“The market itself determines the relative importance of all factors more accurately than any speculator can hope to interpret them.”

. . . Don Guyon, One Way Pockets (1917)

“The market itself determines the relative importance of all factors more accurately than any speculator can hope to interpret them.” So wrote Don Guyon in the seminal book One Way Pockets, one of the best stock market books ever written. The book was written in 1917 and to be sure NOTHING has really changed since then because human nature has not changed. Investors and traders can buy and sell based on their own interpretation of the daily news, but the market action itself determines the true and the most accurate interpretation. In other words, if the investor, or trader, isn’t in sync with the stock market, he/she is going to suffer losses. So, when the stock market speaks, if you want to make money, you had better listen! And the stock market has repeatedly spoken over the past few months, as well as since October 2008 when most of the stocks bottomed, with multiple buy signals according to Dow Theory. Many participants have chosen to ignore the message of the markets, swayed by valuation concerns, low GDP growth, earnings worries, and broken-clock pundits who suggest the trading range will be extended at best, or at worst a bear market has begun. Yet as Ralph Waldo Emerson opined, “Foolish consistency is the hobgoblin of little minds.” Unfortunately, there are far too many “little minds” on the Street of Dreams these days.

Recently, the markets have been gyrating in a narrow range. Again, according to the book One Way Pockets:

When a market fluctuates for several weeks or months within a narrow range, one of these three things is happening: pools and large operators are accumulating securities by absorbing the offerings of tired holders; or they are distributing certain stocks under cover of artificial strength in others; or the market is in a state of uncertainty and waiting a fresh impulse.

As stated in the book’s more recent introduction – the author, who assumed the nom de plume of “Don Guyon” to avoid being identified with his wealthy clients – was associated with a boutique brokerage firm S a u t S t r a t e g y that had sizeable business with investors in all sections of the country. In 1915 he began an analytical study of the orders executed for certain active traders with the idea of determining the fundamental weakness, if any, in their speculative methods. The results were illuminating enough to afford corroborative evidence of general trading faults, which persist to this day. While I have found many of the book’s insights helpful to my investment process, and urge investors to study said book, there have been other investment methods of interest.

Perhaps the best way is to emulate some of the trading principles used by yesteryear’s legends, who beat the market no matter the emotions and mechanics of the institutional herd, is to study them. To wit:

Bernard Baruch – Eighty some years ago, he would research a stock, buy it, and then each time the stock rose 10% from his purchase price, buy an additional amount equal to his first purchase. If the stock began declining, he would sell everything he had bought when the drop equaled 10% of its top price.

Baron Rothschild – His success formula was centered on the famous quote attributed to him – “I never buy at the bottom and I always sell too soon.”

Jesse Livermore – This legendary speculator profited enormously by calling the vigorous 1921 and 1927 advances correctly. In 1929 he reasoned that the market was overvalued, but finally gave up and became bullish near the top in the fall of that infamous year. He quickly cut his losses, however and switched to the short side. Livermore listed three major points for success: Sensitivity to mob psychology, willingness to take a loss, and liquidity (meaning that stock positions should not be taken that cannot be sold in 15 minutes at the market).

Addison Cammack – A broker from Kentucky, who swore by the two-point stop-loss. “If you’re wrong,” he said, “You might as well be wrong by two points as ten.” He followed this method successfully and was one of the few bears to make a fortune on Wall Street and keep it.

Have we got you thinking about what trading/investment strategy to follow? Well, we’ve been holding the best system for last. Here is the sure-thing formula for success, “Don’t gamble – take all savings and buy some good stocks, and hold them until they go up, then sell then . . . if they don’t go up, don’t buy them!”

– Will Rogers

I first heard about One Way Pockets in the early 1970s when Merrill Lynch’s Chief investment Strategist (Bob Farrrell) referred to it as his “investment bible.” Since then, I have read the 64-page book many times and always found it insightful. Obviously, the quote I began this report with has stuck with me and I think that quote is applicable for the current stock market because the S&P 500 (SPX/2961.79) has been locked in a narrow range since September 4, 2019 (2940 – 3020). Most recently that may be about to change. To wit, our models called the trading peak in late-July and the subsequent “selling climax” low of August 5th, which we deemed to be THE low. Since then we have been looking for new all-time highs, a “call” that hasn’t materialized. A few weeks ago, we began writing that those same models were forecasting the potential for problematic trading in the first part of October and maybe sooner. We mentioned that again in last Monday’s missive and punctuated it in last Thursday’s “Trading Flash” where we wrote:

The first part of October is showing up as problematic on a trading basis and potentially before then. Obviously, when we wrote that we had no idea of the impeachment inquiry bombshell. Nevertheless, news events typically only have a short-term impact on the primary trend of the stock market; and in this case, the primary trend is UP. Consider this, in the late-1990s the equity markets we in a primary uptrend. Accordingly, following the Clinton impeachment (10-8-1998) the stock market was up some 30% a year later. The Nixon impeachment was another story as the D-J Industrials fell ~30% from 2-1974 into its bear market low in 12- 1974, but back then the equity markets had already been in a bear market since January 1973. Further, the prime rate in 1974 was 11%, car sales were down 34%, Franklin National Bank declared bankruptcy, and Nixon resigned. More recently, we have gotten several questions about why we have not made any investment recommendations over the past few weeks. To that we reply – we only make recommendations when we think the odds of success are high – we have not felt that way for the past few weeks.

