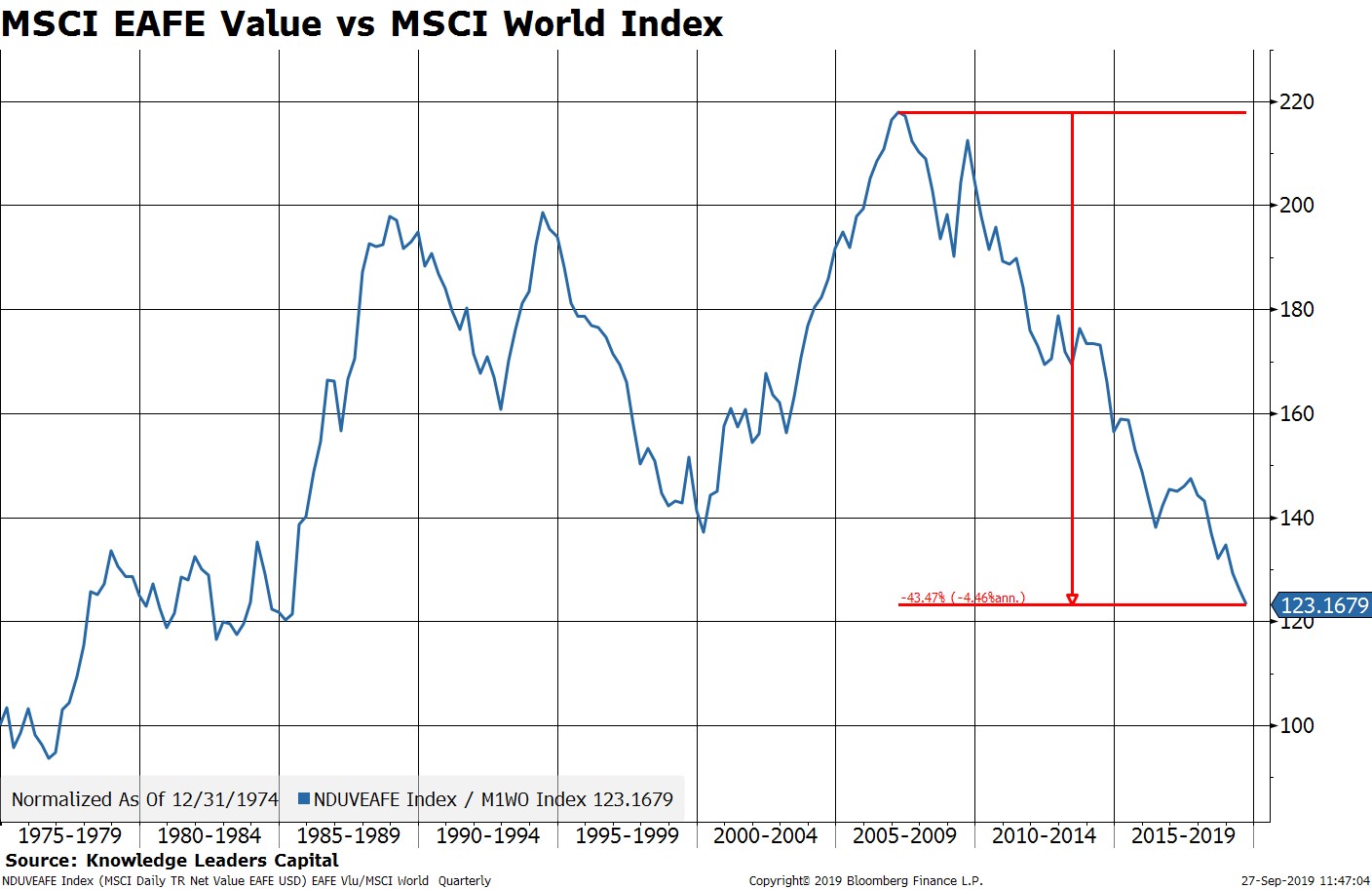

At some point the global economy will get a dose of reflation. Whether that comes from the current central bank easing cycle, fiscal policy response, coordinated fiscal-monetary action, or a détente in the US-Sino trade dispute is not yet known. However, when it happens a certain group of stocks may be uniquely positioned to benefit from it. It’s a group of stocks that has been pretty much left for dead over the last 13+ years and a group that has underperformed global equities by a cool 43% since 2007: international value. It’s an area of increased focus for us recently and an area we’ll be talking more about in the months and quarters ahead.

