I have been reading Shad Rowe’s prose since the 1970s when he wrote a column for Forbes’s magazine. More recently Shad and I met in his Dallas office to discuss the markets, stocks and his investment style. That was about six or seven years ago. Shad is one of the best long-term investors I know, so I thought his August investment letter to the clients of Greenbrier Partners was particularly instructive. He wrote:

Through August, Greenbrier Partners, Ltd. (“Greenbrier”) is up 23.6% net of expenses and profit reallocation (this is an unaudited number). In comparison, the S&P 500 is up 18.3% including dividends.

“He really doesn’t Do anything. All he does is buy and hold. What I need are people who make money” is a comment I occasionally hear from arithmetically challenged investors. I plead guilty. What we attempt to do is simple – identify great companies that fit within compelling long-term themes . . . companies that do something better, faster and cheaper FOR instead of TO their customers, with balance sheets big enough to go after huge opportunities. We attempt to buy shares at reasonable prices, and then hold on (hopefully forever). This is a strategy that should be easy to replicate and borrows heavily from T. Rowe Price, Peter Lynch, John Train, Philip Fisher, and Warren Buffett to name a few. It is a strategy that also flies in the face of conventional Wall Street wisdom. (We do also spend a considerable amount of time checking and rechecking the validity of our theses.)

I have noticed that the truly great companies and great managers generally get better over time. I have also noticed that most investors tend to sell their winners if they meet short-term objectives (12-month price target, financial projections, whatever). And so, they sell, and then they have to start all over, thus damning themselves forever to money manager underperformance hell. The opportunity to buy the shares of a great company at a fair price is rare. So, selling a great company because it surpasses an arbitrary price target after six, 12, or 18 months seems on its face to be counterproductive and tax-inefficient.

Losers seem to take care of themselves, as their stock prices drift off into oblivion. Mediocre investments are more difficult, and they represent an opportunity cost. We believe that investors should be careful with their losers, but we think they should be especially careful with their winners – selling too early is the most overlooked detractor from long-term outperformance.

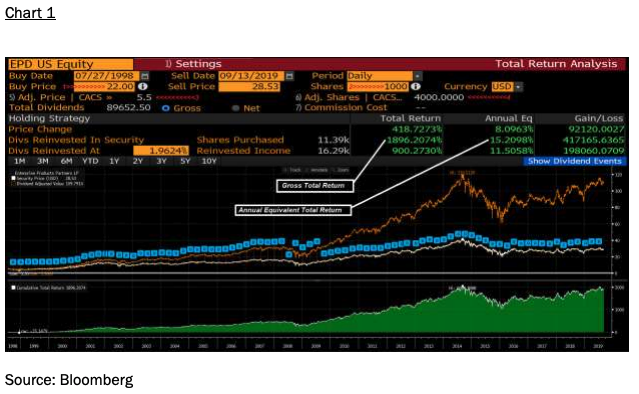

Warren Buffett when asked, “What is the ideal holding period for a stock position?” replied, “Forever!” The reason for that response is embedded in the U.S. tax code. And, Warren Buffett is correct because if the stock in question keeps increasing in value, and you never sell it, you do not have to pay capital gains taxes. Case in point, I called another great long-term investor namely Eric Kaufman of VE Capital, who is the best midstream Master Limited Partnership (MLP) portfolio manager I know. I ask him what would have happened if you bought Enterprise Partners (EPD/$28.53) on its Initial Public Offering (IPO) and held it until this month (Eric actually bought the IPO and still holds the shares). The IPO took place on 9-27-98 at $22.00 per share. Buying 1000 shares on that IPO, adjusted for two 2-for-1 stock splits, produces an adjusted ownership price of $5.50. The number of shares you would now hold is 4000. If you reinvested the dividend distributions over that timeframe, which kept increasing over the years, generates a per annum return of 15.2%, or about 500 basis points better than the per annum return of the S&P 500 (chart 1). As Master Po said in the TV series Kung Fu, “Patience grasshopper, patience.” Verily, as we have often opined – patience is the rarest commodity on Wall Street – which as Shad writes:

I have also noticed that most investors tend to sell their winners if they meet short-term objectives (12-month price target, financial projections, whatever). And so, they sell, and then they have to start all over, thus damning themselves forever to money manager underperformance hell.

We too plead guilty to sometimes adjusting short-term positions but would note those are “trading positions” not “investment positions.” We rarely disturb “investment positions.”

Turning to short-term “trading positions,” our models targeted the late-July trading top in the S&P 500 (SPX/3007.39) at ~3025. Subsequently, they called the “selling climax” low of August 5th at ~2822 that we said was THE low. That low was retested three time and was never violated. We further wrote the SPX is likely to trade out to new all-time highs. The jury is still out on that call, but after three attempts to do so the senior index is probably going to have to regroup before new highs can be achieved. Moreover, the D-J Industrial Average (INDU/27219.52) has rallied eight sessions in a row and history shows that markets rarely go more than 10 consecutive session in any one direction. So, we will say it again, “The senior index is probably going to have to regroup before new highs can be achieved.” Longer-term, however, we remain in a secular bull market that has years left to run.

We had a few random gleanings last week that we think are worth mention, so in no particular order:

1) U.S. Passive Stock Fund Assets [$2.4271T] exceeded active [$4.246T] for first time, which is anecdotal evidence you should be moving money to active managers.