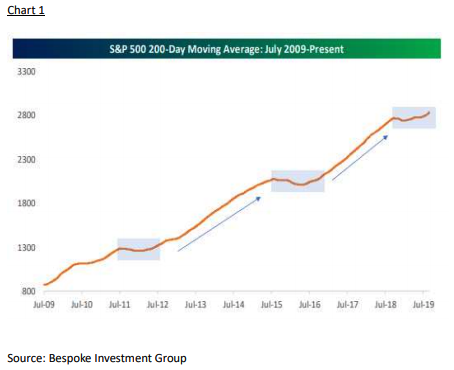

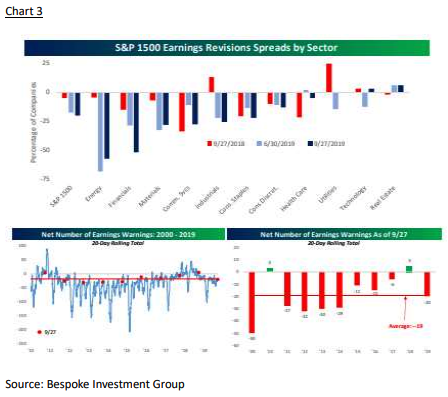

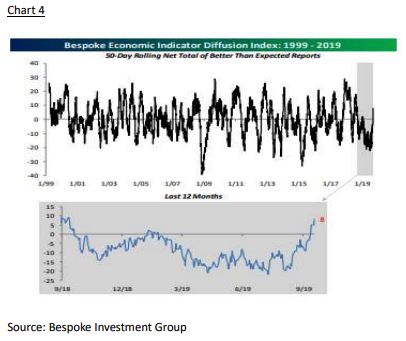

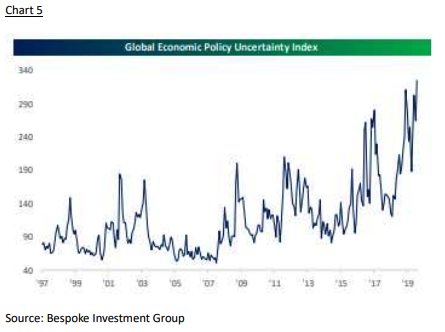

As for the equity markets, last week the SPX dipped into Andrew’s 2940 – 2950 support zone and in the process “kissed” its 50-day moving average (DMA) at 2948.82. That level held leading to a rebound that left the SPX off 15.83 points for Friday’s session, which was a vast improvement from the minus ~30-points that was the intraday “print” low. Despite the day’s rebound, our short-term proprietary model still is cautious on a near-term trading basis going into the month of October. That said, any pullback should be shallow with a max drawdown into the 2880 – 2900 zone; and, maybe not even that deep. Longer term our views have not changed. We continue to believe in our long-term secular bull market “call” that has been in effect since the bottoming process began in October 2008. That view is reinforced by the SPX’s upward sloping 200-DMA (chart 1). And, while the SPX has not made a new all-time, the Advance-Decline Line has (breadth usually precedes price). Bearish sentiment continues to rein supreme among investors as reflected in the AAII numbers (chart 2). This negative stock market sentiment is also reflected in analysts’ earnings estimates that have continued to be reduced (chart 3). Remember, however, that negative analyst earning’s sentiment has historically translated into positive returns for the S&P 500 in the ensuing earnings season (a tip of the hat to Bespoke Investment Group). As for the cries about a pending recession we have been hearing about for years, as repeatedly stated we see no evidence a recession will occur (chart 4). To be sure, about the only negatives we see are Chinese trade issues and potential capital controls concerns, as well as the impeachment rhetoric (chart 5).

The call for this week: In last Thursday’s “Trading Flash” we wrote:

The first part of October is showing up as problematic on a trading basis and potentially before then.” . . . More recently, we have gotten several questions about why we have not made any investment recommendations over the past few weeks. To that we reply – we only make recommendations when we think the odds of success are high – we have not felt that way for the past few weeks.

That said, for your potential “watch/buy lists,” the Financials look to be setting up for an upside breakout and have a positive “energy rating.” Emerging markets also are interesting and “cheap.” Watch the SPDR Emerging Markets ETF (SPEM/$34.30) with a $33.10 stop loss point. Also, of interest is the 8%+ yielding Morgan Stanley Emerging Markets Domestic Debt Fund (EDD/$6.51) with a $6.19 stop loss point. This morning funding pressures have subsided even though it should be increasing with month’s end. The effective Fed funds rate fell to 1.85% as there was only $22.7B of securities in demand for the overnight repo, which has a limit of $100B. Dealers submitted only $49B of securities for the 14-day term repo, which has a limit of $60B. Meanwhile, the Atlanta Fed boosted their Q3 GDP from 0.2 to 2.1%, the UOM Confidence Rebounds [93.2 from 92], and U.S. Treasury Says No Plans to Block Chinese Listings “at This Time.” All of this has the preopening ESUs up about 9 points in pre trading as end of month machinations play

Investing/trading involves substantial risk. The author and Saut Strategy do not guarantee or otherwise promise as to any results that may be obtained from using this report. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first consulting his or her own personal financial advisor and conducting his or her own research and due diligence, including carefully reviewing any prospectus and other public filings of the issuer. These commentaries, analyses, opinions, and recommendations represent the personal and subjective views of the author, and are subject to change at any time without notice. The information provided in this report is obtained from sources which the author believes to be reliable.

© Saut Strategy

Jeffrey Saut

[email protected]

More ETF Topics >