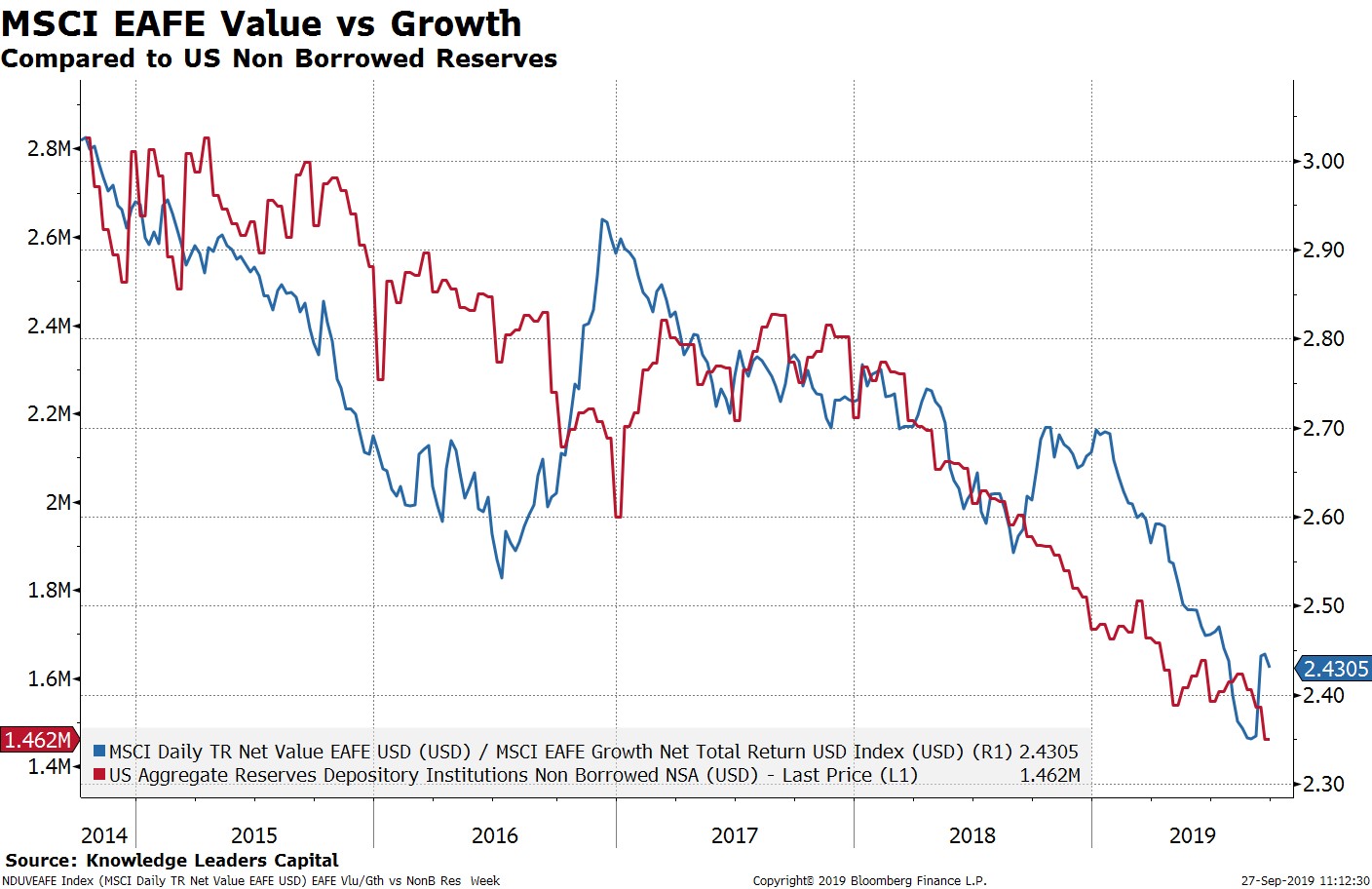

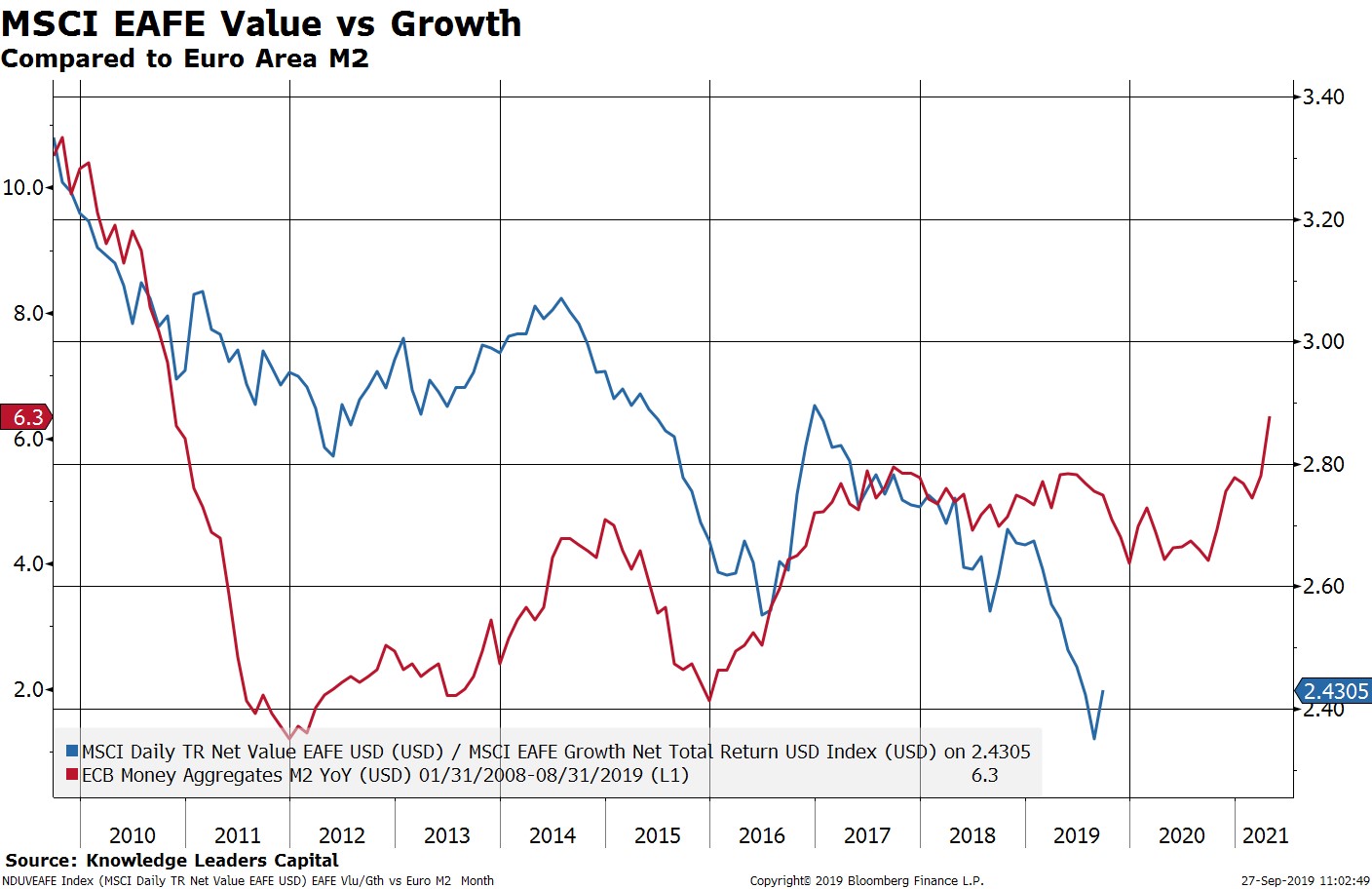

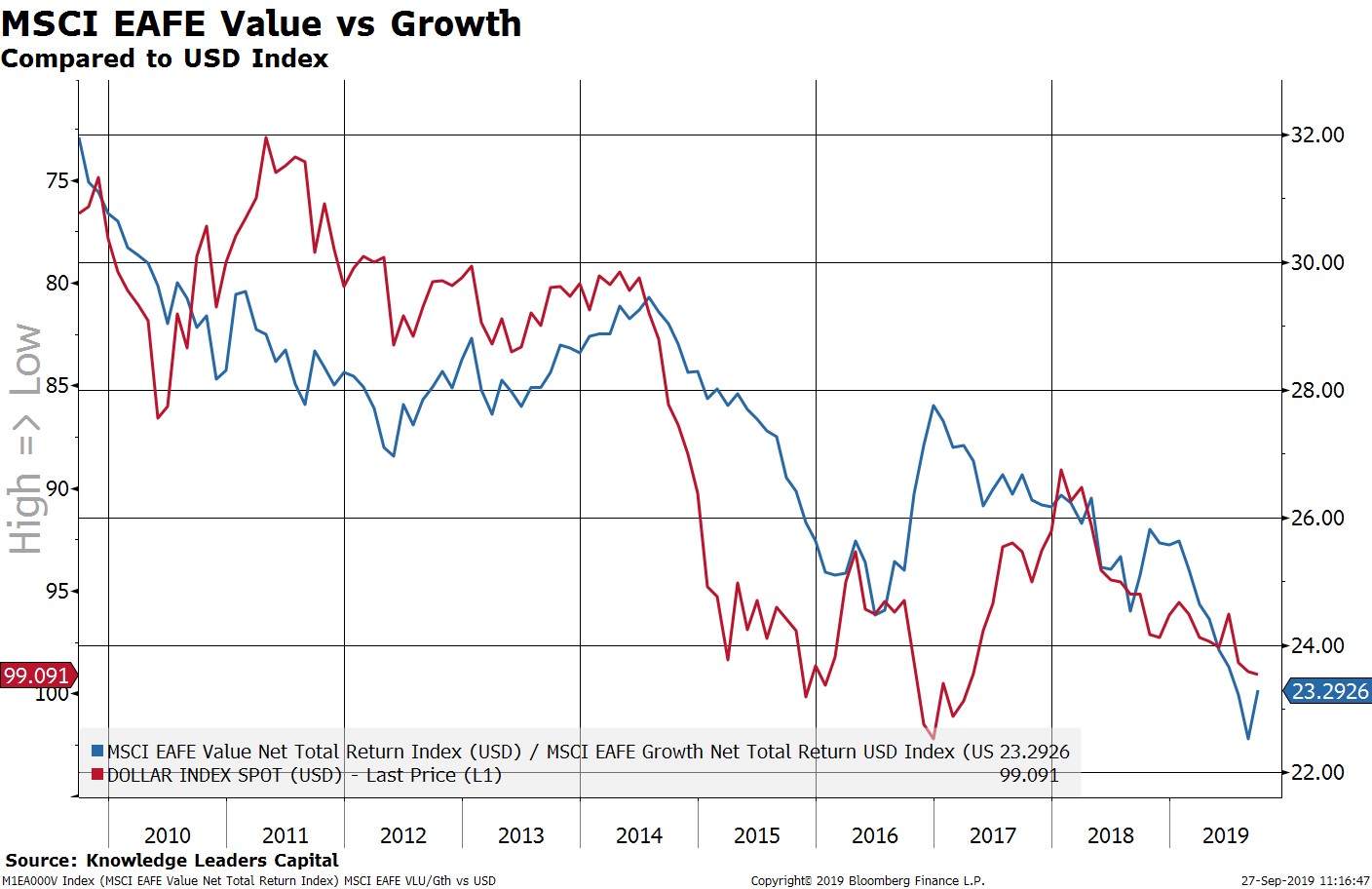

For international value to work we need reflation. Reflation can mean a lot of different things, but suffice it so say that money growth is a key component. Of interest recently is that funding pressures in the overnight lending markets in the US is causing the Federal Reserve to rethink its policy of draining bank reserves from the system via balance sheet shrinkage (red line in the next chart). It’s becoming increasingly obvious that the Fed will in fact need to commence balance sheet growth in order to facilitate smooth operations in those overnight funds markets. The Fed’s balance sheet is one avenue of liquidity creation and it is closely related to the relative performance of international value compared to growth (blue line below). When, not if, the Fed begins to grow its balance sheet once more, the liquidity created could be an important reflationary driver of foreign value stocks.