with two-thirds of last week’s economic releases coming in weaker than estimated. But remember what Tom Bowley wrote last week:

During our last period of consolidation from 2014 to 2016, here's the GDP growth: 2014: +2.5%; 2015: +2.9%; 2016: +1.6%. The S&P 500 consolidated as we approached the slowdown but took off during the year that actually posted the worst GDP grow number. Why? Because the stock market is the best leading economic indicator

The call for this week: Earnings season begins and despite the “Street Screams” that earnings are decelerating, we do not believe it. Yes, this quarter’s reports may “soften,” but we expect them to strengthen going forward. Obviously, this is a “contrarian call,” but as stock market genesis Leon Tuey writes:

After some further mucking around, the market will skyrocket. The Bears are going berserk and Bulls are scarce (chart 7). Note current Bulls are at the same level as in December when investors panicked.

Moreover, we have been basically range-bound for a pretty long time. However, the last year and a half looks like just another period of consolidation after the previous leg higher. We made similar observations when the SPX was consolidating from May 2015 to February 2016 when the negative nabobs were telling us a stock market crash was coming, a recession/depression was due, earnings were going to collapse, blah, blah, blah. As Old Turkey would say in the book Reminisces of a Stock Operator, “It’s a bull market you know!”

PS: They sold the trade news late in Friday’s session because like we said on three different TV shows last week, “They may come up with some kind of truce, but there will be no substantial trade agreement in the near-term.” To wit, Friday’s trade announcement was more of a reprieve than a real de-escalation in hostilities. Further, the unnoticed event last week was not the hypothetical US-China limited trade deal; it was the Fed’s introduction of $60B/month of non-QE (QE 4). Mondays tend to be rally days, especially during expiry week. However, the market was disappointed in the ‘phase one’ US-China trade deal. The staggering dynamic overhanging the market is the Fed’s new QE scheme. Consequently, the preopening S&P 500 futures are off some 7 points as China says more trade talks are needed.

Investing/trading involves substantial risk. The author and Saut Strategy do not guarantee or otherwise promise as to any results that may be obtained from using this report. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first consulting his or her own personal financial advisor and conducting his or her own research and due diligence, including carefully reviewing any prospectus and other public filings of the issuer. These commentaries, analyses, opinions, and recommendations represent the personal and subjective views of the author, and are subject to change at any time without notice. The information provided in this report is obtained from sources which the author believes to be reliable.

© Saut Strategy

Jeffrey Saut

[email protected]

More ETF Topics >