2) 25 years ago, in 1994, Forrest Gump, Jurassic Park, Shawshank Redemption, Lion King, and Pulp Fiction were all in theaters at the same time. Compare that to the movies of Hollywood today.

3) So far this year in Sweden: 182 shootings, 120 explosions, cars being set on fire every night, 21 women raped every day on average in 2018.

4) Privately run Chinese firms bought at least 10 boatloads of U.S. soybeans on Thursday, the country’s most significant purchases since at least June. At more than 600,000 tonnes it was the largest purchase by Chinese private importers in more than a year.

5) Overshadowed by the ECB stimulus euphoria was the fact the U.S. August Core CPI increased 0.3% m/m and 2.4% y/y, the largest increase since September 2008. 0.2% m/m and 2.3% y/y were expected.

6) U.S. Core inflation exceeds forecasts as medical-care costs jump [0.7%, biggest since 2016].

7) Did anyone notice that U.S. Core CPI y/y is at its highest level since September 2008?

To this inflation point, and with what happened in Saudi Arabia over the weekend, stock market oracle Leon Tuey writes:

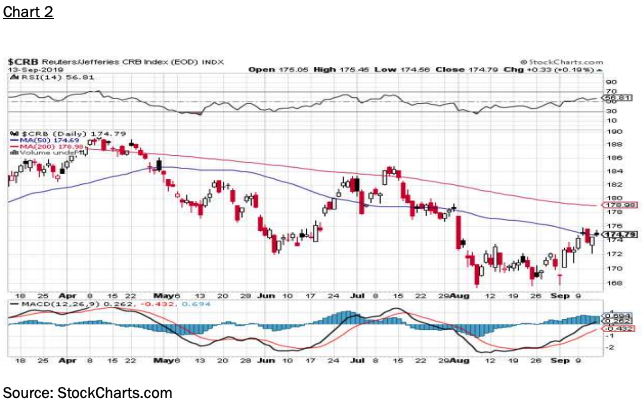

Technically, both Oil and Copper are grossly oversold and momentum is improving. Moreover, the resource stocks are under accumulation (smart/informed buying). Obviously, the smart investors are anticipating better growth ahead. The expected rally in the resource sector could be explosive as most have been preparing for financial Armageddon. Consequently, they are grossly under-invested in this area. Before long, when they realize not only there is no recession, but growth is actually improving and the rush to get in will be a sight to behold. Moreover, against this backdrop, resolution of the trade dispute will send the resource stocks and the market to the stratosphere. Strap on your seat-belts! Better yet, buy the energy/energyrelated and the metal issues before the stampede begins.

As Groucho Marx once exclaimed, “Who you gonna believe, me or your lying eyes?” Study the attendant CRB Index (Commodity Research Bureau Index), which looks to have bottomed (chart 2).

The call for this week: The yield on the 10-year T’note has risen from its September 3rd intraday yield of 1.42% into last week’s intraday “yield yelp” high of ~1.9% causing us to buy the Direxion Daily 20+ Year Treasury Bear 3X Shares (TMV/$12.05) a little over a week ago. We did not mention this in these reports because most of the major brokerage firms will not permit clients to buy any Exchange Traded Funds (ETFs) that are leveraged three-to-one times; and, we did not want to cause conflicts between clients and their firms, which has happened far too often in the past. Clearly, the rise in rates offers competition for stocks. Additionally, after three failed attempts to make new all-time highs typically it implies the SPX needs a rest to rebuild its “internal energy” before a breakout to new all-time high can take place. Surprisingly, the current rally over the past few weeks has come with our internal energy model showing it is not a favorable time for a rally. We would read that as bullish. Still, the senior index (The Industrial Average) is up eight consecutive sessions and indexes rarely go more than 9 sessions in a row in any one direction. All of this suggests a pause in the short-term as the internal energy is rebuilt over the next week or two before an upside breakout to new all-time highs can take place. Today’s discussion would not be complete without touching on the rotation from growth stocks into value stocks (chart 3) that was long overdue. One way to play this rotation is to buy the small-cap energy and material stocks whose prices look like stains on a carpet! We, however, do not make a whole lot of this rotation and would note that Wall Street will ALWAYS pay up for true growth. Today is “Aged Day” in Japan, a day to honor your elders. So, would someone please take me out to lunch at a great restaurant here in New Orleans. This morning the preopening E-mini S&P 500 futures (ESUs) are lower by 12-points, while crude oil futures are sharply higher on the Saudi attack. I sent this email to several portfolio managers yesterday morning:

Saudi Aribia (SA) said they could produce 9.8 million barrels a day using inventories. However, my contacts say that cannot last forever and that unless they can get production facilities back on line rather quickly oil prices are going up. One of my contact in SA told me last night she thinks it will take over a year to bring all the production back online. Of interest, is that the number of energy stocks in the Russell 2000 Energy Index moving above their respective 200-day moving averages has been increasing all year . . .

Investing/trading involves substantial risk. The author and Saut Strategy do not guarantee or otherwise promise as to any results that may be obtained from using this report. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first consulting his or her own personal financial advisor and conducting his or her own research and due diligence, including carefully reviewing any prospectus and other public filings of the issuer. These commentaries, analyses, opinions, and recommendations represent the personal and subjective views of the author, and are subject to change at any time without notice. The information provided in this report is obtained from sources which the author believes to be reliable.

© Saut Strategy

Jeffrey Saut

[email protected]

More ETF Topics >